Please do add sources like link to videos or articles when posting some thing like this, this builds credibility and allows us to check the point of view of management

Posts tagged Value Pickr

Promising Micro Cap and Small Cap Companies- Pil Italica Lifestyle Ltd (28-03-2024)

I want to share report on Promising Micro Cap and Small Cap Companies.

Your constructive criticism is solicited.

Regards

Avanti Feeds (28-03-2024)

A Whistleblower on the Rot in India’s Shrimp Exports

The senator move is after this whistleblower report

Caplin Point Laboratories (28-03-2024)

Caplin Steriles Limited (Caplin), a Subsidiary Company of Caplin Point Laboratories Limited has been granted final approval from the USFDA for its ANDA Ketorolac tromethamine Ophthalmic Solution 0.5% (eye drops), a generic therapeutic equivalent version of (RLD), ACULAR Ophthalmic Solution of Allergan Inc.

Jasch Industries Ltd – value unlocking possible? (28-03-2024)

Does anybody know if this falls under the “Uber Cannibals” framework?

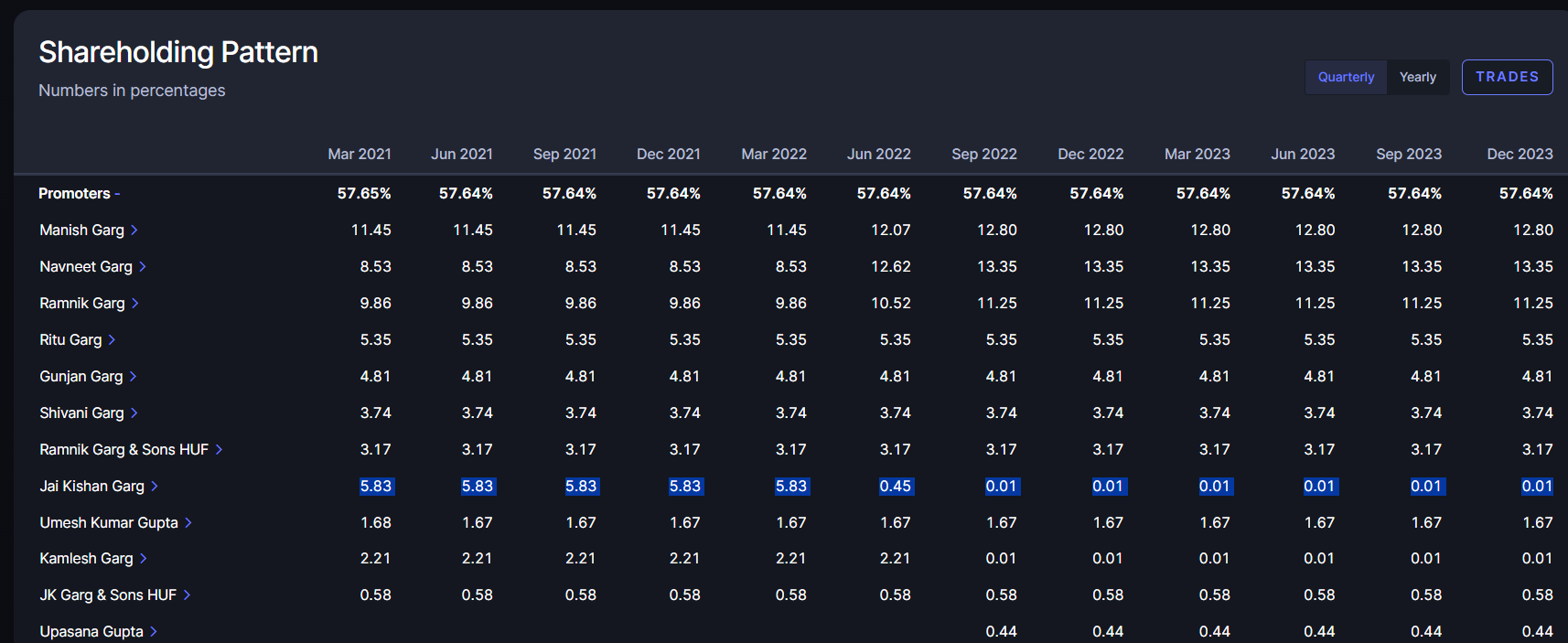

Jasch Industries Ltd – value unlocking possible? (28-03-2024)

