Kotak 811 has huge traction especially for onboarding corporate customers for salary accounts. Its absence will have a dire impact on deposit growth.

Posts tagged Value Pickr

Raghav Productivity Enhancers (RPEL) (25-04-2024)

Anyone tracking the latest updates on this company – please shed your insights on this stock? Seems like solid consolidation in last 7 months and at support now technically.

Indian Energy Exchange (IEX) (25-04-2024)

Any thoughts about IEX to enter now around 140-150 price range.

Sterling & Wilson Solar Ltd. – Will the Sun Keep Shining? (25-04-2024)

Any update on this? Is it in EPC space? What is the valuation of the acquistion?

Suggestion on mutual fund SIP (25-04-2024)

Quant mid cap is also doing as good as it’s small cap.

It the top fund in mid cap catagory.

It s 3 months return is 15 percent while 2nd best mid cap return is 11 percent.

Sandeep Kamath Portfolio | Momentum Investing (25-04-2024)

When we can expect adding of fundamental stand point, what is weightage given to 6M and 12M, have you considered Sharpe ratio ratio also, thank you.

Oracle Financial Services (25-04-2024)

Strong numbers from OFSS

Q4 Revenue up 12% YoY and Profits up 17% up year on year.

Dividend Rs 240

Now this is not blockbuster result like last Q but this is sill best in industry and stock is still reasonably priced considering sticky, geo-diversified, high margin, B2B, only listed blue blooded software products company.

Some analyst may have built unreasonable expectation based on last Q cloud bookings and we may see some knee jerk reaction.

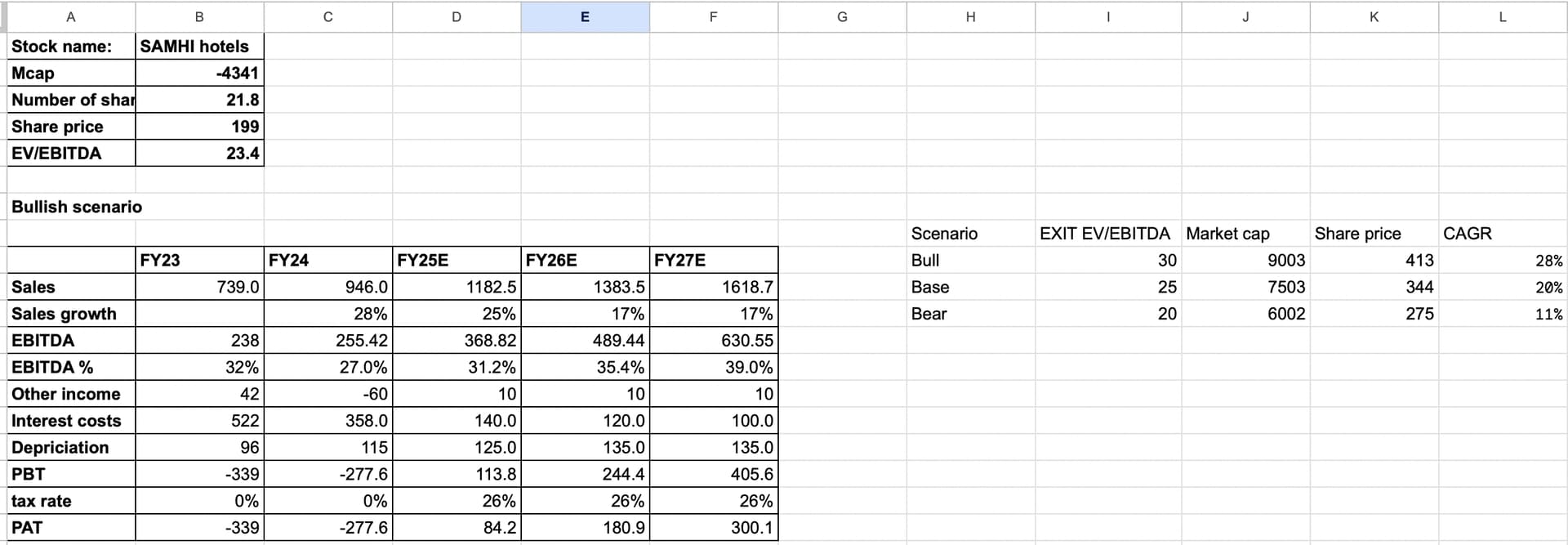

Samhi Hotels – Turnaround with Tailwinds (25-04-2024)

I am quite bullish on SAMHI hotels

Here is my thesis and Financial model regarding my investment

Thesis

Sales growth

FY25 will see addition of around 10-12% more keys which are being added or will get ready from renovation. Moreover, we can expect a RevPAR in double digits, although we are seeing RevPARs in high teen or in the twenties, I don’t know if that can sustain and hence a growth rate of around 13% has been assumed until FY27E

The decline in growth rate from FY26 and FY27 is because not a lot of keys are being added, and we can only expect the newly renovated ones to start(around 900 are under renovation)

EBITDA

The business aims to increase the margins to around 38-40%. Moreover, they shared a chart in one of their presentations that talks of types of costs. 20% was variable and after looking at it, I thought of an additional 20% being semi variable in nature. Despite the fact that semi variable won’t rise as much as revenue, I assumed 60% of the additional revenue each year trickling down to EBITDA.

That is how the model has been made!

Other income

It shouldn’t be negative the next few years because the current year had a one off event and the company took the worst possible scenario and wrote off 70 crores.

Depreciation

It shouldn’t really increase because no keys are being added, only existing portfolio is getting renovated

Interest costs

for FY25, the debt is assumed as 3.7x their EBITDA which is their target. The cost of capital for the business is around 10% and hence the interest cost. Although the management hasn’t guided towards interest cost reduction or anything for FY26 and FY27, the free cash generation does make me believe that a bit of reduction might happen( not taking that into consideration is fine)

Anti thesis pointers

It really comes down to supply and demand

Supply: it’s not dealing in luxury and deluxe luxury hotels, and hence the time taken to build supply is less. So there can be a risk of supply catching up faster than expected against demand

Demand: there could be some issue regarding the whole travelling trend. If foreigners do not come back to precovid level( I don’t see a reason why they won’t) the revPAR won’t go up as much as expected

Debt: If the cycle were to turn for some reason, there will be a big problem as the business can suffer a Lot and might not be able to pay back. Cycle upturn is key for Deleveraging!

Disc: Invested and biased

Srivari Spices and Foods Limited (25-04-2024)

Company has placed its products on D Mart online (Hyderabad only I guess).

Shilchar Technologies – Power & Distribution Transformers – Sunrise Sector? (25-04-2024)

last quarter eps was 35. Let’s take 30 going fwd for 2 years. Given the tailwinds in this sector, this is base case.

Mgmt has guided for 900 cr top line in 2 years with new capacities incrementally online from April 2024.

Base case.

30 (eps) * 4 = 120 with existing capacity

60 (eps) * 4 = 240 with new capacity // 2026 end

240 * 30 PE = 7200 (stock price)