Thank you Mudit!

I haven’t been doing much research on stocks since last 2 years and I feel the market is pretty heated.

My whole position depends on how the capex cycle pans out. So iam sitting and waiting.

Iam trying to be a more regular contributer here! So lets see how that goes.

Posts tagged Value Pickr

Sandeep’s Long Term Concentrated smallcap portfolio( Learnings and Mistakes) (29-03-2024)

Punjab Chemicals & Crop Protection Limited (PCCPL) A Clear Runway Ahead! (29-03-2024)

@harsh.beria93 can you share references of 40-70% price decline in case of peers.? And whats the reason for better pricing given destocking and subdued export is faced by all downstream player including UPL.

Current Portfolio for 6 months – 1 year (29-03-2024)

You have some great investments, i would say. But if i could short out some problems please give All Cargo another look, i was also holding it from 65 level but last quarter result disappointed and the demerger case also disappointed me. As the company that will do business in India is literally use less, and i am also planning to buy when ever the foreign one get listed after the demerger.

for beter reference you can read the CRISL Report

Paradeep Phosphates – A merger to make a mammoth! (29-03-2024)

@TheRInvestor sorry missed this… still new to the portal. Are you referring to the 2023 task force setup to relook at SSP production and ways to boost it again?

If yes, it plays to Paradeep’s strengths as it has SSP in its portfolio

JTL Industries – Fast Grower at an inflexion point (29-03-2024)

CFO upto FY 21 was in the negative due to high debtors ageing. Starting FY22 and including H1 of FY24, CFOs have turned positive and showing improving trend along with drastically reduced debtors ageing.

Now that the financial year is effectively over, the Q4 financials will be a deciding factor.

Zenith was allocated warrants in 2022 and shares allocation prior to ED action was the legal norm. The timing of the events seems unfortunate.

Weakness in a rising market only raises questions of any possible surprises to retail investors.

Smallcap momentum portfolio (29-03-2024)

@theengineer2012 Yes, this is what I continue to use. If you are asking in reference to my previous answer, I was suggesting that as a means to quickly starting a momentum pf.

You can embellish it with lot of other parameters to fine tune it.

Trust this is clear.

Unemployed investors portfolio (29-03-2024)

Any company available at present, based on your criteria, with industry tailwind. Thank you.

Punjab Chemicals & Crop Protection Limited (PCCPL) A Clear Runway Ahead! (29-03-2024)

Punjab came with very subdued results (-18% sales decline, -44% EPS decline). However, these nos were much better than most other technical manufacturers and they have only witnessed 8-9% price decline vs most generic cos facing 40-70% price decline. This has meant that they actually improved gross margins this quarter.

They seem to have invested quite a bit in new product development and are confident of scaling up 7-8 new molecules + intermediates in the next few quarters. Concall notes below.

FY24Q3

-

Export demand is subdued (high channel inventories, adverse weather, customers building inventory closer to season). Expect revival by Q3 of FY25 (so about a year)

-

Gross margin improvement is due to process re-engineering leading to better raw material efficiency + product mix. Make higher margins in specialty intermediates for pharma

-

Of the 3 planned launches this quarter, have got registration for 1 product in EU (different from Australian product; prosulfocarb) and started supplying commercial quantities. Other 2 registrations are expected in 2024 and commercial supplies should begin in Q3/Q4FY25. Total business from these 3 products are 100-150 cr. once all registrations are done

-

Intermediates: Supplies have started for 1 pharma intermediate (currently for EU market, high value, should get US registrations in 1-2 years). 2 other samples have been approved and commercial quantities will start in Q3FY25. These 3 intermediates (2 pharma + 1 agchem) will contribute 150 cr. in 1-2 years

-

So 100-150 from agchem + 150 from intermediate ~ 300 cr. from products being commercialized now

-

Have got into a long-term agreement with agchem customer for 1 agro product which will be launched in beginning of 2025

-

In 9MFY24, have not seen major volume decline. So probably 8-9% price decline (which is quite good compared to generic technical that have seen 40-70% decline)

-

FY25: Existing products should see 10-15% volume growth as volume have reduced in FY24 due to high channel inventory + there will be new product contribution in range of 200-250 cr.

