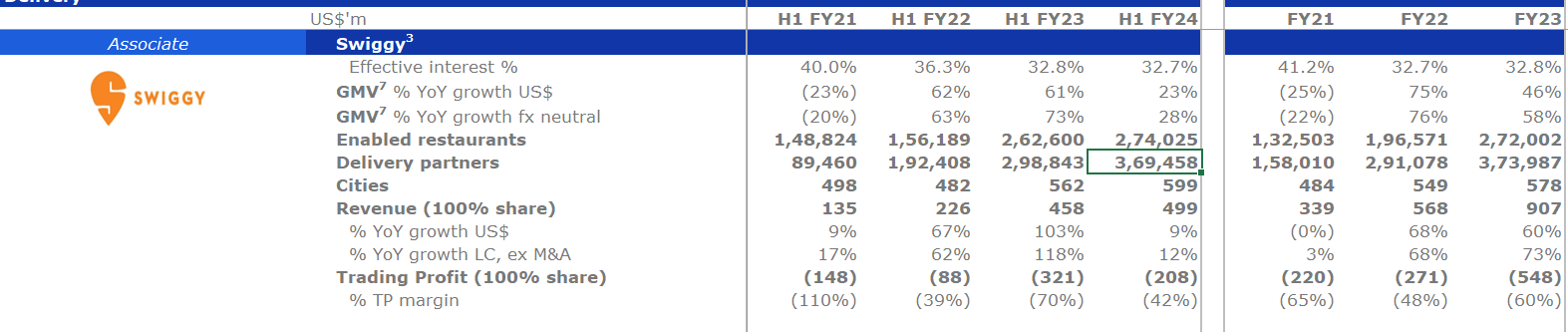

Was able to find the note by Prosus (Swiggy’s investor) that has H1FY24 data… the slowdown in revenue growth for Swiggy is astonishing.

I’m not sure how long will Swiggy continue to hold given the relatively poor economics when compared to Zomato.

Was able to find the note by Prosus (Swiggy’s investor) that has H1FY24 data… the slowdown in revenue growth for Swiggy is astonishing.

I’m not sure how long will Swiggy continue to hold given the relatively poor economics when compared to Zomato.

I missed buying further at that price point, thinking it will drop to 150 levels, quickly went upto 255 and now available around 215-225 levels, assuming certain sell and buy triggered those movements.

In future wont miss these entry points, Vikram Solar will do well.

SUN PHARMA –

Q3 results and concall highlights –

Sales – 12381 vs 11241 cr, up 9 pc

EBITDA – 3477 vs 3004 cr ( up 15 pc, margins @ 28 vs 27 pc )

PAT – 2561 vs 2181 cr, up 19 pc

Region wise sales break up –

India Formulations – 3778 vs 3391 cr, up 11 pc

US Formulations – 3973 vs 3465 cr, up 13 pc

EM Formulations – 2094 vs 2115 cr, down 2 pc

RoW Formulations – 1779 vs 1556 cr, up 13 pc

API sales – 466 vs 515 cr, down 9 pc

EMs include – Romania, Russia, RSA, Brazil, Mexico

RoW Mkts include – Western Europe, Japan, Canada, Israel, NZL, Australia

R&D expenses @ 824 cr, @ 7 pc of sales

Company is ranked No-1 in India with 8.5 pc Mkt share and 32 brands in top 300 brands. Top 10 brands contribute to 18 pc of India sales

Total manufacturing facilities @ 43. Formulations facilities @ 29, API facilities @ 14

Company’s speciality products contribute to 17 pc of company’s topline ( mostly coming from US ) and are growing at rates faster than company growth rates. Currently, the company has a basket of 26 speciality products

Speciality products include –

Illumya

Winlevi

Levulan

Absorica

Odomzo

Cequa

Bromsite

Xelpros

Yonsa

Sezaby

Kapspargo Sprinkle

Speciality products Pipeline –

Deuroxolitinib ( phase -3 completed )

Illumya for Psoriatic Arthritis ( phase – 3 )

Nidlegy ( phase – 3 )

MM- II ( phase -2 completed )

SCD-044 ( phase – 2 )

GL0034 ( phase – 2 )

Net cash on books @ Rs 8200 cr ( Ex – Taro ). Net cash including Taro @ 18,300 cr !!!

Launched 28 new products in India in Q3. Seeing good traction in the in-licensed products portfolio in India

Illumya, Cequa and Levulan grew strongly in Q3. Growth in US was partially offset by ongoing USFDA related compliance issues at Mohali, Halol plants. Launched 03 generic products in US in Q3

Brazil and Romania business grew strongly in Q3

Global Speciality sales grew 26 pc in Q3 to reach 2100 cr in Q3. This represents 17 pc of company’s topline

Generic Revlimid sales in Q3 in US were muted

Supplies from Mohali plant likely to ramp up over next few months. At sub-optimal levels currently

Nidlegy’s ( for Skin Cancer ) Phase – 3 data in Europe is very encouraging. It should be a significant product for the company going forward

In Q3 in India, company’s volume growth was around 7 pc which is far higher than IPM

Looking to in-license products in the GLP-1 category for India Mkts. GLP-1s should be important products going forward in India. GLP-1 products like Ozempic, Wegogy are global blockbusters

Disc : holding, biased, not SEBI registered

SUN PHARMA –

Q3 results and concall highlights –

Sales – 12381 vs 11241 cr, up 9 pc

EBITDA – 3477 vs 3004 cr ( up 15 pc, margins @ 28 vs 27 pc )

