Shri. Akshay Kumar Singh, MD & CEO, Petronet LNG Limited said “the existing long-term agreement

between Petronet LNG & QatarEnergy today accounts for around 35% of India’s LNG imports and is of

national importance. Renewal of this agreement is a step towards achieving vision of Hon’ble Prime

Minister of India to make India a gas-based economy and increase share of natural gas in India’s primary

energy basket to 15% by year 2030. This agreement will provide energy security and ensure stable &

reliable supply of clean energy and help India in its stride towards greater economic development.”

He further added that the long-term LNG purchase agreement with QatarEnergy will further strengthen the

existing relationship between the two Companies.

Posts tagged Value Pickr

Petronet LNG Limited – Green India with Clean Fuel (12-04-2024)

Suggestion on mutual fund SIP (12-04-2024)

Welcome, and be invested for long term, it will definitely rewarding, if you need any suggestions ping me on 9960147980

Aditya Birla Fashion and Retail Ltd (12-04-2024)

An additional view to inform your decision:

Summary: I am a shareholder for ~4.1 years in ABFRL and despite a decent return, am losing confidence in the management’s capital allocation (specifically ability to exit portfolio companies where they are unable to demonstrate right to win) which is hurting shareholder returns (and will likely continue to do so). My interpretation is that the management is focused / remunerated (?) on top line growth and therefore have taken their eye of shareholder returns.

The net effect is that the share count has increased by 38% through multiple fund raises (Rights, Flipkart, GIC, TCNS), have been destroying Net Worth since FY20 excl new shares issued (ok some of this can be attributed to covid) and have increased debt >2x (and have been put on negative watch by credit rating agencies – although credit rating is still strong).

I suspect the split was driven by new shareholders who converted their shares at Rs 288 when the market price was ~Rs 200. This is certainly a step in the right direction and will probably ensure that the new demerged company (ABL) will not get diluted further – but with slower revenue growth (low single digits and should they be in Forever 21?). ABFRL will continue to be diluted (already stated in the press release), will continue to grow fast and questions remains on whether all the businesses make sense (TMRW?)

Discussion

The management has built an excellent portfolio of some brands that promise good growth. As part of any brand portfolio development, it is important that the management reviews areas where they are unlikely to win. So they may grow revenues – but if they cannot make profits they need to exit. By their own classification – this is applicable to their segments of Sub-premium and Value

-

Forever 21 is an example of a business which has been struggling to make money since FY19. There is always some new plan that they are unable to execute on.

-

Pantaloons – FY23 seemed to be a turnaround in terms of EBITDA, but they are back to struggling. And they entirely missed the Zudio wave. This business feels very fragile in a competitive environment

-

TMRW: This is an area of real concern as they seem to be running this like a valuation driven start-up – grow revenues to build scale – at a loss for the next 2-3 years, bring in new investors. Aryaman Birla has been inducted as a director on this – so can’t really see they exiting this business. From my limited understanding, this is probably the most competitive part of the market with the lowest brand loyalties and barriers to entry. Their own forecasts of loss in Q2FY24 for the full year were already exceeded in Q3 – a quarter later. This feels like a bottomless pit with no clear advantage

Unless they are able to demonstrate that they can exit businesses from their portfolio – this M&A led growth is unlikely to be effective. There has been no evidence of this in my view and remains the biggest question mark on capital allocation

Of the two companies, ABL seems a safer bet (although that does not imply a good bet). There is demonstrated profitability in the Lifestyle business, there is a base effect challenge in the Innerwear (among other challenges) but hopefully can turnaround and some very strong growth businesses – Reebok, Collective, American Eagle). If they exit Forever 21, this should be a clean business. Please do see discussions above on whether the Lifestyle brands have a moat though Aditya Birla Fashion and Retail Ltd – #95 by nikhildoshi

ABFRL is a real mixed bag with a lot of uncertainties. Premium and above ethnic has promise – Sabysachi seems to be doing well (revenue and profit) – disclosure is limited though. Taasva will require ongoing investments. Unclear on the smaller brands S&N, Jaypore, Masaba. Pantaloon is a question mark though has improving revenue and ebitda metrics (on a per sqft basis) – but still far from industry standard. TMRW feels like a hole.

Conclusion: The TAM is very large and they have good brands. But if they do not exit brands where they are unable to create a sustainable business (in my mind sub-premium and value segments), they are unable to invest sufficiently in strong businesses because the balance sheet is so stretched. For me it makes sense to hold until the demerger, as that should create value. I am watching for more signs on better capital allocation (driven by new investors) before making a final decision on whether to stay invested in this business. I could not find anything on management KPIs for remuneration – but I hope this is not only top line.

