simple screener not yet updated the balance sheet, pls check

Posts tagged Value Pickr

Mahindra Logistics (28-04-2024)

does any one know about their Financial liabilities, that is increasing year by year and hitting hard on the cash flow (321 cr on FY24)

Investing Basics – Feel free to ask the most basic questions (28-04-2024)

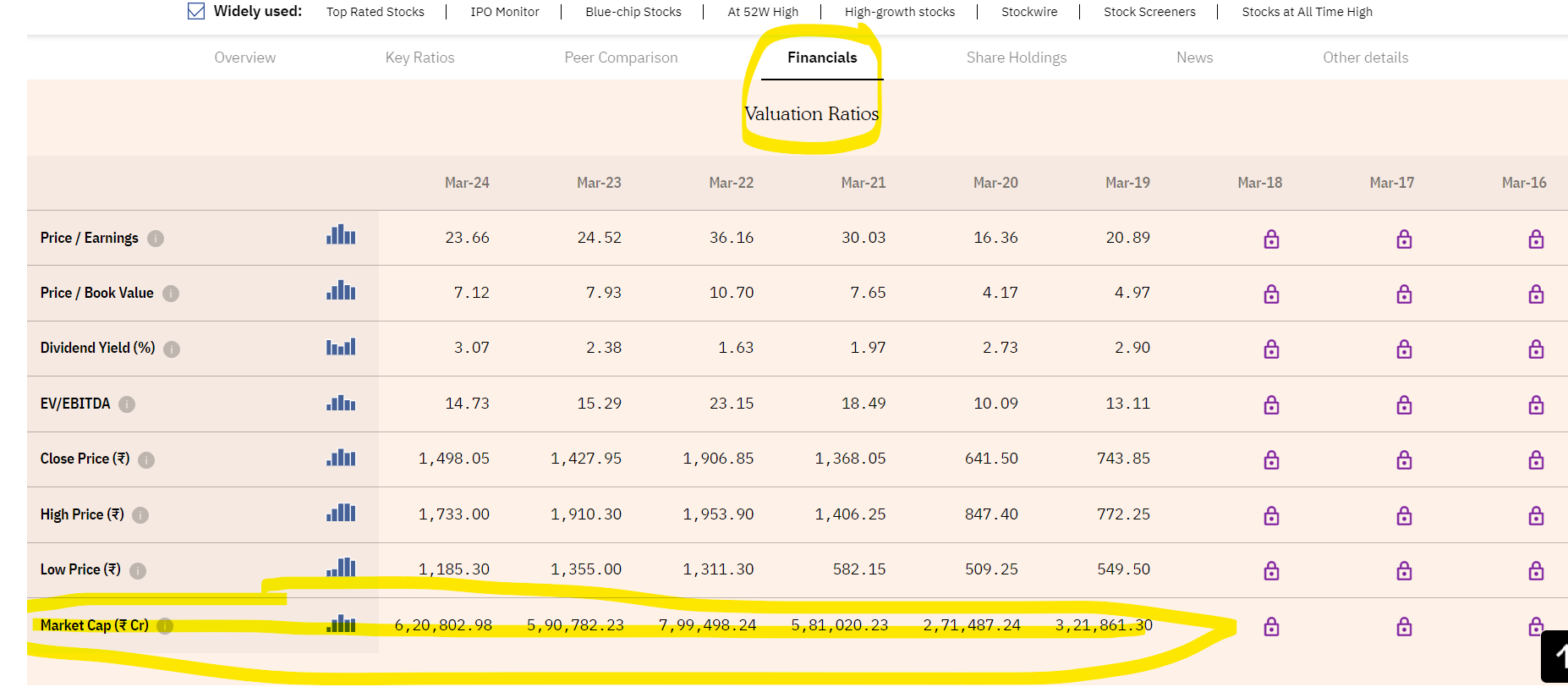

Refer Value Research online website (www.valueresearchonline.com) for Historic market Cap, values at the end of march.

