But do you think that REIT got compensated for taking on this risk. I assume that GIC bought 50% so REIT and GIC wouldn’t have been handed a raw deal by sponsor. As long as it is fair deal, it is not a concern. Also, Brookfield is viewed as professional as they are probably largest globally in this business.

Posts tagged Value Pickr

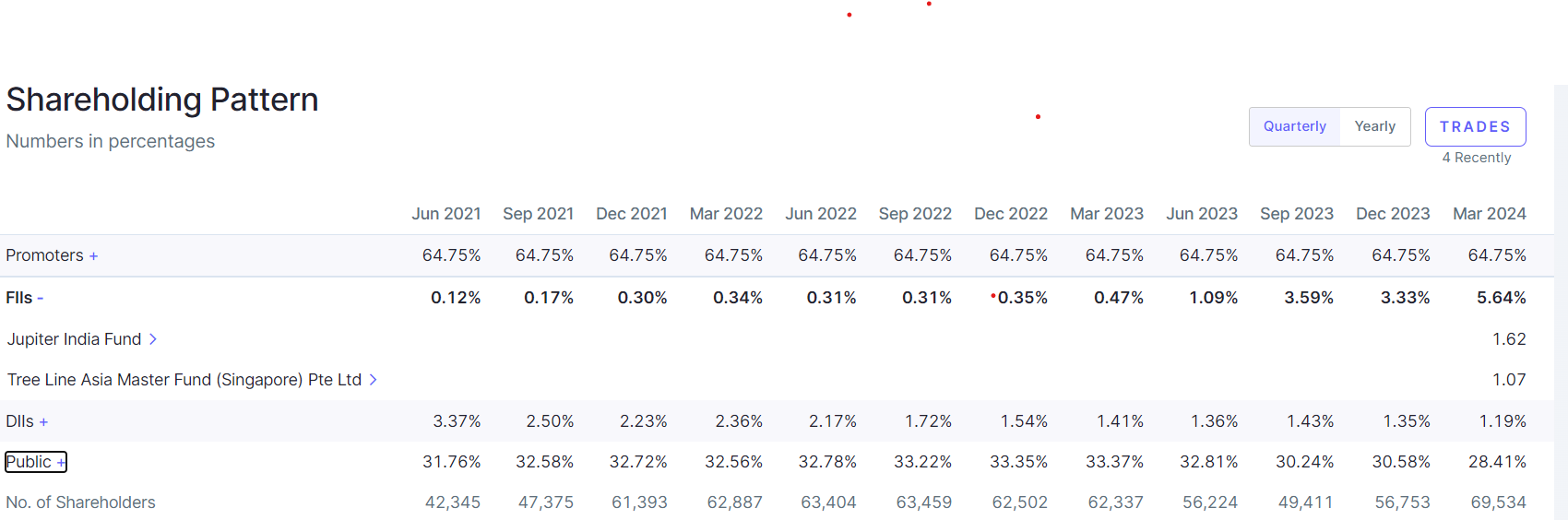

Time technoplast (14-04-2024)

Recent gas pipeline scheme for each home will dent company business?

Solex Energy – Undervalued Solar PV Manufacturer or Microcap Value Trap? (14-04-2024)

Anybody still tracking this company?

Promoter pledge is 0%

Stock is in a clear uptrend both in weekly, daily timeframe

There was a bulk buy on 12 Apr for 0.6%

CMS Info Systems Ltd (14-04-2024)

Not yet. Thanks for the nudge. I’ve sent them a reminder.

MSTC Ltd.: Growth through to E-Commerce (14-04-2024)

FII are continously increasing stake and reached to 5.64% in March 24

Time technoplast (14-04-2024)

Company has first mover advantage in Hydrogen cylinders… it can be game changer for the company…

it is at multi-year breakout… sky could be the limits… am expecting it to go up 100% more from here…

Va Tech Wabag (14-04-2024)

I think the mgmt started applying corrective action plans based on the lesson learnt in the past. A few I could see from their recent presentation are:

-

Outsouring construction work – Core expertise focused on Engineering and Procurement; Civil activities outsourced

-

Reducing Debt – Reduction in net interest cost due to reduction of debt and effective utilization of bank lines

-

Focus on ‘Advanced technology, Value Added & High Margin’ projects enables to remain asset light (Patents, Technology Innovations, Tie up with ‘Pani Energy’ to implement applied AI, etc)

-

Focuses on projects funded by Central Govt., Multi Laterals & G2G Funding

-

Exploring future opportunities on

-

Green Hydrogen (They are in discussion with Hydrogen Developers for collaboration as their water partner)

-

Ultra pure water requirements for Semi-Conductor industry

-

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (14-04-2024)

As anticipated, Ethanol blending target of 20% has no target date (earlier it was 2025)… even PM is not mentioning when the target will be met.

He mentions one more use of bagasse – bio-degradable cutlery… hopefuly demand will go up now…

Sugar consumption has increased to 29 -30 mn tons.

https://twitter.com/fooddeptgoi/status/1778688756381569294

Good days ahead for the sugar sector… demand increasing from multiple uses… entire sector could see a rerating…

Oriana Power – SME play on Renewable Energy (14-04-2024)

Thanks Sulabh for starting thread on Oriana Power. It was long pending as it is one of the most promising renewable energy (solar, hydrogen, CBG) microcaps company.

Few Pointers:

1/ FY24 Numbers: As per crisil report, orderbook in March’24 was 900crs+. They are expected to report revenues of 350crs+ in FY24 (350crs is minimum, they can report 375-400crs as per my expectations), this is 3x vs FY23

2/ Order book: Current order book should be around 1100crs. They should keep getting new orders around the year specially now as they have successfully completed some big projects in last FY (like Coal India etc). Orderbook should be significantly more by FY25 end

3/ Valuations: It is expected that they should report 1100-1200crs revenues and 110-130crs PAT in FY25 (3x growth vs FY24). This translates to 19-22x FY25PE. Other competitors Waaree Renewables and KPI Green are trading at 50x FY25PE. Oriana is expected to show highest growth among the big players and trading cheapest.

3/ Solar Parks: They are currently setting up 350MW solar parks across three states. Concall should provide more details on these

- Rajasthan – 100MW (total 250MW)

- Maharastra – 50MW

- UP – 50MW

4/ International Expansion: They are also expanding to Middle East market and participating in Dubai Energy exhibition on 16th-18th April. This market is expected to be a big contributor for them in next 1-2 days as only handful companies have international experience.

5/ Both green hydrogen (electrolysers + EPC) and CBG (EPC) should be a big growth driver for the company apart from solar EPC.

6/ Management Bandwidth // Strategic Mentor: The have this unique management combination that there are three young promoters who are expert in their own areas: Rupal (Sales/BD); Anirudh (Investor Relations/Strategy); Praveen (Operations)

Also they have Prashant Jain (ex MD JSW Energy) as strategic investor and mentor who has very deep understanding of the renewable energy market.

Thanks

Disclosure: This is just a research note. This is not a buy//sell recommendation

Jkil — jkumar infraprojects (14-04-2024)

agree…

due to entry of few “reputed” investors has helped the stock shoot up… this is the story over and over again in the market. JKIL had shot up to 400 in Aug 2015 and then down to 100 levels in Jan 2020 (pre-covid). again it is time to correct… be careful.