Detailed Analysis on the company is as below : https://x.com/SULABH40/status/1742453632598257925?s=20

Disclaimer: tracking position, for educataional purpose.

Detailed Analysis on the company is as below : https://x.com/SULABH40/status/1742453632598257925?s=20

Disclaimer: tracking position, for educataional purpose.

There are just 19 share holders outside of promoters and no one will sell a single stock.

It’s a dead stock as far as stock exchanges are concerned like Taparia Tools (300 share holders) and ELCID Investments (301 shareholders).

Probability of Sir Ratan Tata Trust selling you a share of TATA SONS is higher than you managing to buy a share of APIS/ TAPARIA/ELCID

Such companies should be delisted.

When screening stocks, and some stock ratios look too good to be true…

always check how liquid shares are for trading.

After a brutal week in the broader markets, my portfolio has taken a substantial hit. I’m down about 13% (annualizaed at about 80%).

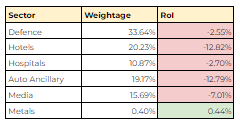

During this correction, I’ve replanned my portfolio allocation theme. Instead of focussing on the number of stocks, I have identified a sectoral mix for my portfolio. Here is how the desired mix would look like:

FinTech is another sector that I would look to invest in, and would like it to occupy 10%-15% of my portfolio, contributed by 1%-2% of dilution from all the other sectors. However, I am yet to research on valuable growth stocks in this space. The idea is to have about 60% of my portfolio in non-cyclical sectors (Defence, Healthcare, FinTech, Music) from which I can expect a fairly stable growth, while cyclical sectors like Hotels, Auto Ancillary and Metals can give me some higher beta over the next couple of years.

So, coming back to my portfolio, I decided to take a tracking position in JTL Industries. While it’s facing some FUD regarding one of its shareholder’s shares being frozen by ED, I’m quite optimistic on its guidance for the next 2-3 financial years. This, along with probably Hariom Pipes, will be accumulated over the next 3 months. Also, I took a bit of a position in Minda Corp. The fact that the Indian government is looking to attract investments from EV manufacturers comes to me as a tailwind for auto-ancillary companies looking to cater to the EV OEMs. I already hold a substancial position in Pricol, and I will add more positions in Minda as it has looked strong in the recent past.

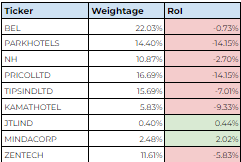

The following is a snapshot of my portfolio, both stock and sector wise.

@ca.rishab

The issues raised by you are valid. One of the problems of small cap investing is that info is always scarce & is perhaps one of the reasons for low market caps for small caps. Another factor that I personally follow for small caps is not to go back more than five years, usually not beyond 2 to 3 years. That’s my style, not necessarily the correct one! Of course the more historical info one has, the better equipped one is in taking a call. Ultimately, it is always a trade off & the investing decision at the end of the day is largely a gut call. If after weighing the pros/ cons, I’m not comfortable with the story for any reason, I too will refrain from investing.

It is perhaps for this very reason that the education business is being hived off. It will probably have no legacy issues in the balance sheet & so would be lean. I feel that the education business itself could value about the same, if not more, than the current market cap, given it high operating margins over the last 6-7 qtrs of over 50% (Stand alone numbers as the NBFC is in a 100% owned subsidiary). A lean balance sheet would also means attractive return ratios. All this if backed by a decent dividend payout ratio, would mean sending positive signals to investors. That said, we have to wait & watch closely, how the story unfolds over the next 3-4 qtrs as nothing is a given.

Awesome & congrats for your remarkable achievement. I have heard about similar strategy being adopted by one of better known skilled investor Basant Maheshwari when an individual is starting with very low amount of capital.

What is your strategy in current market ? Is the degree of risk, you are following now, same as earlier ? Or it is being reduced by considerable amount since your portfolio have reached certain size ?

One of their top 3 products has market size of 250-300 MT (as per CRISIL). Supriya’s capacity is 60-70 MT.

My allocation in this pf is in low single digit as part of my overall equity portfolio.

I have not done any backtesting.

Absolutely, agree. When they crash, it is all gone. But the gains are expected to be more than the losses. This has been my experience till now.

@vkediaonline The reason I look at the index only is to minimise the risk. Smallcaps are known to be risky; one way of reducing risk is to remain in the Index. Someone else (NSE here) is doing the vetting process and we are sure we are fine with these companies.

With the index rejigging that NSE does regularly, the weaker ones are removed and hence over any period of time, the stocks in the index are the good quality ones.

I understand that some good smallcaps outside the index might be performing better, but this is a price I have to pay to ensure quality and a good night’s sleep.

Good blog explaining how growth seems to be returning in OFSS.

Sir, I wanted to share some feedback with you regarding the responses I’ve observed on several threads. I’ve noticed that sometimes the context of conversations with management isn’t fully provided. It would be immensely helpful if you could include more details about the questions asked and the responses received. This way, readers can better understand the situation. Your efforts to ensure clarity and transparency are appreciated.

Thank you