Royal Orchid share has reacted to penalty imposed by SEBI. At this price it appears to be cheap as company’s performance is not impacted by it. After a difficult Q1, outlook is improving . Q3 is expected to be best. And new hotel at Mumbai is expected to be a game changer as it will start contributing from 2026 FY.

This is my expectation and I may be wrong. Invested.

Posts tagged Value Pickr

Royal Orchid Hotels – Available at good valuation! (30-10-2024)

Anant Raj Limited (30-10-2024)

Q2 FY 2025 CONCALL HIGHLIGHTS :

Fundraising and Growth Plans:

-

Anant raj is planning to raise ₹2,100 crores, with ₹100 crores from promoters and ₹2,000 crores from the market.

-

The funds will primarily be used to expand their data center business, specifically for cloud services, as it’s a very capital intensive venture costing about ₹100 cr/MW.

-

The company plans to expand its data center capacity to 63 megawatts by the next year, with 14 megawatts dedicated to cloud services.

Cloud Services:

-

Anant raj has launched “Ashok Cloud,” offering Infrastructure as a Service (IaaS).

-

They plan to expand to PaaS (Platform as a Service) and SaaS (Software as a Service) in the future.

-

The current cloud infrastructure has a capacity of 0.5 megawatts and is expected to reach at least 4 megawatts by the end of the FY ’25.

-

The company has partnered with Orange, a French company, for technical support.

Data Center Revenue and Capacity:

-

Anant raj’s existing 28 megawatt data center capacity is fully booked.

-

The data center revenue in the last quarter was ₹8 crores, with an 82% margin.

-

Anant raj expects cloud services to generate revenue of ₹150 crores per megawatt per year.

-

The company aims to provide more detailed revenue breakdowns for real estate and data centers in future investor presentations.

Real Estate Updates:

-

Anant raj has acquired 20 acres of land in Gurugram for ₹20 crores per acre.

-

This land will be used primarily for group housing projects, with a potential development of 3 million square feet.

-

The launch of their group housing project, Estate Residency, is expected in January.

-

The company plans to increase its rental income from commercial properties to ₹75 crores annually in the next two years.

Other Important Highlights:

-

The company is on track to become net debt-free by December 2024.

-

A news article reporting a court order halting 12 Anant raj projects was clarified as inaccurate. The issue involved only 1,000 square yards of land and no licenses were canceled.

Microcap momentum portfolio (30-10-2024)

This is fine. There is another one with Groww also. He presents his indicator in all these videos.

