Yes, although i completely respect the experienced views of Mr Adityaji, even i was wondering the same. Margins in EPC could be higher as spoken by Rishiji in concall.

Awaiting your reply Mr. Aditya ji. Thank you

Yes, although i completely respect the experienced views of Mr Adityaji, even i was wondering the same. Margins in EPC could be higher as spoken by Rishiji in concall.

Awaiting your reply Mr. Aditya ji. Thank you

Hi, i think during covid, inventory days shot-up as radhika being a local player. But it looks like inventory days has been improving since then. Company also opened a new store which is 4 time larger then their previous store. The new store will take time to reach normal operation, till then inventory days will remain high.

As per management credit cost will be 1.65 going forward. So, its normal. Expect it at this level.

Number seems high because:

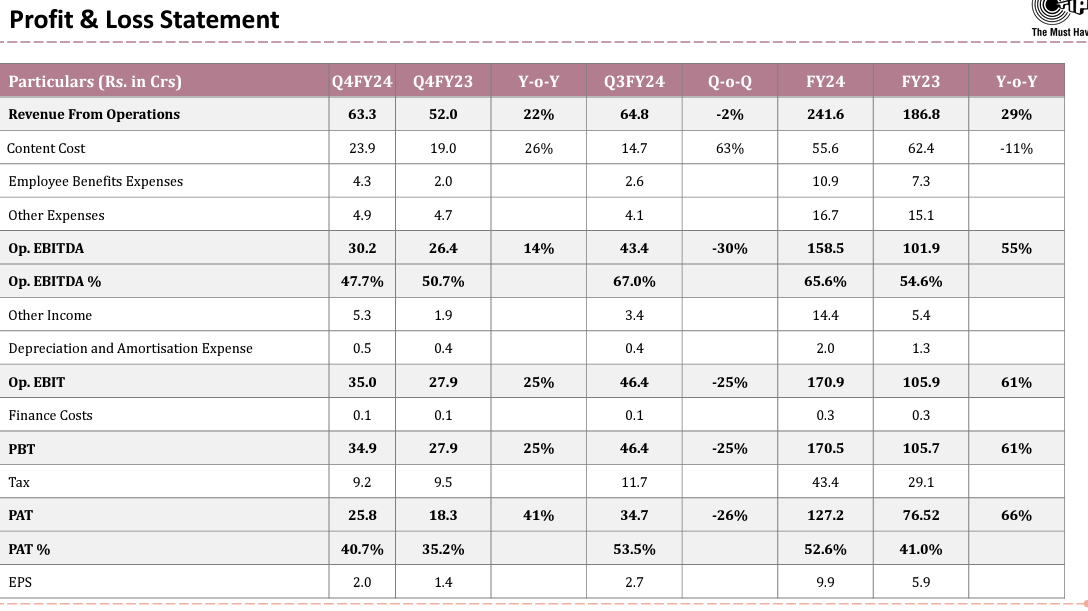

Concall link LII0820240429152482.mp3 – Google Drive

Concall takeaways

Disclosure: Invested

Why sudden 9 percentage fall in the counter??

Turnaround potential Cement pack after 2 Years

Another part to watch carefully,News of JSW Cement IPO!!!

Does anyone has any idea, why the provisions have gone up in this quarter? Did Mr.VV give any commentary on that?

Right Issue of Rs 400 Crores and objective of the issue

Repayment of Debt: RS 345 Cr

GCP: Rs 55 Cr

Was doing some research – the company has interesting history:

It was in BIFR, then the promoters bought 8% of shareholding at Rs.6

Many QIPs at various prices for funding capex. not much of funding projects through internal accruals.

promoters shareholding is down to 39%. with such low promoter holding such practices are bound to happen in small cap companies.

Company is in high growth segments and hence the pref. investments from Malabar and Anil K Goel.

But for smaller shareholders, is the risk-return justified.

Indostar Capital Finance Q4FY24 result Update: Posted Rs. 35.26 crores consolidated PAT in Q4FY24. The NBFC is focused on lending to the used-CV segment in T3/T4 space and the Affordable Housing Space in T2/T4 cities. The business has been running down its legacy SME book and is completely focused on growing the Retail book (CV+ Housing). Asset quality improved drastically with the company continuing to sell the bad loan SME book. GNPA: 4.9% vs 8% YOY in FY24. The overall loan book grew at a tepid pace of 11% YOY in Q4. PAT fell 50% YOY. All this would continue to put pressure on the ROE number. The company has also started monetising its security receipts which it shall use to grow the CV and the HL book. Indostar Capital Finance is still in a rebuilding phase and will take some time to come in good shape. Thnaks Deepak ![]()