Exactly, what i find very weird is how the company can post such great numbers in a matter of a couple of quarters after new management takeover? The previous management has been with the company for a long time and how could they not forsee this growth?

Posts tagged Value Pickr

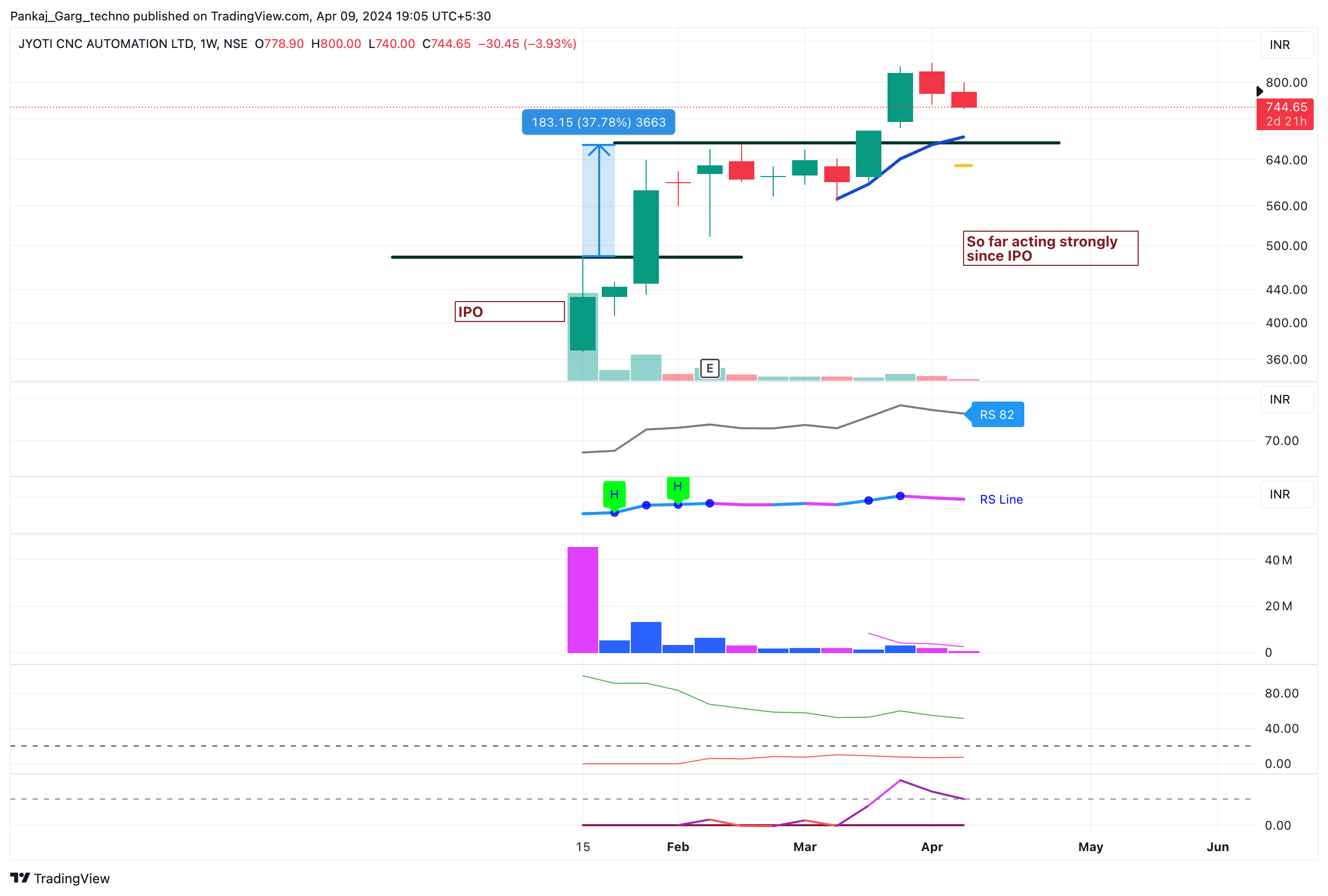

Jyoti CNC Automation Ltd (09-04-2024)

-

Jyoti CNC Automation Limited is one of India’s largest CNC machine tool manufacturers.