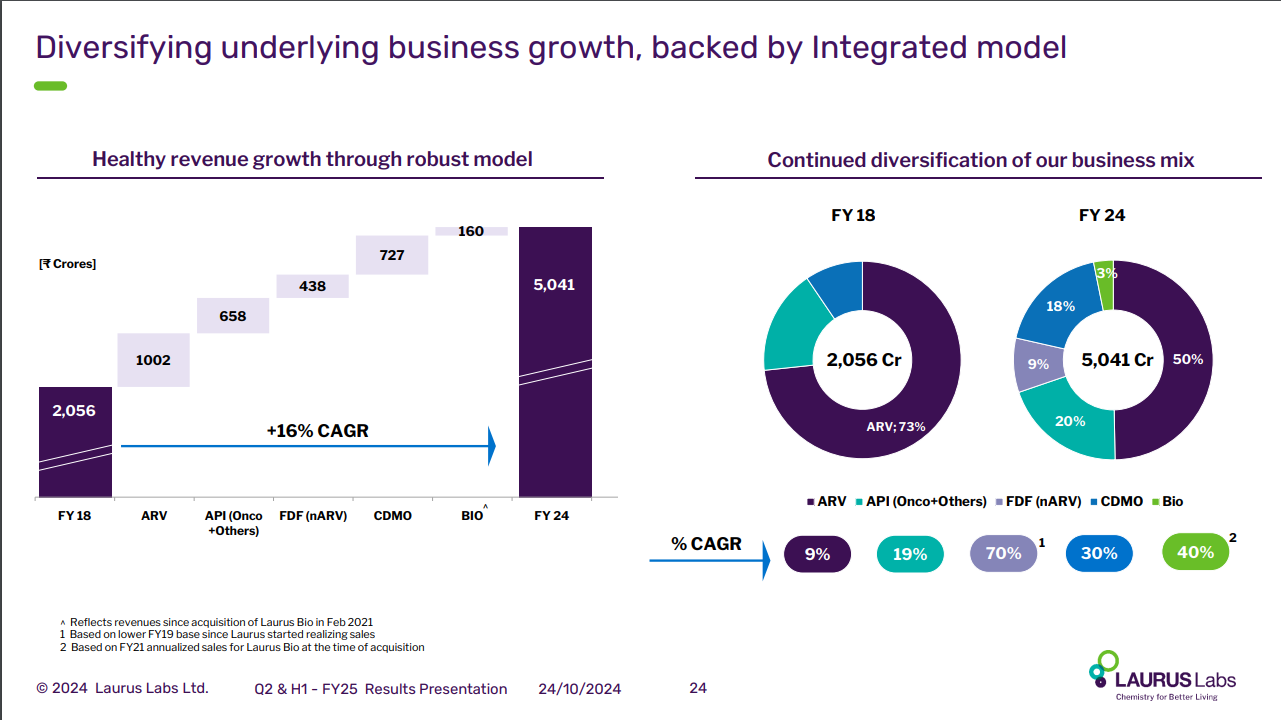

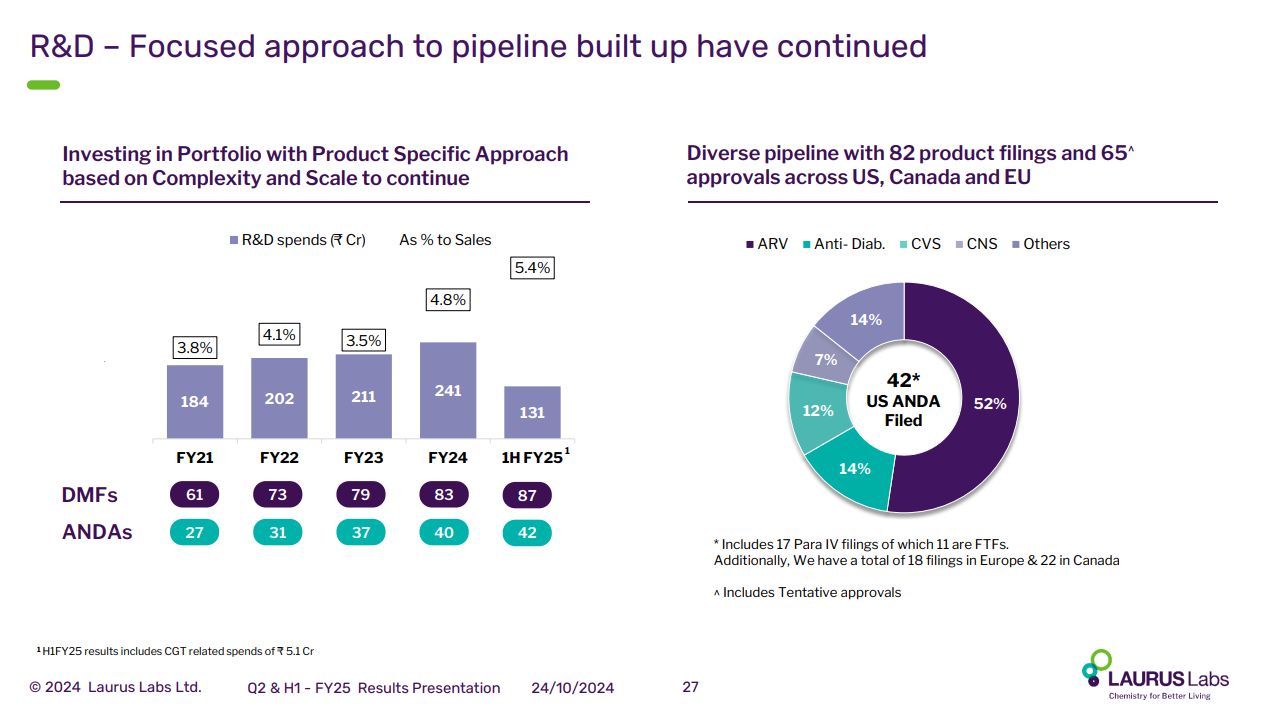

Laurus Labs – Can Business Transform to Next Level? (30-10-2024)

Laurus good summary of last 6 years progress.