For Infosys sample:

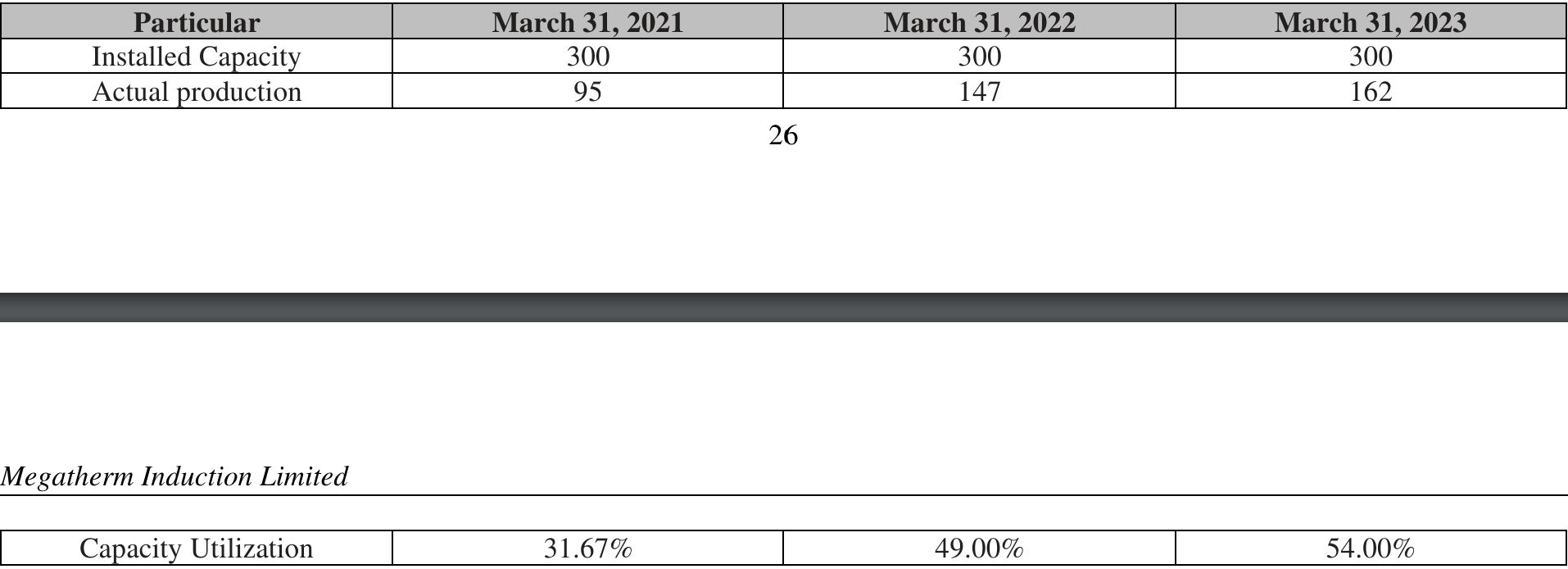

Megatherm – Mega Opportunity (28-04-2024)

Some information that I came across that should help you figure out the potential India’s steel industry currently possesses which will contribute to the growth of ancillaries, also do not forget the Paris Agreement. For more info, I suggest going through RHP page – 93 onwards.

Elecon’s Q4FY24 con-call –

Another factor confirms the trend –

Protean EGov Technologies Ltd – A Play on the ONDC, Digital Policies (28-04-2024)