-

The Company’s range of products that includes CNC Turning Centres, Turn-Mill Centers, Vertical Machining Centers (VMC), Horizontal Machining Centers (HMC), and advanced 5-axis Machining Centers, along with solutions for Industry 4.0 and Artificial Intelligence (AI).

-

Vertically integrated company with in-house manufacturing of machine components such as spindles, tool-changers, pallet changers, rotary tables and universal heads in-house. The company has its own R&D Centers, Foundry, Machine Shop, and Sheet Metal Unit. Also has in-house design capabilities.

-

Focus on R&D with dedicated R&D facilities at Rajkot and Strasbourg.

-

diverse customer base. Some of the marquee customers include ISRO, Brahmos, Harsha Engineers, Bosch, Tata Advanced Systems etc.

-

Exports constitute ~ 40% of revenue.

-

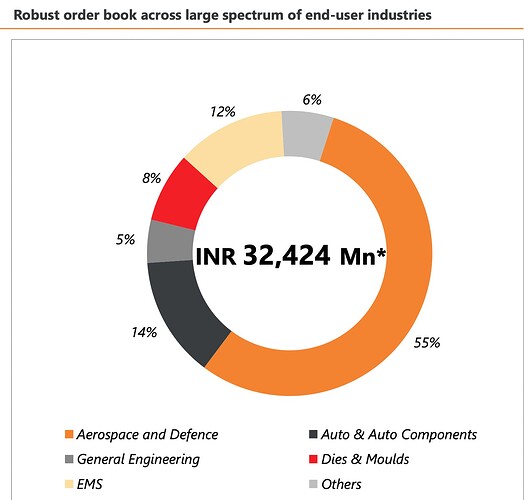

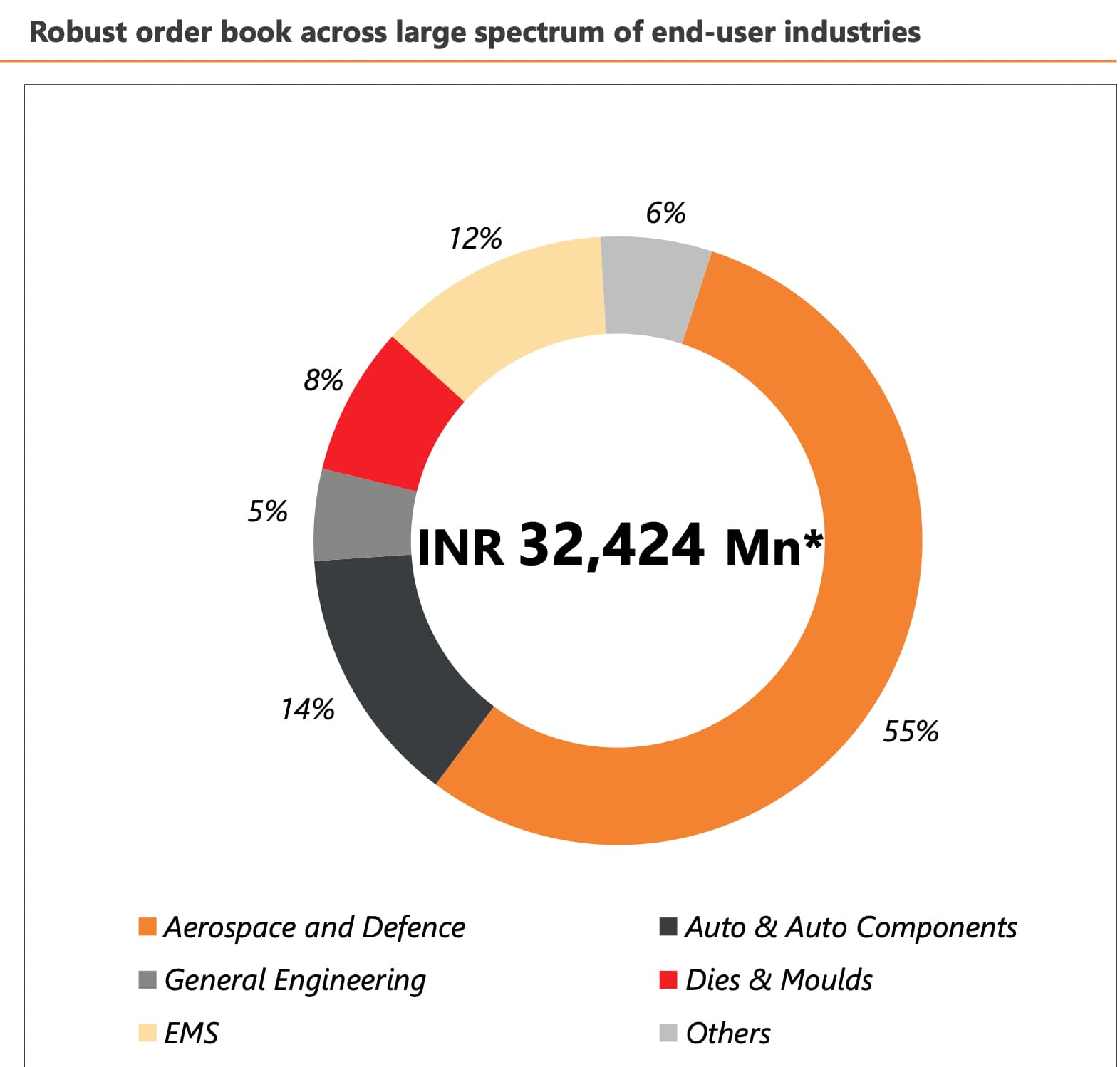

Catering to Aerospace, Defence, Auto, EMS, Dies and Moulds and General Manufacturing Industry

-

Orderbook as on 31 Dec 2023:

-

Vertically Integrated Company

Industry Size:

-

As per management, India consumed $3 billion worth of CNC machine last year (approximately 24,000 crore). of this 65% was imported while 35% was domestic over the next 5–7 years the consumption is expected to grow at 20%.

- The company eyes that the proportion of imports will decrease in the next 5-7 years that is import substitution is likely to happen. Secondly, the market itself is growing at 20%.

-

85% of the total market is metal cutting and 15% metal forming. Jyoti CNC status metal cutting

-

Overall market the entry level is domesticated 80–85% is domestic while in high end machines 90% is imports. the company is focusing on this high end of the market, where competition is mainly from Germany and Japan.

-

The Company operates in a niche growing sector. But a good business is not always a good investment if the valuation is not in favor.

I think this is a good stock to discuss on this forum