-

Expect 10-15% growth in near term which will then ramp up to 25-30% in 3-5 years

-

In current portfolio, 2 products are patented by Japanese innovator, 4-5 other products are generic but in a couple of them, Punjab has 80-90% of market share

-

Will start working on a new production block in Derabassi in April/May 2024

-

Hydrogenation added to capability

Disclosure: Invested (position size here, no transactions in last-30 days)

Sula vineyards – pioneers in indian wines (29-03-2024)

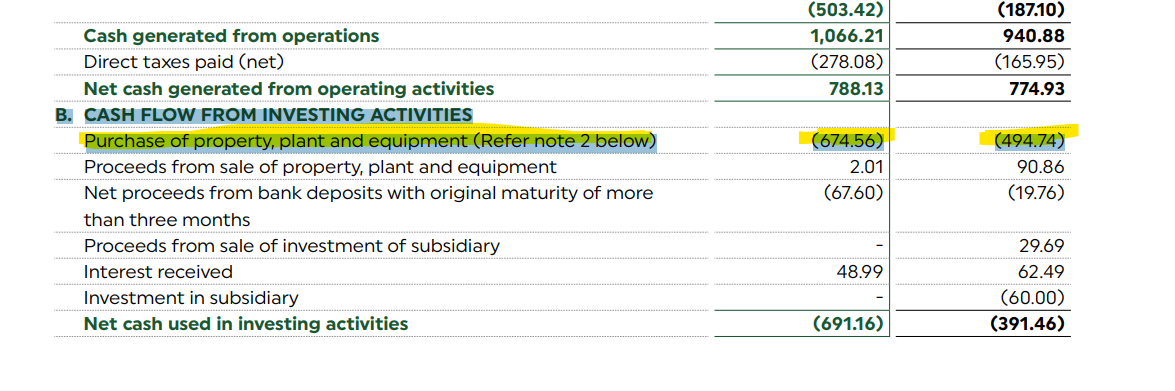

Hi I have QQ -For the below highlighted figure ,is the Purchase of PP&E is a real purchase of the plant and machinery or its just an general raw material and repairing of the machinery .

I want to understand like are they purchasing PP&E for growth so that they can increase production capacity Or its just a maintenance no Capacity increase .

Looking at the balance sheet ,it seems to be main reason behind reducing free cash flow.

Time technoplast (28-03-2024)

Time Techno seems to have hit a purple patch in terms of delivery (17% sales growth, 49% EPS growth) and investor confidence. Its hard to believe that the co was available at 3x PE during COVID fall! Management now seems very confident of exceeding 15% growth in the medium term. Concall notes below.

FY24Q3

-

Targeting 15%+ sales growth in next 2-3 years (10-12% packaging + 30% composite)

-

Established product growth of 15% was driven by polyethylene pipe businesses (expect 25% growth in pipe business in next 2-years)

-

9M debt reduced by 65 cr. and will reduction will exeed 100 cr. in FY24. Without any further divestment, debt will reduce to 450 cr. and interest cost will reduce to 50-60 cr.

-

Capex : 45 cr. (23 cr. towards established products + 21 cr. towards value-added products). Reduces FY24 capex to 175 cr. (vs earlier planned 200 cr.)

-

Middle east disinvestment : 50% business for $25 mn (13-14% EBITDA margin, ~350 cr. FY24 revenues; include Dubai, Bahrain and Saudi; excludes Egypt plant; out of 1.4mn IBC capacity in Middle East, divesting 0.1mn IBC capacity). Net of taxes, will get ~175 cr.

-

Target divestment of 125 cr. of non-core assets (earlier 100 cr.) and no non-core assets by FY25. First transaction of 26.5 cr. will be used for debt reduction

-

In IBC manufacturing, leader in 7 out of 10 countries. Are not leaders in US. Total capacity: 1.4mn abroad (60% utilization) + 0.5mn India (75% utilization). 60% IBC sales comes from overseas and 40% from Indi a

-

In CNG cylinders, will target auto segment after next capex cycle in FY25

-

CNG composites : capex of 125 cr. (capacity increase from 480 to 1,080) can generate revenue of 800-850 cr.

-

Targeting 1500 cr. revenues from composite in next 3-years (vs 500 cr. in FY24)

-

Oxygen cylinders: started registering process with army and navy authorities. Fungible capacity with LPG

-

LPG Type-IV cylinders: Only Supreme and Time techno are making this (combined capacity of 2mn)

Disclosure: Invested (position size here, no transactions in last-30 days)