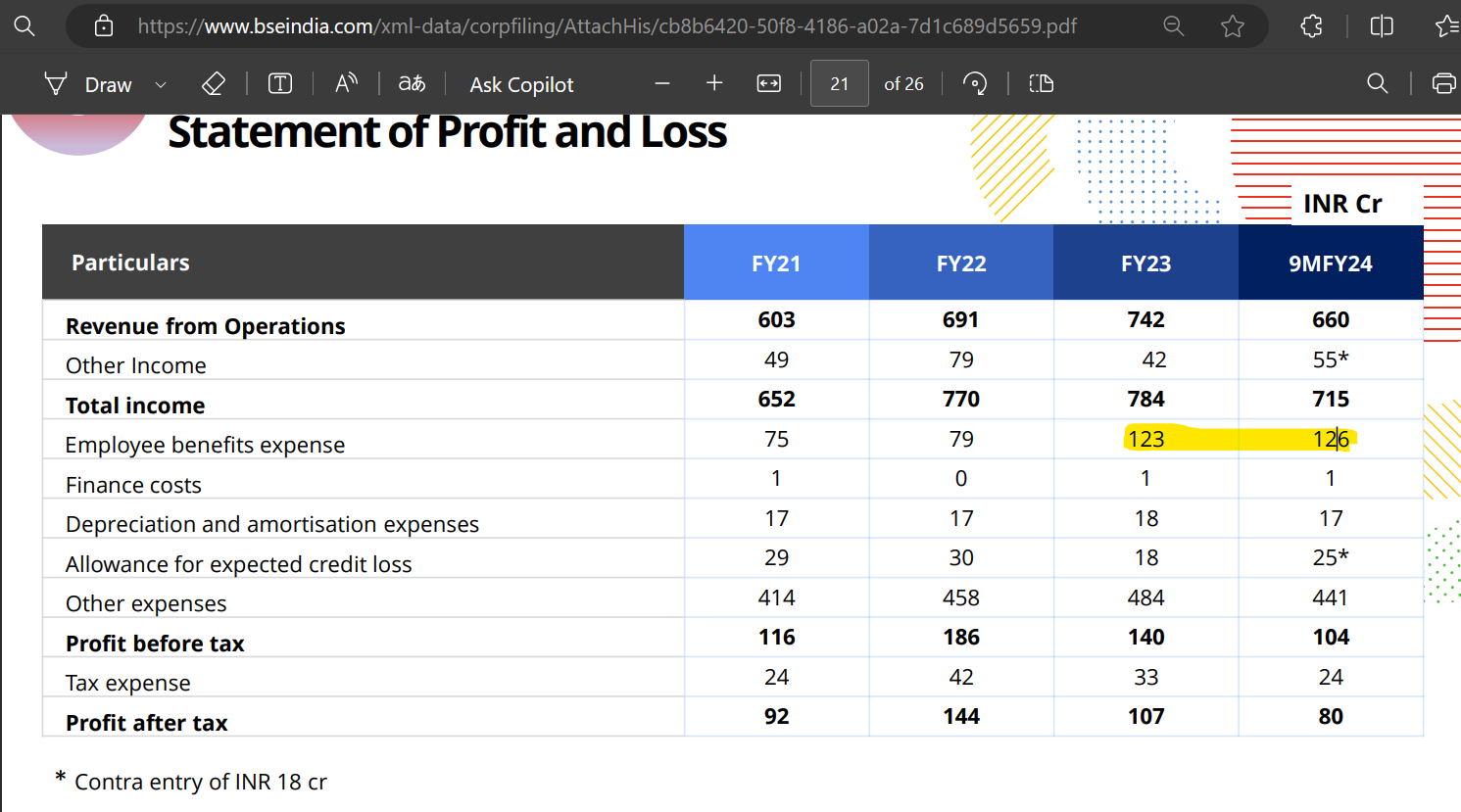

Can someone explain why the employee benefit expense has gone up by ~50Cr (66% increase) in FY23 and ~50Cr in 9M FY24. Are these one time, or recurring? Looks like recurring for now. Any updates would be appreciated.

Shilchar Technologies – Power & Distribution Transformers – Sunrise Sector? (28-04-2024)

I don’t think that a fast growing business will/should run out of working capital. I can name many small companies who are growing fast but are very prudent in managing their cash flow.

It’s important to distinguish between long term capital requirement and day to day operating expenses. It’s OK to raise debt for the first if you are in a fast growth phase and can’t fund that with internal cash. But for the latter a company should be able to consistently generate enough cash, from their operations, to buy raw material, pay their employees, clear their bills and fix broken equipment, at a very minimum, and still have enough for rainy days. If the management can’t do that, then either it’s a reflection of poor quality of management or nature of the industry.