R&D Spend and Current pipeline. 17 Para IV of which 11 are FTFs

MTAR Technologies – A wager on innovation meeting economies of scale (30-10-2024)

Concall:

FY25 revenue guidance- 725 Cr & Ebitda 21% is intact.

Closing order book ~ 1400 Cr from earlier guidance of 1500 Cr.

CY25- bloom indicated hot boxes numbers could be 4000 instead of earlier guidance of 3000.

FY26 guidance is 20% growth as of now with better margins as compared to FY25, I think by Q4 they will get more clarity on FY26 growth prospects.

Skipper Ltd., (Power and Water) a moat in making? (30-10-2024)

Skipper Limited Q2 FY25 Earnings Call Summary

Skipper Limited reported strong Q2 FY25 results, achieving its best ever second-quarter revenue of ₹1,190.5 crores, representing a 44% YoY growth. The company also delivered a record half-year revenue performance of ₹2,210 crores, demonstrating a 66% increase compared to H1 FY24. This impressive growth is attributed to robust execution in the Engineering and Infra segments.

Financial Performance

- Consolidated EBITDA for Q2 FY25 rose by 53% to ₹112 crores, while operating EBITDA margins improved to 10.1% from 9.5% in the previous year quarter. All segments experienced margin growth, with Engineering at 11.5%, Infrastructure at 6.5%, and Polymer at 4.6%. Management emphasized a continued focus on bottom-line improvement.

- Consolidated PBT for the quarter surged by 56% to ₹44.4 crores, resulting in a PBT margin of 4% compared to ₹28.6 crores in the previous year. Consolidated PAT also witnessed a significant increase of 66%, reaching ₹32.9 crores against ₹19.8 crores in the same period last year. PAT margins improved to 3%.

- Half-year export revenue grew by an impressive 233% to ₹410 crores, while consolidated PAT reached ₹65.4 crores, reflecting an 81% growth.

Segment Wise Information

- Engineering: This segment generated ₹845 crores in revenue, marking a 42% increase over the previous year quarter. The segment’s operating margin increased to 11.5%.

- Infrastructure: This segment achieved ₹160 crores in revenue, demonstrating a remarkable 149% surge. Notably, the segment’s operating margin significantly improved to 6.5% from 3.5% in the previous year quarter.

- Polymer: While the segment recorded a 7% decline in revenue, reaching ₹104 crores, its operating margin still saw an improvement to 4.6%. The management attributed this decline to channel partner destocking due to price volatility and a slowdown in water projects. They anticipate sales recovery in future quarters.

Growth Drivers

- Strong Domestic T&D Market: The company benefits from the robust growth of the Indian transmission sector, driven by government initiatives to expand renewable grid infrastructure and enhance electrification.

- Global Renewable Energy Trends: The worldwide shift towards renewable energy integration and carbon neutrality presents a significant long-term growth opportunity for Skipper Limited.

- Diversification: Skipper is expanding into new sectors like Telecom, Railway electrification, Water EPC, and Drip irrigation to strengthen its revenue streams.

- Capacity Expansion: The company’s ongoing 75,000-ton capacity expansion, expected to be commissioned by the end of the financial year, will enable it to capture growing demand.

Management’s Guidance for the Future

- The company expects continued growth in both top line and bottom line, supported by a strong order book and a favorable market environment.

- Management anticipates a 25% CAGR over the next three years and aims to reach a top line of ₹10,000 crores, potentially by FY29.

- While a specific target was not provided, the company aims to improve margins to around 11% over the next two to three years.

- Management emphasized a focus on securing higher-quality contracts, increasing export penetration, and implementing cost efficiency measures to enhance margins.

- Skipper Limited plans to further invest in capacity expansion, with a projected capital expenditure of ₹800 crores over the next four years. To fund this expansion, the company is considering raising ₹600 crores through equity or other instruments.

