They already have high debt(considering the promoters have other real estate businesses, and might be leveraged to large extent on that side, I would consider existing or future debt for the listed company as much riskier), if they can sell the Goa hotel to execute planned screen growth, i think it can play out. From the numbers in last 2-3 quarters, I can see they have unit economics in place already. As long as they get rid of debt and by better capital allocation , I think this probably will do well.

Posts tagged Value Pickr

Ujjivan Financial – Small Finance Bank (27-03-2024)

As per my understanding, Idfc and idfc bank have got approval to hold shareholders meeting which is on 17th May. Post the shareholder approval, they will have to file final application with Nclt.

In case of Ujjivan, the above process is all done and the final order is reserved. So all that’s pending is getting the final judgement order from Nclt. Though I agree Nclt has been slow in case of Ujjivan reverse merger

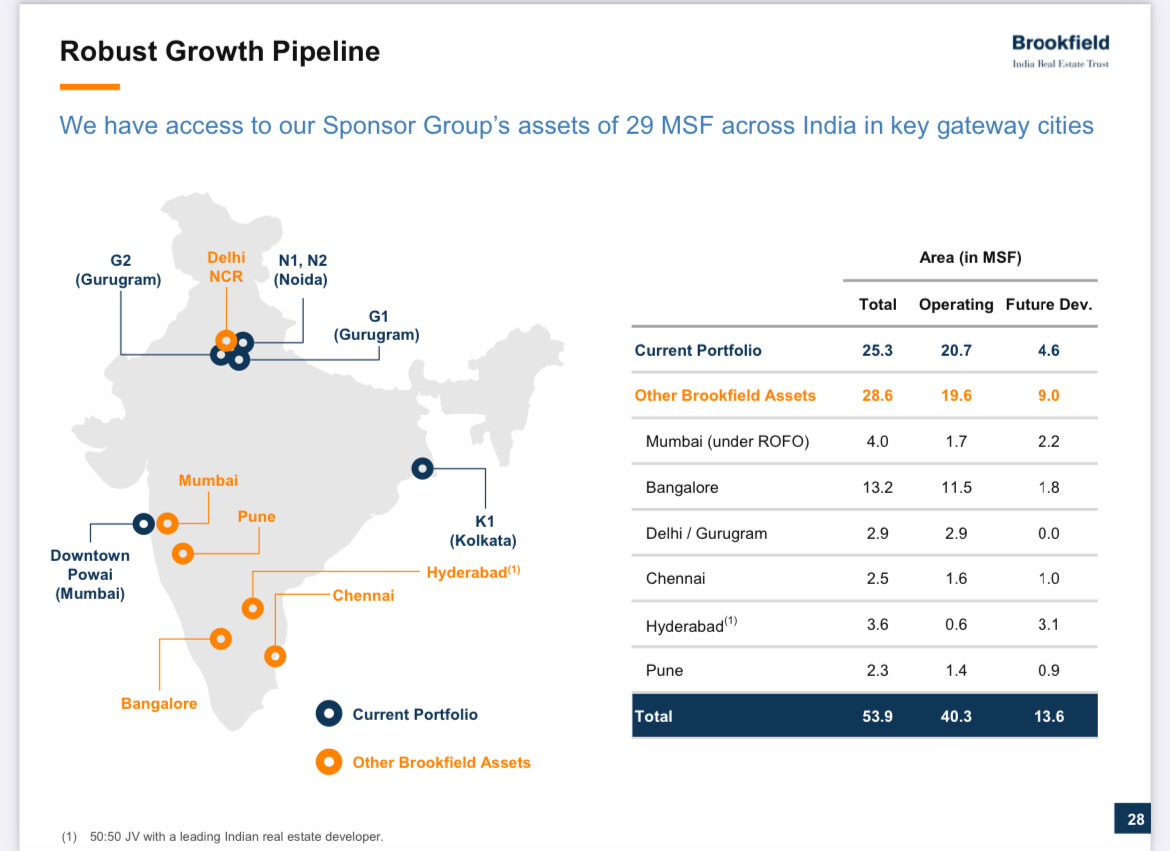

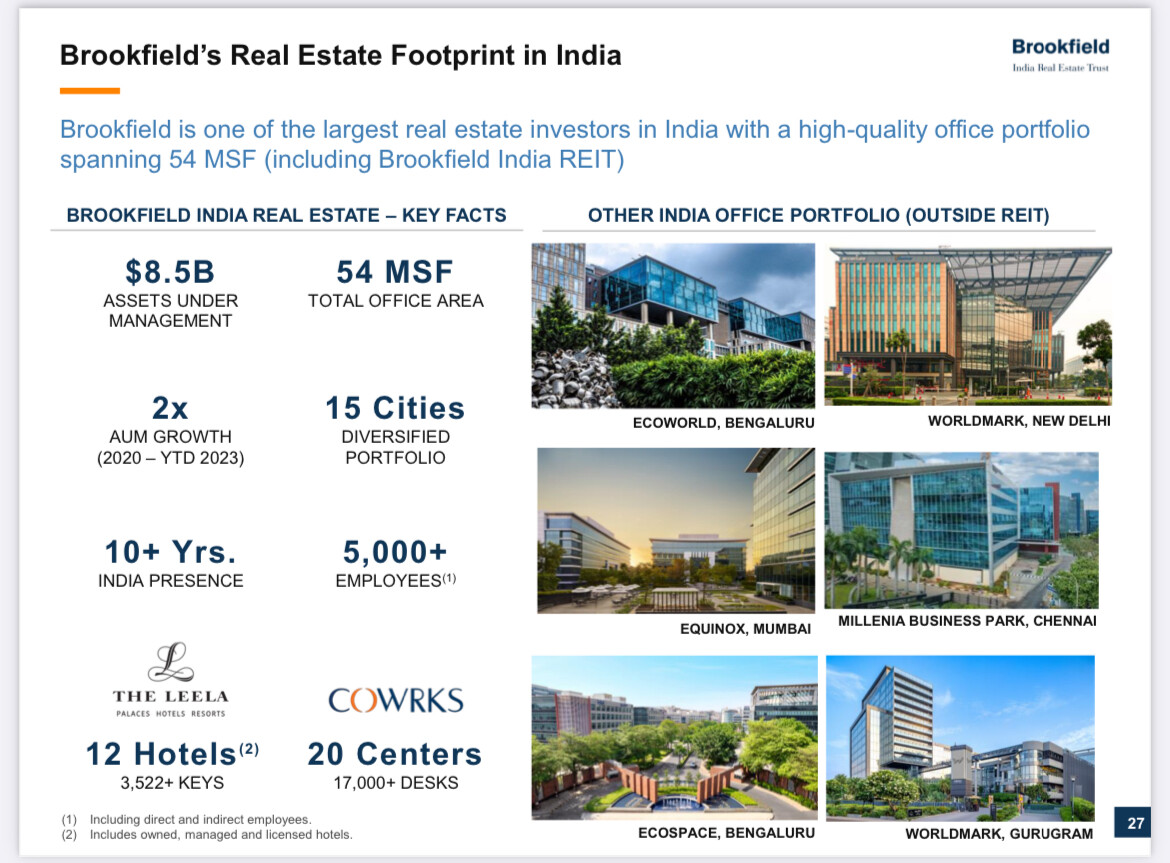

Brookfield India Real Estate Trust (BIRET) – Institutionally managed REIT (26-03-2024)

I am waiting for when the REIT acquires the assets in Bengaluru – Ecospace and Ecoworld. It would help in diversify more.

Jindal saw – Another beneficiary of India’s growth story (26-03-2024)

Promoters said margin will settle down but won’t go below 15. Looking at the next 3 quarters they are going to beat the QoQ performance hands down with increased revenue and better margins. So PE will keep going down further. Plenty of juice left here if my thinking is correct.