Shilchar Technologies – Power & Distribution Transformers – Sunrise Sector? (28-04-2024)

My rule (unless an exception is proven ) is that any micro-very small cap stock (under 1000 cr market cap) that gives 15-20x move in 1-2 years, in a bull market, after having done nothing for ages, is being manipulated. With such stock one would normally see a lot of bullish management commentary, rosy business prospects, overflowing order-book, capacity additions and an exciting narrative about industry outlook.

So far without exceptions I have seen such stocks flaming out with retail left holding the bag. And it happens when people are least expecting it.

Ashok Leyland – A major CV player (28-04-2024)

I wrote a DETAILED article talking about the business of Ashok Leyland – here

Pros

- Infrastructure boom – GoI is spending BIG on infrastructural development and that will benefit AL + other CV players. A substantial amount has been earmarked for Capex in the Union Budget (around 10L CRORE) + the Government wants to convert 8 LAKH diesel buses into e-buses over the next 6 years.

- An astute management – AL is part of Hinduja Group which is a high pedigree conglomerate. On the earnings call, the management was very clear about it’s intent – it will NOT sacrifice profits / margins to gain market share but focus on the quality of the product instead. Over the last 10 years, AL has transformed itself from being a south centric player to a pan-India player with strong market share in most regions that it operates in.

- High barriers to entry – CV market is not easy to enter. It requires a lot of capital, and it takes a long time to achieve break-even, so you need deep pockets. No major entrants are expected in the short term.

- Future Growth drivers for AL:

M&HCV Business – the management believes that the industry is moving towards higher tonnage tractor trailers which has a higher selling price + higher margins. Globally, the penetration of high tonnage tractor trailers is quite heavy and in India it is only 20%. With goods roads that should increase and bode well for AL going forward and should help it expand margins.

LCV Business – LCV business has higher margins compared to M&HCV. Is less cyclical. And the current product portfolio addresses only 40-45% of the market, which means there is more room to grow and more variants that AL can launch in the future.

Investing in new technologies – AL is investing in EVs (through it’s step down subsidiary Switch Mobility), and in hydrogen fuel cells, hydrogen ICEs. In EVs, via Switch Mobility – it recently unveiled it’s e-LCVs which already has a pre-booking of 13,000 units. In e-buses, it has an order book of 1300+ e-buses. AL is also getting ready to launch electric trucks very soon.

Cons

- Cyclical industry – the growth in CVs is a factor of the growth in the economy, Any slowdown in the economy would adversely effect this industry and it is quite cyclical.

- High competition – even though the barriers of entry are quite high, existing players are quite BIG and very competitive. Tata Motors is the largest CV player in India.

- Commodity prices – the business is heavily dependent on commodity prices, especially steel. Although AL has been able to pass on increase in commodity prices to end customers, in a highly competitive scenario this might not always be possible

- High Debt – There is a significant debt on the books of AL, primarily because of the financing subsidiary (HLFL). However, investors should keep tabs on this # to ensure it doesn’t balloon out of control.

- No FY25 guidance – in the Q3 earnings call, no forecast was given by the management on estimated deliveries / revenue #s for FY25.

- Promoter Pledging – the promoters are pledged some of the shareholding, which is a red flag in case the stock price start to drop drastically

Conclusion

I think AL is being valued as a traditional CV company and the future potential in the e-bus / e-LCV / e-Truck segment is not being baked in. That said, it has to prove itself that it can capture a significant portion of the EV market to be able to command a premium valuation.

Disclosure: Not invested, tracking closely – waiting for a 10-15% correction to make a BUY decision.

IDFC First Bank Limited (28-04-2024)

When the Q4 FY 23 came up with a profit figure of more than 800 crores, the thought crossed my mind that it may stick out and make the upcoming quarterly performances of fy 24 look flat. The story has played out the same way.

However if one looks at the bank performance of last 5 years then the management has met all the targets except cost:income ratio which is as well. The bank is rightly on track to open new branches and investing in technology. This year credit card costs should drop below breakeven point by Q1/Q2.

The bank looks much better and healthier than fy 23. I feel, till the time infra book is on the balance sheet, the provisioning will continue to give negative surprises. Hopefully by fy25 end or H1 fy26 infra should cease to matter along with high cost legacy borrowings. That would complete the job of restructuring the business model.