As of now i have no holding , only tracking.

Posts tagged Value Pickr

Tara Chand Infralogistic Solutions Ltd (12-04-2024)

@VIMAL_AGRAWAL @Meetkatrodiya @Ashar_Mann

The order book is ~ 325 Cr.

Let say FY Revenue comes out 170 Cr.

How much order they would be left with at start of FY25 ?

I’ve started tracking recently but before i make a move ![]() CMP doubled just in a 1 month from 144.

CMP doubled just in a 1 month from 144.

I find tarachand to be good name with bright prospects for few more years.but Before i give into FOMO. I wish to study & understand what could be prudent approach to hook up with ? ![]() . Let it migrate to mainboard or wait for a blimp ? What could be Base/Bear case scenario ?

. Let it migrate to mainboard or wait for a blimp ? What could be Base/Bear case scenario ?

Market cap is ~400 Cr.PE~34, CMP ~ 5.03 times book value ![]()

Aditya Birla Fashion and Retail Ltd (12-04-2024)

Looks really interesting! Just want opinion of the community as to which business are you more interested in? Tried reading views of a few and most are excited about ABFRL’s high growth strategy and brands which will benefit from premiumization but personally I am more interested in Madura’s part of the business. The reason? It is luxury retail segment. ABFRL, accoriding to the management will be focusing on value segment which has become cluttered in the past 3 years. Every other person wants to enter the value clothing market. Snitch is becoming famous day by day, then there are brands like Zudio, Zara, H&M, reliance is also a new entrant in this segment. I think it will become really hard for brand to establish itself in this segment. But on the other side, Madura owns almost all the luxury clothing retail brands and this segment has close to no competition as customer preferences usually don’t change based on prices in this segment. But it remains to be seen that what valuation of Madura will be offered for listing in the market.

Just my view… Open to criticism

Disc.- Tracking since 2 years but never got the confidence to invest

Jubilant Ingrevia – Life Science Ingredients (LSI) (12-04-2024)

Jubilant Ingrevia has recently inaugurated an innovative facility for Diketene Derivatives in Gajraula, Uttar Pradesh. This plant will significantly enhance the company’s production capacity by adding 2,000 tonnes per annum (tpa) for manufacturing high-value esters.

The expansion into diketene derivatives represents a strategic move by the company to tap into new markets, particularly in the US and EU regions. These derivatives are poised for substantial growth, positioning them as a key segment within the company’s specialty chemicals portfolio.

With this facility,the organisation is not only bolstering its existing offerings but also signalling a shift in strategy towards capturing emerging opportunities in downstream derivatives. The company is committed to further strengthening its presence in this segment, with plans to introduce new derivatives in addition to the existing ones.

This forward-looking approach aligns with the corporation’s long-term strategic objectives, as it aims to build an advanced product portfolio and solidify its position as a leader in the diketene derivatives market. With innovation and expansion at the forefront, the company is poised to capitalise on evolving market trends and deliver value to its customers worldwide.