PAT – 2561 vs 2181 cr, up 19 pc

Region wise sales break up –

India Formulations – 3778 vs 3391 cr, up 11 pc

US Formulations – 3973 vs 3465 cr, up 13 pc

EM Formulations – 2094 vs 2115 cr, down 2 pc

RoW Formulations – 1779 vs 1556 cr, up 13 pc

API sales – 466 vs 515 cr, down 9 pc

EMs include – Romania, Russia, RSA, Brazil, Mexico

RoW Mkts include – Western Europe, Japan, Canada, Israel, NZL, Australia

R&D expenses @ 824 cr, @ 7 pc of sales

Company is ranked No-1 in India with 8.5 pc Mkt share and 32 brands in top 300 brands. Top 10 brands contribute to 18 pc of India sales

Total manufacturing facilities @ 43. Formulations facilities @ 29, API facilities @ 14

Company’s speciality products contribute to 17 pc of company’s topline ( mostly coming from US ) and are growing at rates faster than company growth rates. Currently, the company has a basket of 26 speciality products

Speciality products include –

Illumya

Winlevi

Levulan

Absorica

Odomzo

Cequa

Bromsite

Xelpros

Yonsa

Sezaby

Kapspargo Sprinkle

Speciality products Pipeline –

Deuroxolitinib ( phase -3 completed )

Illumya for Psoriatic Arthritis ( phase – 3 )

Nidlegy ( phase – 3 )

MM- II ( phase -2 completed )

SCD-044 ( phase – 2 )

GL0034 ( phase – 2 )

Net cash on books @ Rs 8200 cr ( Ex – Taro ). Net cash including Taro @ 18,300 cr !!!

Launched 28 new products in India in Q3. Seeing good traction in the in-licensed products portfolio in India

Illumya, Cequa and Levulan grew strongly in Q3. Growth in US was partially offset by ongoing USFDA related compliance issues at Mohali, Halol plants. Launched 03 generic products in US in Q3

Brazil and Romania business grew strongly in Q3

Global Speciality sales grew 26 pc in Q3 to reach 2100 cr in Q3. This represents 17 pc of company’s topline

Generic Revlimid sales in Q3 in US were muted

Supplies from Mohali plant likely to ramp up over next few months. At sub-optimal levels currently

Nidlegy’s ( for Skin Cancer ) Phase – 3 data in Europe is very encouraging. It should be a significant product for the company going forward

In Q3 in India, company’s volume growth was around 7 pc which is far higher than IPM

Looking to in-license products in the GLP-1 category for India Mkts. GLP-1s should be important products going forward in India. GLP-1 products like Ozempic, Wegogy are global blockbusters

Disc : holding, biased, not SEBI registered

@Pragnesh thanks for sharing. what new stocks do you recommend at this point based on its valuation? Is it reasonable to enter the below stocks at this point of time?

Beta drugs

Pix transmission

Carysil

Apcotex

Astec

Paushak

Prevest denpro

I always had this question for rapidly growing Banks/NBFCs: why use P/B at all? It is more of a “present” metric rather than something that takes into account the future.

And instead of PE, use it growth in AUM + sales (something similar like PEG) to get a better sense of the value that they would generate for us shareholders.

Disclosure : Invested

This company is in a cyclical industry. Money is made by investing while PE is high, margins are low and selling when PE is low and margins are high.

Dec 23 OPM is 3%, TTM OPM is 5%, where as at the peak of the cycle it was 25%. Did some basic google searches – Based on an article in TOI in Dec 22, in FY25 there will be an oversupply of both BOPP and BOPET. BOPP capacity would be 1300KT against demand of 1075KT. BOPET capacity would be 1200KT against demand of 940 KT.

Assuming above data is correct, there will be pain for another 4-8 quarters, however with most companies starting to report ~80% reduction or negative PAT, it will be interesting to see if companies will put the expansion on hold, or might run in to financial issues. If that were to happen, well run companies will be set for next up cycle.

Is any one tracking this industry?

Maybe they just need the money. Small selling is not ever anything to worry. The short term top might have been set to have reached if

A. There was a climax move where everyone was talking about it and RSI went through the roof or a parabolic move happened with stock pricing doubling from say maybe a 30 week moving average.

B. The stock went up just on narrative with no concrete improvement in business or with poor results. As far as I can see, Mr Vageria has delivered what he’s promised.

C. There was a change in the business in sales or margins which the market hadn’t factored in or ignored – which we will probably know in the results.

Generally stocks pause to take a breath after a 50 percent upmove. In fact, it’s not given a deep correction even on carnage days. This seems like a consolidation phase in a narrow range.

As far as the crude oil price hike is concerned, I suspect companies which depend on crude a lot will or should have a pass through clause to protect their margins especially in longer term contracts.

Why do you think that double digit growth is only for two years?it will help if you can explain about the longevity of business.i was of the opinion (solely assumption) that this company has strong chance of more than 15%cagr for next five years atleast considering the diversity of the sectors it’ is present.Also management is known to give conservative guidance in past and not overpromise…

Bias…have tracking position

Folks, just 2 cents from me…

Please understand that many a times there are other decisions also in consideration for management to decide between equity and debt.

Like they may want to onboard some marquee institutional investors who gives credibility and visibility to the company among the various stakeholders. It wouldn’t be nice to have a 2.5 to 3kcrs marketcap and have no insitutional investors onboard. In this case, having two reputed DIIs (LIC and SBI MF) in QIP gives a lot of credibility on corporate governance and future potential.

Regarding doing fund raise, as someone has mentioned, their quarterly run rate will be now 500crs which gives 80% capacity utilisation. In any industry if you see significant demand coming in the future then you need to start building capacity well in advance. It will be foolish for company to let go some orders just because capacity is under construction!!!

Thanks