MOLD TEK PACKAGING—dividend plus growth (26-03-2024)

How can we know that perticular stock(e.g. mold tek pack, bajaj finance etc) will not go up in next two yrs? These examples are retrospective studies.

By the way, i try to follow 100 bagger book. As per book, one should not sell stock because it is not going anywhere. Rather one should add that stock during this consolidation phase.

One point from that book is as follow

“DONT GET BORED

=People often do dumb things with their portfolio just because they’re bored. They feel they have to do something

=Why do people buy and sell stocks so frequently? Why can’t they just buy a stock and hold it for at least a couple of years? (Most don’t.) Why

can’t people follow the more time-tested ways to wealth?

BECAUSE PEOPLE GET BORED

=People get bored holding the same stock for a long time—especially if it doesn’t do much.

…They see other shiny stocks zipping by them, and they can’t stand it. So they chase whatever is moving and get into trouble.

=Wanger used to say, investors tend to like to “buy more lobsters as the price goes up.” Weird, since you

probably don’t exhibit this behavior elsewhere. You usually look for a deal when it comes to gasoline or washing machines or cars. And you don’t sell your house or golf clubs or sneakers because someone offers less than what you paid

=Usually the market pays what you might call an entertainment tax, a premium, for stocks with an

exciting story.

=So boring stocks(stock going no where) sell at a discount. Buy enough of them”

BEW Engineering- A proxy play on pharma and chemical sector (26-03-2024)

Management commentary at Arihant Conference:

-

Doing 55 cr fundraise at 1540 now. Will be 150cr net worth after 55 cr find raise.

-

15 to 17cr capex will double production capacity. Out of this 11 cr for land

-

HLE is 3 times bigger than us. Years to come the gap will narrow down.

-

Penetration of process equipment is very very less. Only top 100 companies are using and the bottom 900 are not using. As government regulations come, usage will increase.

-

We are into niche where customers come to us with problems and we provide solutions.

-

We are saying no to few companies to improve margin.20% EBITDA margin target for new sales

-

World is going through capex cycle after 20 years and this will act as tailwind.

-

Spherical dryer not picked up to expectations.

-

Aramco subsidiary audited and approved us.

-

Capacity doubled from Jan 2024 onwards

I was not able to write down everything and may have missed a few points, if someone else attended please add on.

MOLD TEK PACKAGING—dividend plus growth (26-03-2024)

Rightly said, though as a small individual investor – I find it difficult. After investing 100s of hours going through concalls, presentations, reports, etc and continuous tracking, bias is hard to get rid of. Maybe for the likes of us, as far as we know that there is nothing significantly wrong with the company’s management or business per se, it is okay to stick to it? I am new at this even after 3+ years but hopeful of learning from the more efficient investors. The likes of Divis, Bajaj Finance and HDFC are going through difficult times, and untill I gather enough confidence or energy (part time investor with limited bandwidth so track less than 20 companies at a time) to invest in something better I find comfort sticking with them.

Goodluck India Ltd (26-03-2024)

In Arihant conference today, management gave a guidance of Billion Dollar Revenue target with 10% margin by 2030.

Kitex Garments Limited (26-03-2024)

As per the interview with Sabu M Jacob – it seems like they gave 25 Crores to Telangana party through Electoral Bonds. It is still kept as Privacy per Law – many companies do that including Bajaj Finance.

Company is having 3-5X Expansions in Telangana & That is what we Investors should focus for.