Disc: Hold a fully invested position so am likely to be biased. Am not a registered financial advisor and none of the above should be interpreted as financial advice

Piccadily Agro Industries Ltd (12-04-2024)

Link to one of the article covering the points highlighted

Glenmark – Will Innovation Pay? (12-04-2024)

I don’t remember the exact calculation

What I broadly remember is I extrapolated ( an optimistic scenario ) management commentary of strong growth in FY 25 ( 15 pc type or something, will have to revisit the concall ) and subtracted the GLS sales

But … I am not able to recollect clearly. Anyways, don’t go by that. One can still assume a 8-10 pc topline growth over FY 24 and almost NIL interest payments due to the sale proceeds ( post Tax ) received from the stake sale in GLS

Embassy REIT: Is this “Blackstone” promoted REIT is real diamond? (12-04-2024)

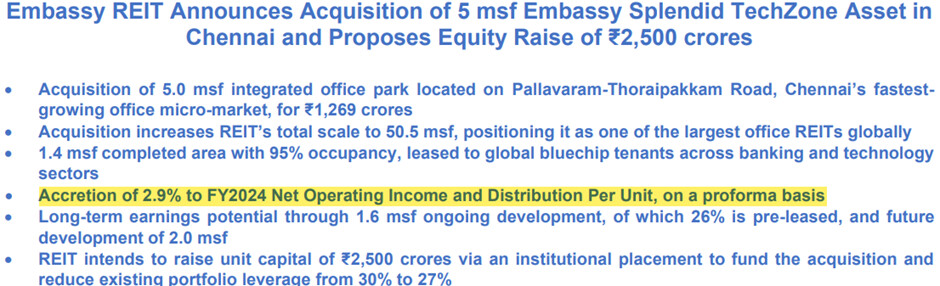

Embassy has recently announced the acquisition of an office park in Chennai, Embassy Splendid Techzone (ESTZ) from its sponsor. It has shared a press release and a detailed presentation for this acquisition. Highlighting here the grossly misleading disclosures in these.

To fund this acquisition, Embassy is looking to raise Rs2,500 crore via an institutional placement and it claims that post the placement and the transaction, this acquisition will result in a 2.9% accretion to FY24 NOI and DPU on a proforma basis.

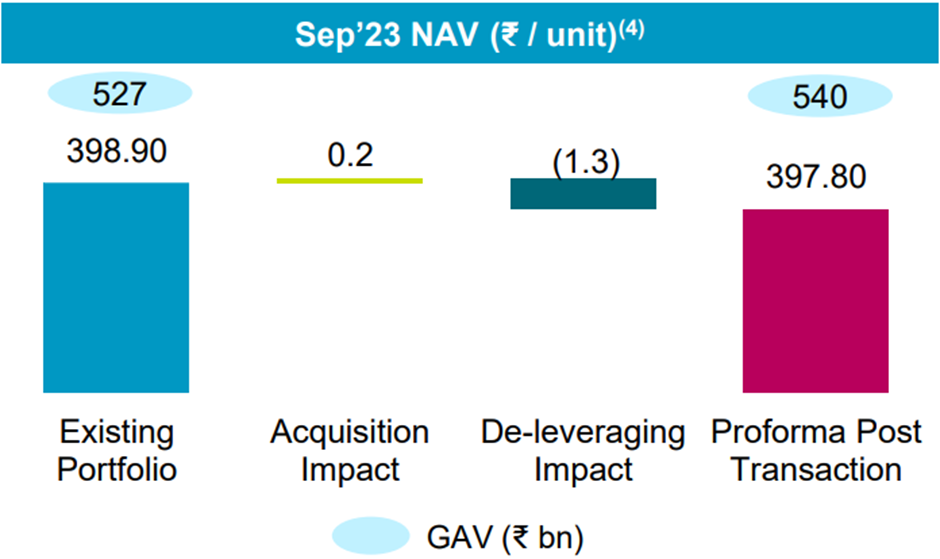

But from a long-term value creation perspective, the more metric is the impact this acquisition has on Embassy’s NAV, on which the press release mentions nothing. This aspect is disclosed only on slide no. 8 in the presentation and as expected the acquisition by itself will increase the NAV by only Rs0.2.

However, even these projections are based on highly aggressive assumptions. For the projected increase in NOI, DPU and NAV to materialize, Embassy’s manager has assumed that it will be able to raise the required capital from institutional placement at the then prevailing market price of Rs375.43 per unit. This is disclosed in the Notes to the slide no. 5 in the presentation.

Despite the well-known fact that institutional placements happen almost always at a discount to the prevailing market price as otherwise the investor has no incentive to participate in one, Embassy’s management has slyly mentioned this important assumption in passing in the presentation. Naturally, Embassy’s unit price has crashed 6% since the announcement of the acquisition and in all probability the placement will take place at a discount even to this crashed unit price. As a result, instead of this acquisition being DPU, NOI, and NAV accretive, expect this acquisition to actually lead to a dilution in these metrics.

I don’t think so that Embassy’s manager would have been unaware of these basic facts then it begs the question, why did the management proceed with this equity funded acquisition despite enough debt headroom being available. A quick back of the envelope calculation shows that even if the acquisition would have been fully debt funded it would have resulted in Embassy’s LTV inching up only to about 32% from the current 30%, which would be still lower than that of the most levered REIT, Brookfield India REIT, which has an LTV of ~35% and still be below the regulatory cap of 49% LTV.

Inviting views from experts in this field on this.

