Any view w.r.t holding.

Posts tagged Value Pickr

Moldtek Technologies (26-03-2024)

Actually the owner being Mr J. Lakshmana Rao boosted my confidence in this company and was a major factor in buying this as my thought process is, if he built plastics to what it is today at an impressive growth, he can do the same for this, and till now YoY it has proven right. Their reviews online by employees is rather poor and is an issue to consider.

Kama Holdings Limited (26-03-2024)

SRF is approaching 52 week high and rebounding. Parent company Kama Holdings is not reflecting the value in its price action yet. Kama Holdings alternatively is closer to its 52 weeks low.

Any thoughts on this divergence?

52 week highs and all time highs strategy (26-03-2024)

Hitesh Bhai, Per my understanding, 200D.EMA had flattened & a double top pattern was evident on the daily chart after a long uptrend. Price broke below 200D.EMA in the last week. I felt that the current week’s closing price will confirm/disconfirm the double top pattern.

Do you think otherwise?

Disc: No position. Just curious to learn.

IBC referred Cases: Value investing or Value trap? (26-03-2024)

@Amit2saxena asked me a question, which i think might help everyone

the question was-

in ongoing IBC, if there is agreement between CoC and aquirer and 1) company owns valuable assets and 2) plan is to keep the company listed, then case becomes very interesting.

Example – 1) Amusement park of Imagica 2) Processing plants of Ruchi Soya

In the cases that I mentioned above, what part of the asset base i found interesting. For example, in case of Golden Tobecco or MT Educare?

my answer-

in golden tobacco its not about the assets, its about the list of prospective resolution applicants, i have never seen that many individuals being interested in any firm. In any of the IBC cases i read, i do not give any particular preference to assets, if its there then its a bonus.

I have a very simple strategy to follow change, any business going from 0 to 5 or 0 to 10 will give the same returns till a particular point (10 being the firm with strong assets and value and 5 with nothing special or significant), so i need to hold the firm till that particular point and then understand its value, in this way i broaden my target area (universe of firms), while also not getting paralysed while analysing the small units of data which prevents me from cashing out alpha till that particular point.