Navneet Garg buying out Jai Kisan Garg

IBC referred Cases: Value investing or Value trap? (28-03-2024)

So, just coming basic point, the company has defaulted and not able to honour its obligation. In more than 95% of the cases, Financial creditors/opertional creditors need to take waiver on their claims. In simple finance, when lenders take waiver (which mean cashflow value/assets value of company is not able to meet debt obligation), equity value is nil. In that scenario, why would rationale investor offer equity value in such IBC cases to equity holders?

In my understanding, only two reasons can justify equity value.

- Accumulated losses can be utilised as tax shield in future by profit making new investor in case they merged IBC referrred company

- In case of listed company, acquisition of IBC give indirect listing route to new investor (after merger of existing business, something similar to Orchid Pharma and Bhushan steel post Tata group acquisition).

In these situation, 99% of resolution plan have following clauses:

- Full writedown of equity owned by previous promoter group

- 90-99% equity value wirte-down by previous non-promoter group shareholding

- Some stake being given to financial creditor for waiver of claim

Subsequently, equtiy share face value would be consolidated to previous value. So a minority shareholder holding 100 shares of Rs 10 face value each (Total face value Rs 1000), would end up on 90% write down 100 share of Re 1 each (Total Face value 100). Subsequently, share capital would have consolidated face value of Rs 10 each resulting in 10 shares of Rs 10 each (Total face value of Rs 100).

Now when the scheme is implemented, very few shareholder would have shares which are available in their demat account. Someone holding 1,000+ share only would be 10 shares now. Furtther, the new listing approval and allotment also take some time. During that period, we she major volatility in such shares. I would strongly advise investors to understand whole events timeline and cautiously look at investing during these volatile period.

Enclosing certain example of volatility during that period.

Orchid pharma: 24 July 2019 price Rs 5.45, delisted, and post corporate restucturing (IBC approval resolution plan) reslited on 6 Nov 2020 Rs 20.75. Price went up from Rs 2527 per share on 1 April 2021, almost 100x during 5 months with very limited volume of 1,000-4,000 shares traded per day. By March 2022, share price declined to Rs 282, almost 89% decline.

Same pattern can be observe from Ruchi Soya (Now Patanjali) and Alok textile.

The biggest risk while investing in these company at very low price, the reoslution plan may provide for delisting with complete write down of old equity capital. In such situation, one has write off investment one hold in such companies. Probability of such incidence would be in very high (say more than 50-60% cases). Given such outcome, I would sugest every one to careful and not carried away by just price increases. It would be very difficult even during upswing to exit from such stock in my limited undestanding.

IBC referred Cases: Value investing or Value trap? (28-03-2024)

while whatever you have shared is facts, all this like you said has no significant weight on the acquirers since they clear all amounts/defaults according to their resolution plans.

There is no further demand or scrutiny which can be taken forward by existing or new creditors regarding the past once the NCLT has approved the resolution plan, there maybe certain cases of plant closures or shutdowns which may have been done in the past due to environmental issues, but i dont think so there can be anymore demand on the funds side of things once the rp is approved.

keeping it simple again, one would only invest if they see value, all these transactions would for sure be in mind before becoming a prospective resolution applicant. Regarding the listing, maybe yes, maybe no, i dont think that plays any part in this discussion, because we see acquirers coming in through cirp route constantly, so no point in going against the facts

it would be very helpful if you could shares more problems which can be faced by the acquirers, it would maybe add to my base since whatever CIRP cases i am tracking once the mgmt changes/changed, the only thing that changed were numbers (sometimes for the worst), efficiencies (increased) and business clarity.

lastly, i completely agree that life is not simple, you need to measure the odds and play it in your favour. Strictly keeping risk to reward in mind, till now IBC has been great for me, maybe thats because i have been able to keep it simple (its not easy for sure) by following change, or maybe its beginner’s luck.