Quarter after quarter this company fails to impress. Valuations still high in spite of a long time correction. Holding on to it since 2019 with negligible gains. Patience running out.

Posts tagged Value Pickr

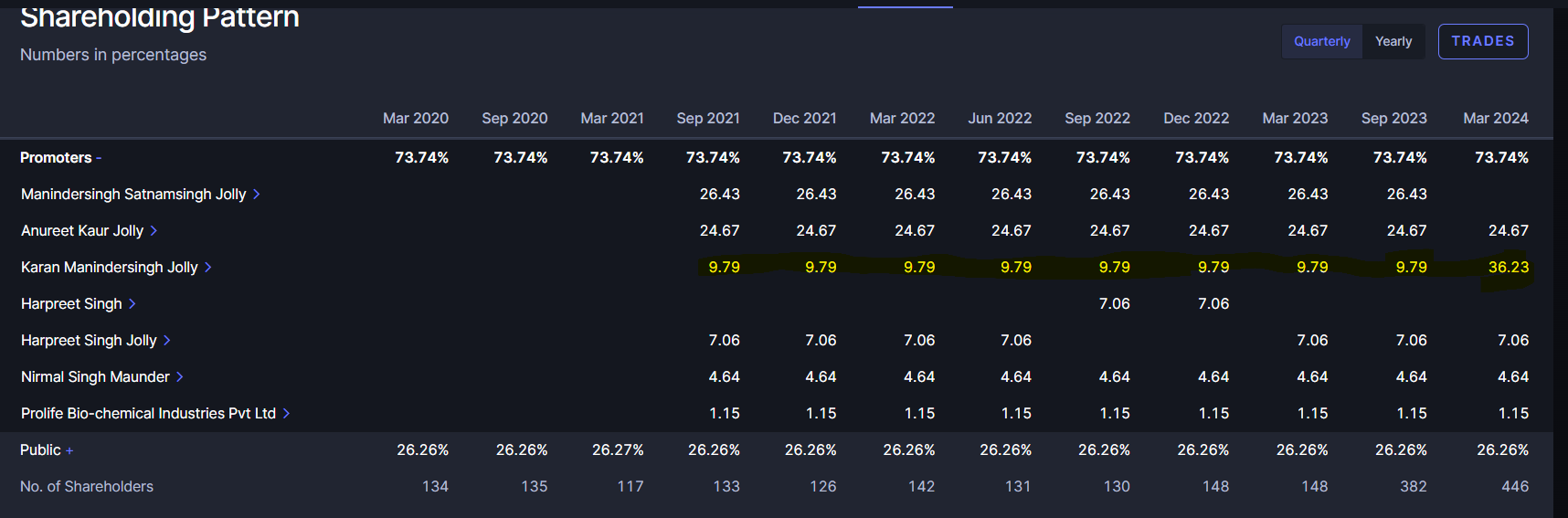

Prolife Industries – Emerging chemical SME company (25-04-2024)

I see there’s huge buying by promoter. Not sure whether to manipulate prices or bottom fishing.