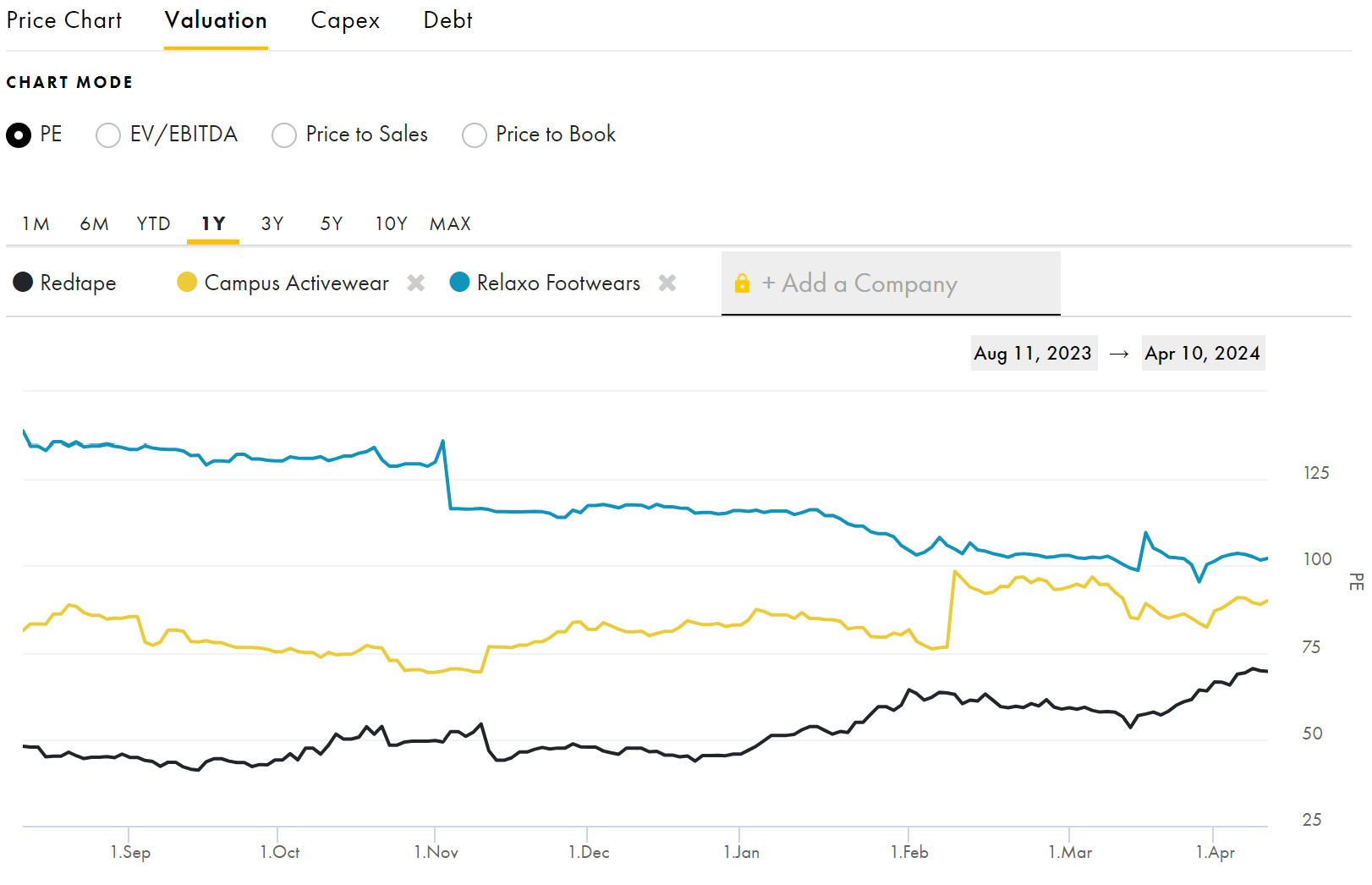

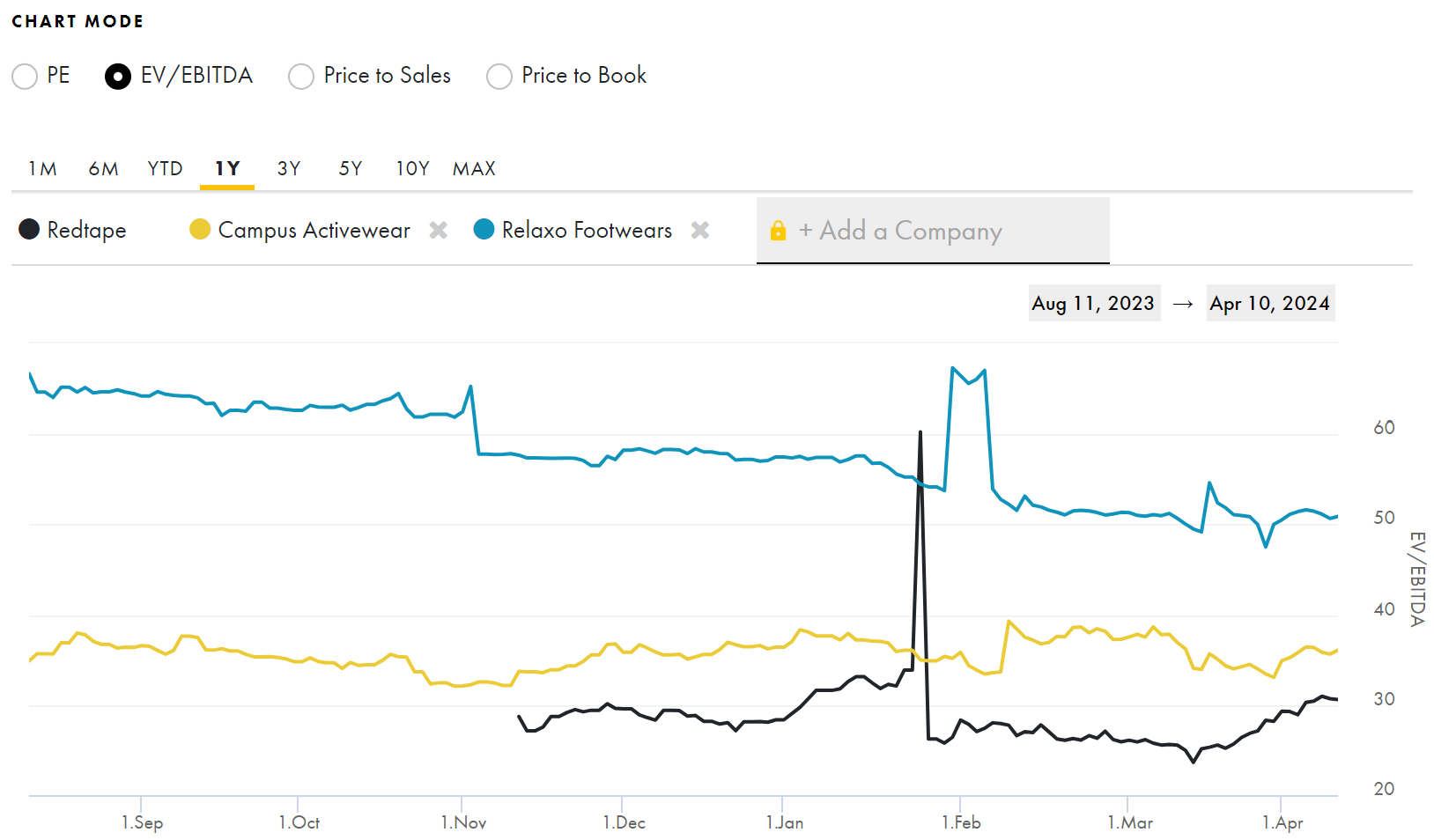

Red Tape Ltd. – The next fashion giant? (12-04-2024)

Yup, I would agree to disagree. Redtape is the most efficient and fastest grower of the lot, We shouldn’t forget with growth comes earnings which ultimately improves valuations. I am expecting the upcoming qtr to be the best one so far, 950-1100 isn’t too distant.

ROCE

Redtape – 44.8%

Relaxo – 11.8%

Bata – 19.6%

Campus – 23%

Metro Brands – 24.3%

Sales QoQ | YoY

Redtape – +90% | +29%

Relaxo – (-) | +4.6%

Bata – +10% | +0.33%

Campus – +82% | +1%

Metro Brands – +14.3% | +6%

PE ratio

Redtape – 58

Relaxo – 102

Bata – 61

Campus – 89.5

Metro brands – 87

What’s fascinating here is the realization of valuation disparity by the market, It is evident how the competition is seeing a fall in premium valuations and how Redtape is being taken to there.

Smallcap momentum portfolio (12-04-2024)

Not sure I understand the question fully. Can you please re-phrase?

Websol energy system ltd (12-04-2024)

The board has approved the issue of 12,10,000 convertible warrants on preferential basis to Promoter Group at Rs.530/Share. So, infusion of Rs. 64.13 Crs for Approx. 2.8% of total shares. Interesting.

Aditya Birla Fashion and Retail Ltd (12-04-2024)

Every consumer company posting highest ever or at least pre-covid level results and here is this company. Management is still blaming Macro economic environment and discretionary income of population for its losses! Also, management is mentioning that slowdown in growth is also due to the lack of demand from rural tiers. Can’t understand if it makes any sense for a mid to high segment clothing retailer to blame rural population for its bad numbers.

I guess the main problem i.e. unit economics needs to be fixed before anything.

Disc. Not invested

Suggestion on mutual fund SIP (12-04-2024)

Thanks for information. I will make changes to portfolio accordingly