Key Risks

- Execution Challenges: The company’s ambitious growth plans are contingent on its ability to effectively execute projects, manage capacity expansion, and navigate potential supply chain disruptions.

- Competition: While Skipper Limited currently faces limited competition in the extra high voltage segment, new players entering the market could impact pricing and margins in the future.

- Raw Material Price Volatility: Fluctuations in raw material prices could affect profitability, particularly in the Polymer segment, which has already experienced some challenges.

- Dependence on Government Spending: The company’s growth is significantly tied to government investments in the power transmission sector. Delays or changes in government policies could impact its performance.

Industry Outlook

- The industry outlook remains highly positive. The Central Electricity Authority (CEA) projects an investment of ₹9.15 lakh crores in the power transmission sector by 2032. This significant investment is fueled by an anticipated 30% growth in interstate transmission line additions.

- This robust growth trajectory creates a favorable environment for Skipper Limited, positioning it to capitalize on the expanding demand and contribute to India’s energy infrastructure development.

Sheela Foam – An exciting branded play (30-10-2024)

There’s nothing wrong here. They have interest expenses from their acquisition and, on the other hand, depreciation—which was paid upfront but is recorded monthly in the books to leverage tax benefits. This isn’t exactly a deduction.

Yatharth Hospital & Trauma Care Services Limited (30-10-2024)

It is finalized – they have been recognized as the successful bidder for the model town hospital in new Delhi

Shivalik Bimetal Controls Ltd (SBCL) (30-10-2024)

I also first thought its family transactions from Sandhu to Ghumman family. But from screener we can easily see around 18% equity sold to Mutual Fund houses. Did they discuss any of these fund raise plan in AGM? Is there any further reduction of promotor holding in future?

Disclosure: Having exposure to this counter from long time. My views can be biased.

Happy Investing,

Karthik

Sheela Foam – An exciting branded play (30-10-2024)

Summary of the Sheela Foam Limited Q2 FY25 Earnings Conference Call (October 30th, 2024):

———————————————————–

Not attended any such call however providing summary of what has been provided over legitimate screeners.

———————————————————–

1. Acquisition of Kurlon

- The acquisition of Kurlon, finalized in October 2023, has been smoothly integrated into Sheela Foam’s operations. The integration included aligning operational models and optimizing distribution channels. Although both companies operate in the mattress industry, some differences in their business strategies needed to be addressed.

2. Financial Performance

- Standalone Results:

- Revenue: ₹602 crore, up 42% YoY.

- EBITDA: ₹70 crore (12% margin), up 54% YoY.

- Net Profit: ₹43 crore, up 12% YoY.

- Consolidated Results:

- Revenue: ₹813 crore, up 32% YoY.

- EBITDA: ₹69 crore (9% margin), up 5% YoY.

- Net Profit: ₹9 crore, down 79% YoY, mainly due to higher interest and depreciation costs from the Kurlon acquisition.

3. Growth Strategies

- Expanding in branded mattresses, particularly through Sleepwell and Kurlon, with branded mattresses contributing over 50% of total revenue.

- Increased stake in Furlenco to 45%, aiming for ₹500 crore revenue by FY28 in the growing furniture rental market.

- Launched new mattress brands, Tarang and Aram, targeting the economy segment, expected to generate ₹100 crore by FY26.

4. Operational Highlights

- Achieved ₹100 crore in annual run-rate savings post-acquisition, through scale efficiencies in raw materials, facility consolidation, and improved distribution.

- Reducing reliance on distributors in certain regions, like Karnataka, to improve margins and reduce turnaround times.

- Running a pilot to sell furniture in select Sleepwell centers, leveraging synergy with Furlenco, with potential for broader expansion.

5. Challenges

- Competition from unorganized players, especially in the economy segment. Sheela Foam is countering this with value-added products like the Fitress mattress, offering warranties and unique features.

- Balancing growth in branded products with profitability in the foam and furniture cushioning segments.

- Managing inventory effectively across its distribution network to optimize working capital.

Overall Outlook

- Sheela Foam Limited is well-positioned for growth in India’s mattress and furniture rental markets. The Kurlon acquisition, expanded branded offerings, and strategic investment in Furlenco have strengthened its market position and growth prospects.