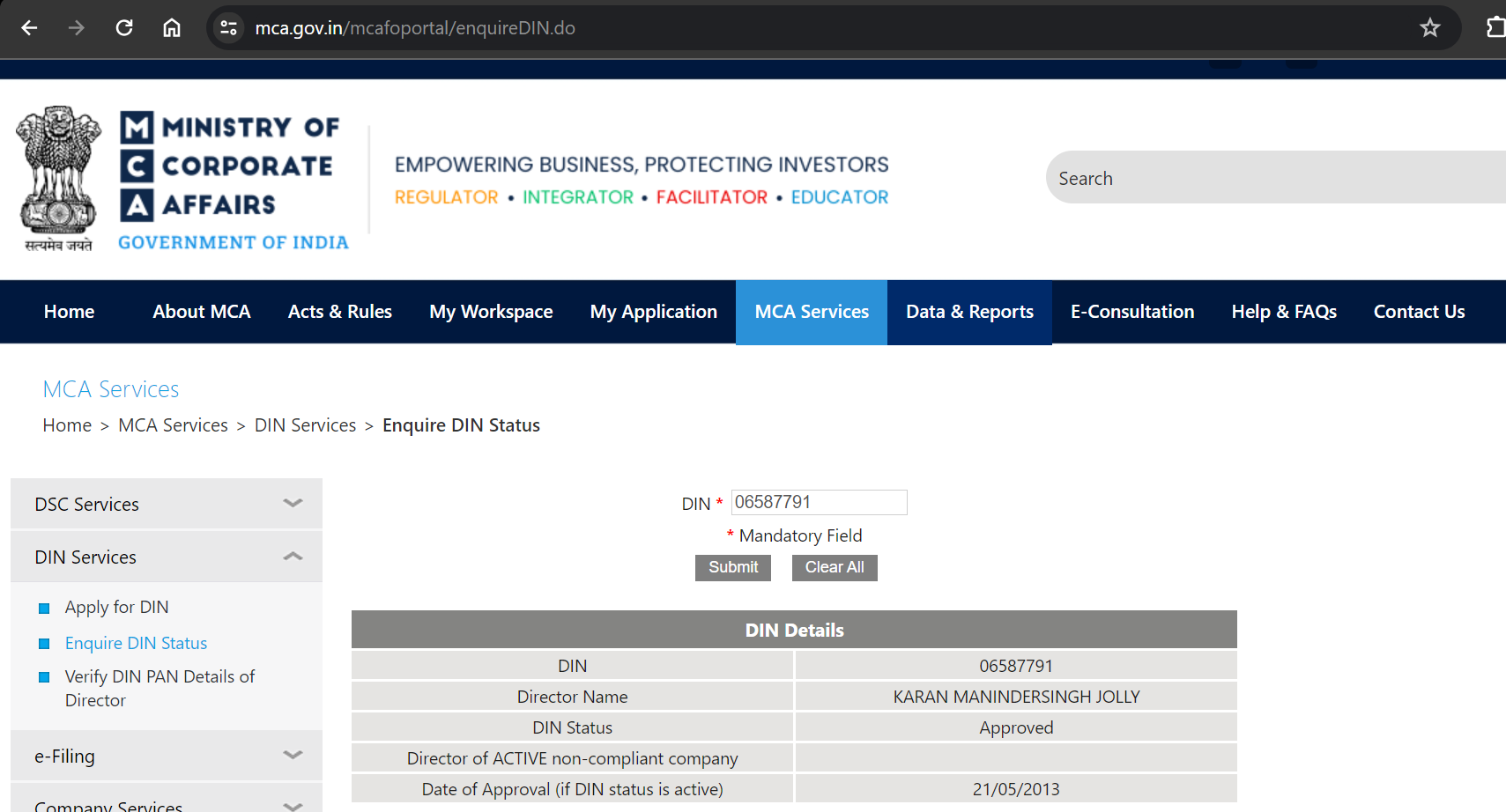

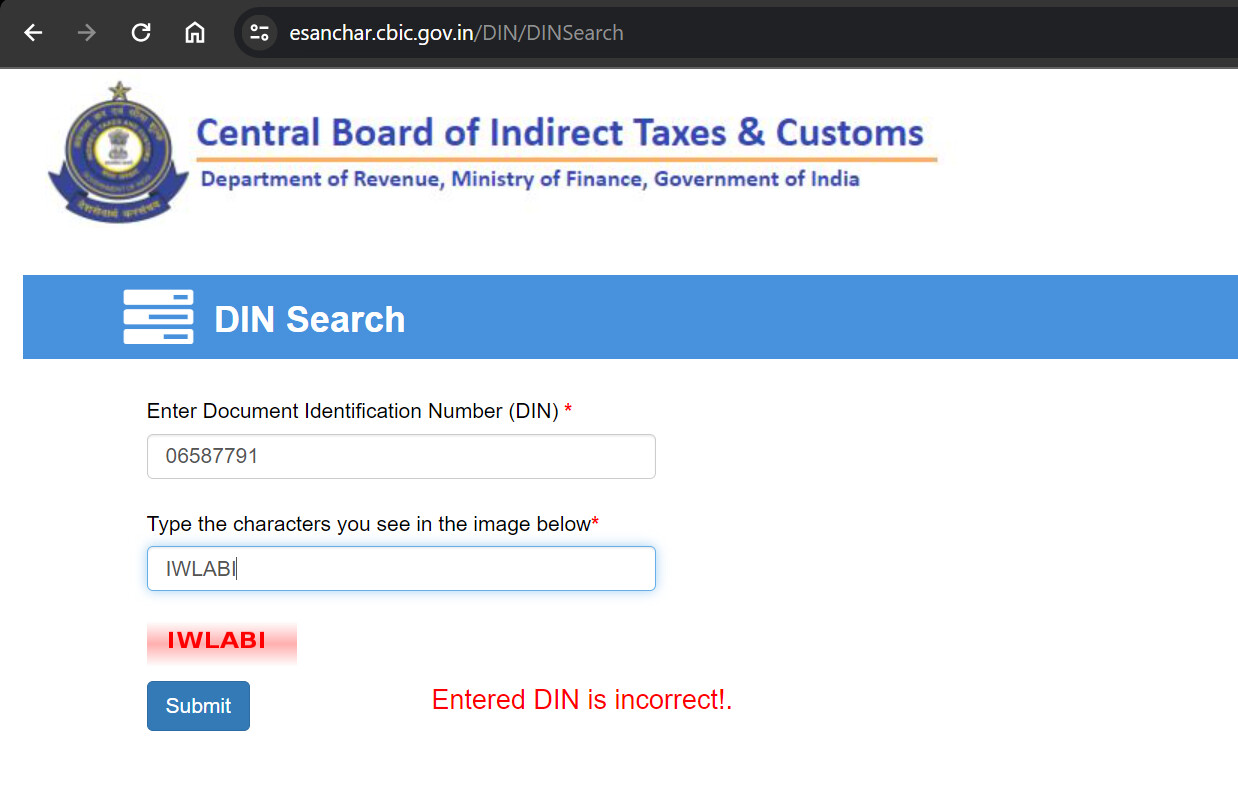

Regarding Promoter DIN I got contradictory results. Can anyone cross check what’s wrong.

B’s Notes : company analysis, portfolio roundup (25-04-2024)

HDFC_Bank

NIM’s are below 4% range due to merger. It is on the rise but may take a few years to get back to normal.

The CASA drop(38%) since 2022 continues and is yet to come back to normal

The cost of borrowing is at 4.9% on account of above along with merger of effects of HDFC.

The key concern is 1.6% growth in Gross advances QoQ and 4.34% Book Value Growth

Embassy REIT: Is this “Blackstone” promoted REIT is real diamond? (25-04-2024)

E-voting for the ESTZ acquisition and Rs3,000 crore equity capital raise has opened today. Depending on your depository, you can use either of the following links to cast your vote. It takes less than two minutes to cast your vote.

https://evoting.cdslindia.com/Evoting/EvotingLogin

While I’m still not too optimistic about the capital raise resolution failing, there still remains a small probability about a favourable outcome. This specific resolution requires 60% of the total votes to pass. As of 31st March 2024, the sponsor holds only 7.69% of the total outstanding units while institutions hold 73.63% and non-institutions hold 18.68% of the total outstanding units. This fragmented unitholder base and high voting threshold present a small probability that enough non-sponsor unitholders may not vote in favor of the resolution for it to cross the 60% threshold. In such a scenario, votes cast by retail unitholders may prove to be the deciding factor. As a disclosure, while I voted in favor of the first resolution regarding the acquisition, I voted against the second resolution regarding the equity capital raise.

Tata Consumer Products Limited (TATACONSUM) (25-04-2024)

One problem they have is either wrong strategy or execution on Nourishco Brand.

This if done well should be a blockbuster brand with 2500 Crores in Revenue by FY27. But execution lacking.

I see their cup style Packaging as a issue. Needs bottle and new packing wiz Appy styled bottles. Product can move better. They are focusing on low priced pack when they can also move to higher priced at 20-30 Rs Packs.

