Q4 is typically strong for the company as said by Mr Surana to CNBC. They expect 10-12% growth medium term with prices of certain compounds increasing.

Posts tagged Value Pickr

DDev Plastiks Industries – A Smallcap Gem (31-03-2024)

Company having peak operating and gross margins. Any understanding of margins and visibility. How much of it is cyclical and how much has risen structurally.

Else industry witnessing good growth due to power capex

DDev Plastiks Industries – A Smallcap Gem (31-03-2024)

74.85% is “officially” held by promoters under the promoter category.

Rest held by Almond Polytraders Pvt Ltd – 8.23% and

Liable Textiles Pvt Ltd – 2.81% in public

Totaling to about 85.89%.

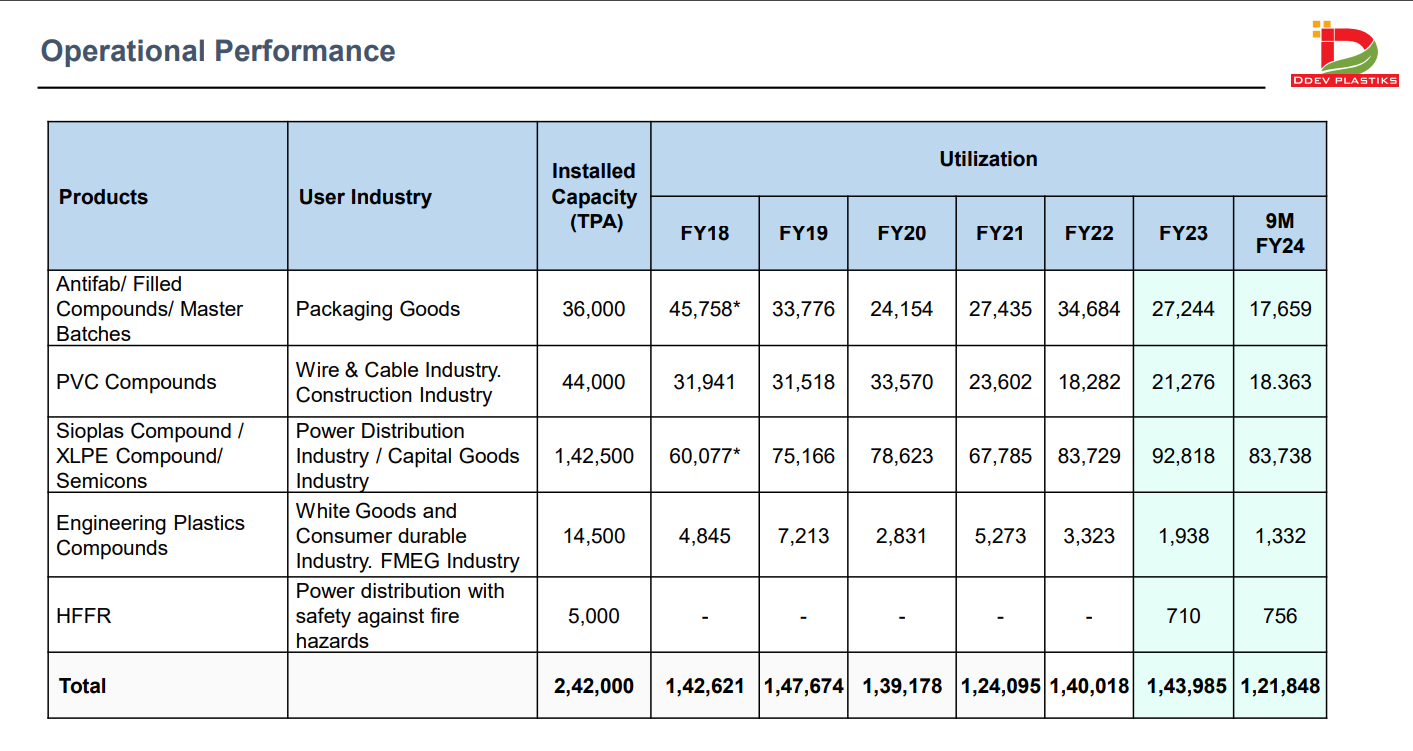

As per doubling capacity what I understand is that the entire industry is not in a good shape right now, however the promoters believe the industry will recover late 2024 and should start blooming after 2026 as predicted by many experts in this space so they are keeping production capacities ready if demand grows.

They have minimal debt and a strong balance sheet so picking up cheap debt wont be a problem to them.

To add CRISIL has also upgraded their rating to A/ positive from stable

I hold small qty for tracking purposes

MSTC Ltd.: Growth through to E-Commerce (31-03-2024)

Let me know if this link works. Thanks

DDev Plastiks Industries – A Smallcap Gem (31-03-2024)

I have few queries. How promoters and related party are holding 85% stake? It can’t be more than 75%. What is the catch?

And if capacity utilisation is 52% then I fail to understand rationale behind doubling capacity by 2025.

Will be obliged if anyone can clarify.

Jindal saw – Another beneficiary of India’s growth story (31-03-2024)

Basically Jindal Saw is manufacturing steel pipes. So isn’t it fair to compare it with likes of JTL industries and Jai Balaji? Both of them trade at much higher valuation then Jindal Saw. What could be the reason?

MSTC Ltd.: Growth through to E-Commerce (31-03-2024)

Hello

Can you reupload the writeup the link has expired

E2E Networks Ltd – Listed small Cloud computing player (31-03-2024)

Analogy

- Manufacturing plant → datacenter

- more capex → more datacenters → more revenue

- workers → software engineer building the platform for customers.

- currently high margins as less players in market.

Pros

- early mover advantage.

- building datacenters takes time ( time barrier for new players)

- data localization is the future

- booming Indian software companies/groups/ individuals will use E2E.

Cons

- new players with deep pockets can disrupt.

- only meant for small size companies.

Notes:

With current hype of datacenters, AI n semiconductors, valuations has no limit.

DDev Plastiks Industries – A Smallcap Gem (31-03-2024)

One important point that you missed is that the promoter along with their related parties hold more than 85% stake in the company.

This is the main reason why institutional investors are not interested in this stock due to low public float.

Also if one looks at the capacity utilization it is about 55%