@lohiyaakshay08 Thank you so much… This clarifies the doubt…

Posts tagged Value Pickr

Rural Elect Corp (30-04-2024)

Can REC reach IREDA valuation or at least REC should be given Bajaj finance valuation?

REC PE: 10 PB: 1.93

IREDA PE: 38, PB: 5.6

Bajaj Finance PE: 30, PB: 5.59

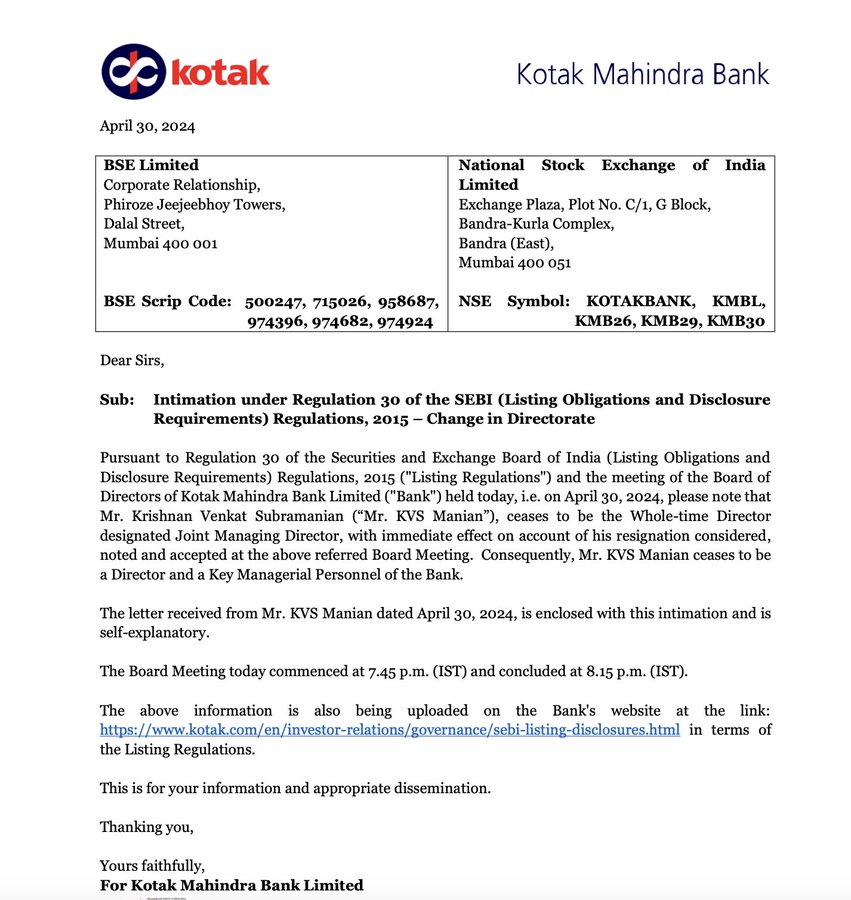

Kotak Mahindra Bank – Low Cost Liability Banking Franchise (30-04-2024)

Joint MD of Kotak resigns!

Zomato – Should you order? (30-04-2024)

Agreed. BlinkIt can even do a bigger gross than Dmart in the upcoming years

Shilchar Technologies – Power & Distribution Transformers – Sunrise Sector? (30-04-2024)

Shilchar reported solid earnings today. EBITDA margins remain rock solid at 30%,head and shoulders above peers. Revenue growth was disappointing however there is a large jump in inventories at 60 cr. for FY24. Company was slated to add around 40% capacity from April 1st. I am quiet sure Q1 will be better than Q4.

As an aside,while people are free to interpret data as they deem fit…recent posts on this thread seem increasingly disconnected from reality. So much so that people are suggesting Shilchar will need to dilute! Here is the current economics of the business:

Capex of 30 cr,addition of ~90% capacity on base of 4000 MVA. Company has done 118 cr revs in Q3 and should be able to do 500 cr on annual basis given current capacity. This number is going up by 90% assuming current realisations. Thus,an addition of roughly 450 cr revenue at a cost of 30 cr. However,this won’t happen in Year 1 itself. Let’s assume 50% utilization in Year 1. One gets addl revenue of 200 cr.

Given that the WC is 86-90 days this implies a capital employed of ~80 cr(50 cr wc+30 capex)

So what incremental margins does the company need to do to make 20% RoCE?

On assumed utilization of 50% the answer will be just 8% ebitda!(16/80)

However,Shilchar is currently making north of 25% margins. Even assuming a margin of 25% one gets RoCE of 60%. This in Year 1 itself at 50% utilization. Q4 exit is at 30% ebitda

At peak,we are talking of an RoCE of 80-90% on incremental capital employed!

I don’t see how such a company will ever need to dilute. On the contrary,markets are paying 50-55x fwd for a company from the same sector that has diluted to repair a broken B/S and has another QIP lined up. Shilchar is most likely trading at 35x fwd unless the whole economics of the business goes for a toss in coming quarters.

Disc.: Invested. Views are biased.

Sanghvi Movers (30-04-2024)

Generally found EPC to be a topline heavy business with slimmer margins of 12-14%.

I will be happy to be proven wrong and I hope Sanghvi Movers does earn margins that they have stated. In the meanwhile I wanted to be conservative in my estimates.

Sanghvi Movers (30-04-2024)

Generally found EPC to be a topline heavy business with slimmer margins of 12-14%.

I will be happy to be proven wrong and I hope Sanghvi Movers does earn margins that they have stated. In the meanwhile I wanted to be conservative in my estimates.

Manappuram Finance (30-04-2024)

Getting a nod for IPO is a big positive in view of regulatory hammering going on on banks and nbfc like IIFL

-not sure if IPO can unfold any value

-I feel IPO or no IPO value will remain same

But overall IPO is positive

Manappuram Finance (30-04-2024)

Getting a nod for IPO is a big positive in view of regulatory hammering going on on banks and nbfc like IIFL

-not sure if IPO can unfold any value

-I feel IPO or no IPO value will remain same

But overall IPO is positive

Arrow Greentech (Old name: Arrow Coated Products) – Anybody tracking (30-04-2024)

Hello Friends.

I was recently tracking this company. I could see they are entering into CDMO space (as per Feb-24 Presentation and completed a project for client) and also see one of director purchased from Market this week. though I see some negatives comments about this company in the past in above thread. recent price action and fundamentals seems improving. Request fellow investors review this company and provide your valuable inputs…