A very well-written note highlighting the core issue here.

Posts tagged Value Pickr

HDFC Bank- we understand your world (16-04-2024)

A very well-written note highlighting the core issue here.

HDFC Bank- we understand your world (16-04-2024)

(post deleted by author)

HDFC Bank- we understand your world (16-04-2024)

(post deleted by author)

Marksans Pharma- Can it be the next Pharma Biggie? (16-04-2024)

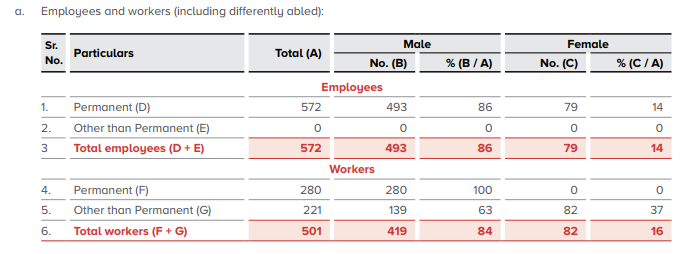

I have been going through the 2023 Annual Report, and I don’t know what numbers to expect but for some reason these remunerations and ratios seem a bit too much. Are these the industry standard?

Even with a decent employee/workers count the median renumeration felt a bit odd. (Company total Income being 7157.86 Million in Indian Rupees)

I could be completely wrong on this, just starting with AR’s, and I did not what to expect, hence looking for guidance.

Marksans Pharma- Can it be the next Pharma Biggie? (16-04-2024)

I have been going through the 2023 Annual Report, and I don’t know what numbers to expect but for some reason these remunerations and ratios seem a bit too much. Are these the industry standard?

Even with a decent employee/workers count the median renumeration felt a bit odd. (Company total Income being 7157.86 Million in Indian Rupees)

I could be completely wrong on this, just starting with AR’s, and I did not what to expect, hence looking for guidance.

HDFC Bank- we understand your world (16-04-2024)

There is a reason for stock underperformance.

Credit growth is what drives banking industry while deposits are fuel for them. Higher deposit growth means low capital cost for banks as they don’t have to tap financial markets for raising debt which comes at higher cost (e.g. 8-12% compared to 3-4% interest rate on savings account or 7% on FD accounts). This translates into higher net interest margin (NIIM). Finally asset quality of a bank shows their ability to recover their loans from the borrowers- less bad loans means less provisioning for NPA meaning better bottom-line.

HDFC bank of late has “disappointed” on all these metrics after the merger.

1- They inherited a lot of bad loans from the HDFC limited impacting asset quality

2- Net cost of deposit went up due to high cost of debt of HDFC limited, the latter being an NBFC

3- They have been conservative (and rightly so) in their lending (avoiding risky borrowing class) impacting credit growth

4- Slow deposit growth means they are attracting less deposits from Indian public raising questions on their ability to raise capital at low cost- having implications for NIIM

All the above will impact profit growth, ROE and ROA, the main determinants for a bank’s valuation.

Coming to valuations, HDFC and Kotak Bank have historically delivered superior performances on both ROE and ROA, compared to their peers, which drove up their valuations in the past, both trading at much above 3 times book for a very long time.

But now some of their peers are catching up on both ROE and ROA which has resulted in moderation in valuation premium for both and hence time correction in their stock prices. Investors are choosing to invest in cheap banking stocks (trading at marginally above their book value) with slightly lower ROE and ROA than HDFC and Kotak.

Valuation concerns for HDFC seem to have ebbed, with stock trading at somewhere 2.5 times book. But low valuations don’t automatically translate into higher stock prices; they only offer downside protection (depending on the quality of the stock). Investors invest based on what a company will deliver in the future and not what it has done in the past.

So no doubt HDFC bank is a high quality franchise and has a great track record of execution. But they need to deliver the results for stock to get rerated. Merger has proved to be an overhang and it will take some time before stock can find its mojo back.

Disc- invested.

HDFC Bank- we understand your world (16-04-2024)

There is a reason for stock underperformance.

Credit growth is what drives banking industry while deposits are fuel for them. Higher deposit growth means low capital cost for banks as they don’t have to tap financial markets for raising debt which comes at higher cost (e.g. 8-12% compared to 3-4% interest rate on savings account or 7% on FD accounts). This translates into higher net interest margin (NIIM). Finally asset quality of a bank shows their ability to recover their loans from the borrowers- less bad loans means less provisioning for NPA meaning better bottom-line.

HDFC bank of late has “disappointed” on all these metrics after the merger.

1- They inherited a lot of bad loans from the HDFC limited impacting asset quality

2- Net cost of deposit went up due to high cost of debt of HDFC limited, the latter being an NBFC

3- They have been conservative (and rightly so) in their lending (avoiding risky borrowing class) impacting credit growth

4- Slow deposit growth means they are attracting less deposits from Indian public raising questions on their ability to raise capital at low cost- having implications for NIIM

All the above will impact profit growth, ROE and ROA, the main determinants for a bank’s valuation.

Coming to valuations, HDFC and Kotak Bank have historically delivered superior performances on both ROE and ROA, compared to their peers, which drove up their valuations in the past, both trading at much above 3 times book for a very long time.

But now some of their peers are catching up on both ROE and ROA which has resulted in moderation in valuation premium for both and hence time correction in their stock prices. Investors are choosing to invest in cheap banking stocks (trading at marginally above their book value) with slightly lower ROE and ROA than HDFC and Kotak.

Valuation concerns for HDFC seem to have ebbed, with stock trading at somewhere 2.5 times book. But low valuations don’t automatically translate into higher stock prices; they only offer downside protection (depending on the quality of the stock). Investors invest based on what a company will deliver in the future and not what it has done in the past.

So no doubt HDFC bank is a high quality franchise and has a great track record of execution. But they need to deliver the results for stock to get rerated. Merger has proved to be an overhang and it will take some time before stock can find its mojo back.

Disc- invested.