R Systems International (12-04-2024)

Is R System worth to consider at current valuation?

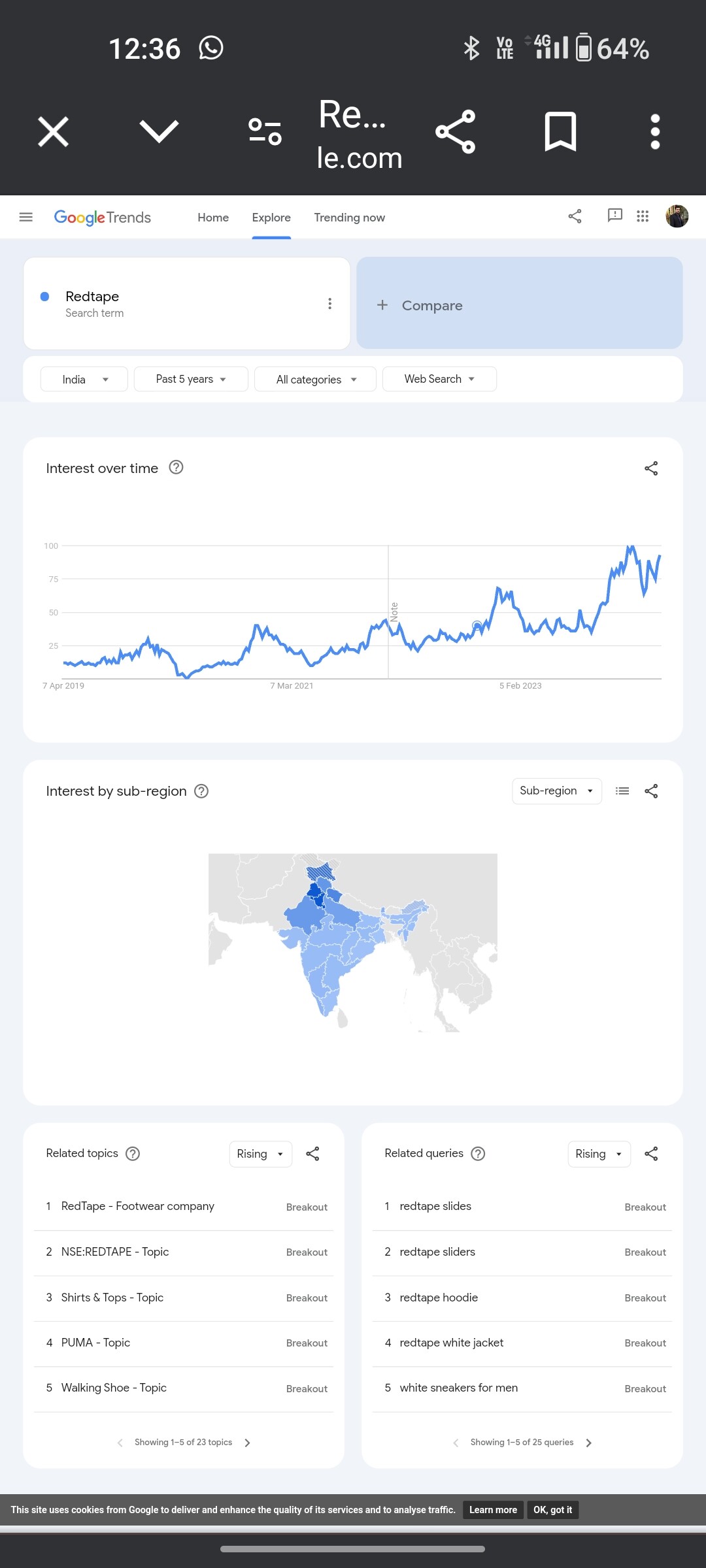

Red Tape Ltd. – The next fashion giant? (12-04-2024)

In addition to this if you check the Google trends, it is clearly indicating the Redtape search traction in last few years.

Tara Chand Infralogistic Solutions Ltd (12-04-2024)

1st thing 1st

PE shouldnt be the matric that you shohld be viewing this are high depreciating co. Look at cashflow

2nd thing how does it matter weather it is at SME or main board? Think of it this way if you wanted to buy Parle G but the same wasnt available in Dmart hence you bought the same from local vendor. How does this matter eod its the biscut (In this case business you are buying)

The business did 50 crores of Op. Cashflow last year on Mcap of 400 crores (12.5% yield)

The co. Is doing 170 cr. Of capex mostly towards renewable side where there is shortage of cranes

It can do another 40 cr. Of cashflow easily with better rental yield and good utilisation

Get out of price baisness if you are holding the business

There is nothing such as bear case scenario if you want to buy the business

If you have any bear case scenarios dont buy it simple

Maybe baised, DYD

List of Research Service Providers (12-04-2024)

Looking to create a list of RA’s and the kind of research they provide, which can be helpful to people to discover new analyst services. Based on my research found the following services. I could not find another discussion on the same topic. Hence posting here.

A few popular equity research providers.

https://katalystwealth.com/

https://www.asksandipsabharwal.com/

https://aurumcapital.in/