Disclosure: Tracking position

Macpower CNC Machines: Manufacturing a Strong Growth? (09-04-2024)

Macpower Cnc: Notes from Arihant conference

Margin levers: – Backward Integration (largest driver of margins)

Services → high valued machines + defence machines have a sizeable service component as well

Operating Costs → co to aim to reduce operating costs to 15% from current 17%+ (revolutionary in Indian mfg)

As avg realization continues to improve from 20lacs, over the next 5 years co aims to touch 25% margins!

Expansion: – Starting May, co will be on track to utilize 2000 machine capacity for production – also with additional debottlenecking co will be able to manufacture upto 2200 machines

Over the next 5 years company plans to increase capacity by 2000 machines every year to reach 10000 machines capacity in 5 years (from 1500 in FY24)

Capex: – 10cr to take current capacity of 1500 to 2000.

100cr for 2000 machines in the new set up (reach 4k machines capacity) – 15cr additional capex every year to add 2000 machines every year (depends on demand as well).

Other Highlights: – no new player in the last decade, present 6-7 players will continue to compete – Due to govt focus to take manufacturing to 25% of GDP from current 17% loans have become easy, subsidized with interest rate waivers and tax waivers → this is leading to import substitution

Very conservative management.

Hitesh portfolio (09-04-2024)

@hitesh2710 Dear Hitesh Sir, do you pick stocks based on sectoral tailwinds or stocks benefiting from the current popular themes ( like EV, Green Energy etc. ) , would be interesting to know the future themes that you are bullish on…

Walchandnagar Industries | Return of a Golden Era (09-04-2024)

ISpA Welcomes Walchandnagar Industries Limited as a Platinum Sponsor for the Indian DefSpace Symposium 2024.

The 2nd Edition of the Indian DefSpace Symposium will take place on 18-20 April 2024 at Manekshaw Centre, New Delhi, India.