Rest their execution is actually reasoble and will do well over next few years. They have the brands to perform.

Invested from Lower levels.

B’s Notes : company analysis, portfolio roundup (25-04-2024)

Kotak_Bank

As an optimistic investor I am sure Kotak Bank will correct from their mistakes. It may entail additional expenditure and may hurt their growth temporarily (2-3 qtrs – not this qtr.) but for a long term investor these are the exact opportunities to add in to this stock.

Reference can be found in Dec. 20 to Aug. 21 HDFC Bank ban which is very much similar.

The most difficult part is assessing what price is right for such an entry.

Disclaimer: May Hold positions.

Geospatial sector – Sunrise Opportunity (25-04-2024)

Very nice and detailed information ![]()

![]()

have written about genesys in this thread you can have a look

![]()

Samhi Hotels – Turnaround with Tailwinds (25-04-2024)

In my opinion demand will improve post elections as the new govt may introduce some policies to bring up the travel industry. (?). even aviation sector is facing some challenges. Domestic travel has to go up so that these hotels will see better results.

Samhi Hotels – Turnaround with Tailwinds (25-04-2024)

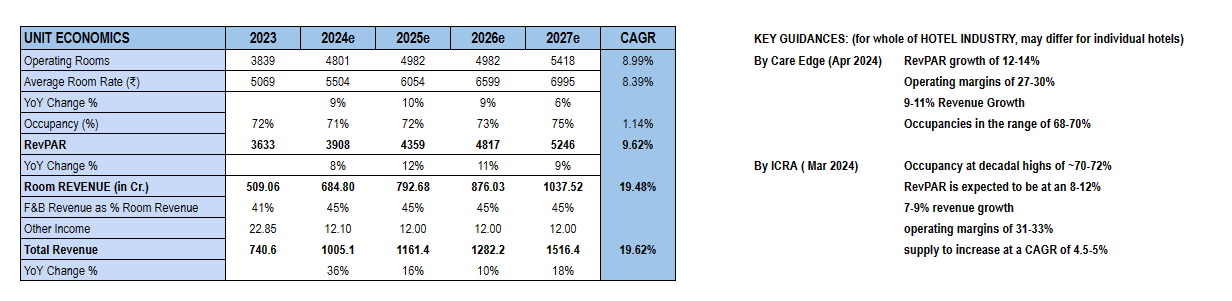

Thanx for sharing your views… Here is my views on the Unit Economics of SHAMI hotels.

TAILWIND

^ IHCL Commentary Q3Fy24 – Hotel room demand growing at 8-10% far exceeds supply at 5-6% CAGR.

^ As per ICRA Mar 2024 – In FY2024, the RevPAR is expected to be at an 8-12% discount to the FY2008 peak. ICRA expects hotel industry to report a 7-9% revenue growth. And as per various research report SAMHI rev growth will be close to 20%.

^ As per Jeffries report Mar 2024- “Foreign tourist arrivals have yet to catch up, while Indian Nationals’ Departures are back to pre-COVID levels.” which is a tailwind for SAMHI hotel being internationally recognized brands. With Occupancy CY23 broadly matches CY19 levels.

Occupancy at close to 70% in Fy2024 which can further go to 80-85%.

Samhi Hotels – Turnaround with Tailwinds (25-04-2024)

Hello

Thank you!

For me I view competition as increasing Supply

SAMHI is this premium position( not ultra luxury like Oberoi but premium) where the average key price is 1-2cr and the time to build considerable keys takes a few years!

I am not worried on the supply side as whatever a company does, they can’t hasten the process by a few years to build keys!

However, I am worried about Demand side! If consumers were to spend less and the traction reduces, there could be a problem!

In terms of tailwind for the company, my bet is mainly on the sectoral tailwind+deleveraging that the company can do. I am not so sure, but the cities that SAMHI operates in will have increasing demand compared to India so the rate at which the RevPAR can shoot up is higher!

Check Chalet hotels as well, they too operate in similar geographical areas