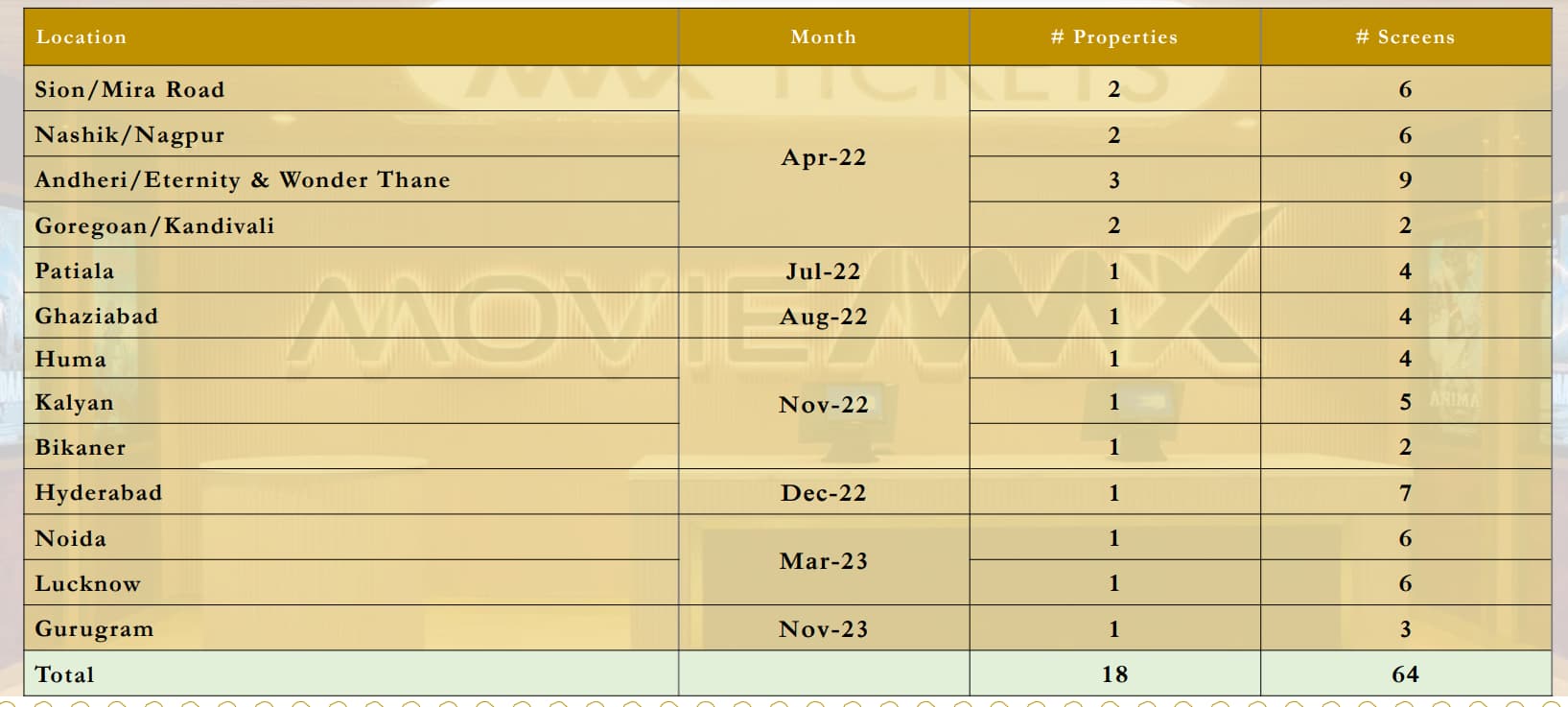

Cineline India – Picture abhi baaki hai (26-03-2024)

Has management given any commentary on slow screen growth this year?

They had added 60+ screens in FY23. They have added less than 10 screens in FY24. Each screen contributes to 8-10 Cr valuation.

Investor value creation only happens through screen addition in movie business. You can play with 10-20% with ATP + SPH increase. For multibagger returns, they need to add 30-40 screens every year.

I see only 2 possibilities – Sell hotel/ Dilute equity and bring growth money.

Companies with 20%+ growth guidance for next few years (26-03-2024)

Hi Anant,

I am not sure if there is a sureshot way to know if management is acting in their interest or that of shareholders. (If there was, I’m sure no Enron would ever happen.)

What an aam investor can do is some due diligence and hope (or pray) that things won’t go south.

What I do with my investee companies (small caps) is to read quarterly concall transcripts and check quality of answers management provides to analysts’ questions. I also follow corporate actions (e.g. fund raise, preferential allotment), third party transactions, legal disputes, relevance/quality of investor announcement (and their timings) etc. If something seems odd or fishy, I either get out of stock or avoid it completely (if I’m not invested yet).

Others may debate this approach but I feel at peace knowing that I’m not stepping on a visible landmine.

There is no guarantee that I wouldn’t end with odd companies with hidden landmines and that’s the risk I will have no choice but to accept. As they say in stock market it’s important to not only have rules for what you want to buy but also have rules for what you will never buy.

MOLD TEK PACKAGING—dividend plus growth (26-03-2024)

I also dont know too much technical analysis and for long term investors , chart patterns and other intricacies are not much helpful. But what chart is made up of is, Price and volume action and it shows what other buyers and market players are doing with your stock. If their buying and selling is affecting the price of your stock and through that your wealth, then you need to give attention to it. So what part of technical is useful to us as investors ( and not traders) is…to see if our stock is in uptrend (as per stage analysis…in stage 2) , or downtrend (Stage 4) or in sideways that means neither moving up , neither down…

Why this is important …because of opportunity cost of your capital…As you dont want your promoter of Mold-Tek Packaging to mis-allocate capital into such avenues where return on capital is less, similarly you also dont want your own capital to get mis-allocated into such companies at such stages where they are not earning anything.

Few Examples

- Mold-Tek Packaging is a great company with great fundamentals but its price on January 2022 was 830 and after more than 2 years in march 2024, its at 796…During these 2 years, its between and around this price. 2 Years is a long period of time, where you could have invested your capital into some equally good and fundamentally strong company and price may have taken your capital into 60-70% up, considering the roaring bull market during these 2 years.

- Same is the case with equally superior Bajaj Finance with price at 7800 in october 2021 till today at 6910 , more than 2 and half years , price at that level…big opportunity loss for our small capital

- same is the case with SRF, PI industries , Divis labs, Tata Elxsi…all of these are A-grade blue chip companies but price has not moved over last 2 years and its a great mis-allocation of capital on our part in remaining invested in them during their down trend. We are not married to them or neither we have any personal interest in these promoters. Our sole goal is to enhance our capital at a decent rate of return , probably better than index. These are just instruments for us to increase our capital. They are not End point, they are just intermediaries to fulfill our financial goals, not goal in themselves…What say?

Snowman Logistics (26-03-2024)

Exited the stock. stocks with good earnings and fair valuations will survive through the upcoming events.

Jindal saw – Another beneficiary of India’s growth story (26-03-2024)

I don’t think you are differing with me. EV/EBITDA multiple (just like P/E) currently looks low due to outstanding EBITDA performance company has delivered in the recent quarters.

If I’m not mistaken in the last quarter concall, management has guided for slightly lower EBITDA from current 18.2% as they said it’s not sustainable. .

So if EBITDA margins have peaked and start yielding you will have to look at valuation picture again as to how they are placed against historical median. From a quick back of envelope calculation, a 2% moderation in EBITDA margins will inflate EV/EBITDA multiple by 10%.

Point I was trying to make was that commodity stocks go through cycles of mean reversion (from top or bottom) and timing can be a critical factor. These are not your typical consistent compounders where you can hope to make decent returns from any point you enter.