Polycab India ~ Connection Zindagi Ka – W&C, FMEG and EPC Player (09-04-2024)

Hey Everyone, while I don’t have insights related specifically to polycab specifically, I’ve compiled some data of 20 Listed Wires & Cables companies and shared some big insights from an Industry overview perspective

if you’re going to invest in a co’ might as well keep an eye on what’s up with the rest of the players.

Hope you find this useful

Disclosure : NOT Invested | Tracking.

Finolex cables ltd (09-04-2024)

Hey Everyone, while I don’t have insights related to Finolex Cables, which is obviously having its own set of issues as we all know. I have compiled some data and tried to share the big insights from an Industry overview perspective on the Power cable companies

Disclosure : NOT Invested but Tracking

Sintex Plastic Ltd (09-04-2024)

The insolvency regime prioritizes the interests of creditors and hence, the interest of minority shareholders of an entity undergoing CIRP remains largely ignored. They occupy the lowest position in the ‘distribution waterfall’. They don’t have any representation in the CoC. The minority shareholders of DHFL and Sintex Industries suffered huge losses when the resolution plans suggesting for the delisting of the entities were approved by the NCLT and they were left with no recourse.

The public shareholders are denied a fair bargain by providing an exit opportunity at a market-determined price and are instead left at the mercy of the Resolution Applicant (RA).

The provision that existing public shareholders be given exit opportunity at a price which equal to or more than what is offered to the promoters is of little help considering that promoter’s equity is often written off, making it highly unlikely that public shareholders will receive any value. Further, in insolvent liquidations, there is no liquidation value attributable to equity-holders.

Another amendment in the Securities Contracts (Regulation) Rules, 1957 (SCRR) in 2021 mandated a minimum of 5% public shareholding for an entity to remain listed post-CIRP. Such a mandate disincentivises the new entity post-CIRP to be listed and hence, they go for delisting which again is against the interest of minority shareholders.

Therefore, once a RP is approved for a listed company, the possible scenarios are:

-

Liquidation of the company in which case they get virtually nothing;

-

Continuation of the company with or without listing, based on the resolution plan which largely results in dissolution of shares again squeezing out the shareholders.

In both the scenarios, the existing public equity shareholders get squeezed out and usually end up with almost nothing.

Need for protection of minority shareholders

One could argue that the treatment of such shareholders is justified if they chose to remain interested in the company even when the company had reached at that stage. While this reasoning is not misplaced, it is also important to consider that the shareholders are often misled hoping that they might end up getting a better deal.

The minority shareholders argue that they don’t have much say when equity owners run down the company. Further, most of such minority shareholders are retail or small shareholders who don’t possess the awareness and the level of information to make a timely decision.

Another concern is that the CIRP can be triggered on a mere default and the company need not be balance sheet insolvent.

The SEBI consultation Paper

Addressing the concern of the minority shareholders, SEBI came out with a framework for protection of interest of public equity shareholders in case of listed companies undergoing CIRP. The key recommendations are as follows:

Opportunity for Public Equity Shareholders: Public shareholders will have the opportunity to acquire equity in the new entity that is formed post CIRP. Promoter and promoter group, KMPs etc. would be excluded while identifying such public equity shareholders.

Minimum and Maximum limit: The acquisition of equity by public shareholders will be minimum 5% and a maximum of 25% of the capital structure. The pricing terms for this acquisition will be the same as those agreed upon by the resolution applicant.

Mandatory Delisting on failure to achieve minimum Shareholding: For the company to continue as a listed entity, at least 5% of the fully diluted capital structure must be held by public shareholders. If the resolution applicant fails to achieve the 5% public shareholding, the company will be delisted, and the consideration received from public equity shareholders will be refunded.

Exemptions from Delisting Regulations: The recommendation also states that exemptions from Delisting Regulations will be applicable only in cases of liquidation or if the public equity shareholding remains below 5% of the new entity after the offer.

Source: Out of Focus: SEBI’s Distorted Lens on Shareholder Protection in the IBC Landscape – CBCL

Sintex Plastic Ltd (09-04-2024)

Let me know if anyone has access to this below:

From investor’s paradise to graveyard: the tragic tale of Sintex

Emerald Insight

https://www.emerald.com › content › doi › full › pdf › ti…

](From investor’s paradise to graveyard: the tragic tale of Sintex | Emerald Insight)

JTL Industries – Fast Grower at an inflexion point (09-04-2024)

Company is forward looking and it’s operations indicate the same.