So no ground on CPM funding – as CPM is biggest troublers for them. (although they paid lower amounts as contributions to all parties including cpm)

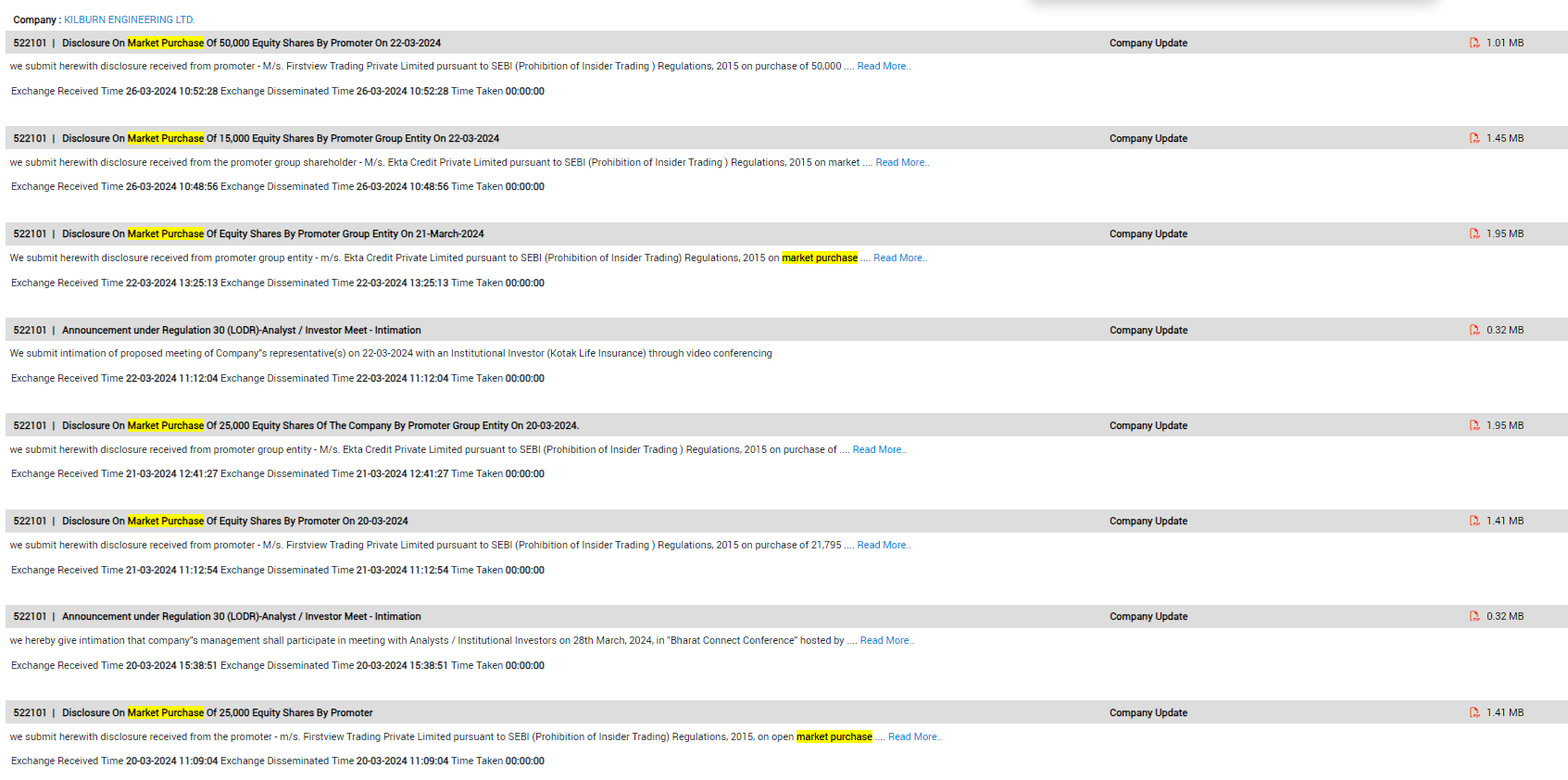

Kilburn Engineering – Huge undervaluation (26-03-2024)

Promoters have been continuously buying from open market in March. They bought more than 2L shares in March.