CANCELLATION OF PREFERENTIAL ISSUE

Posts tagged Value Pickr

Genesys International – Product Monetisation (14-03-2024)

“The company secured a mega-contract worth Rs. 155 Crores with BMC to develop

Mumbai’s 3D city model and map stack”

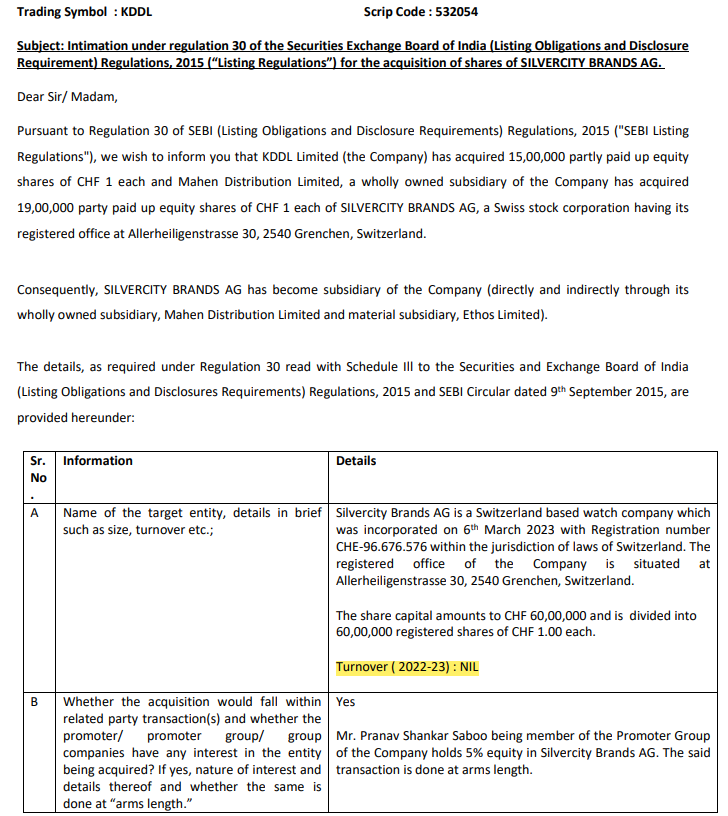

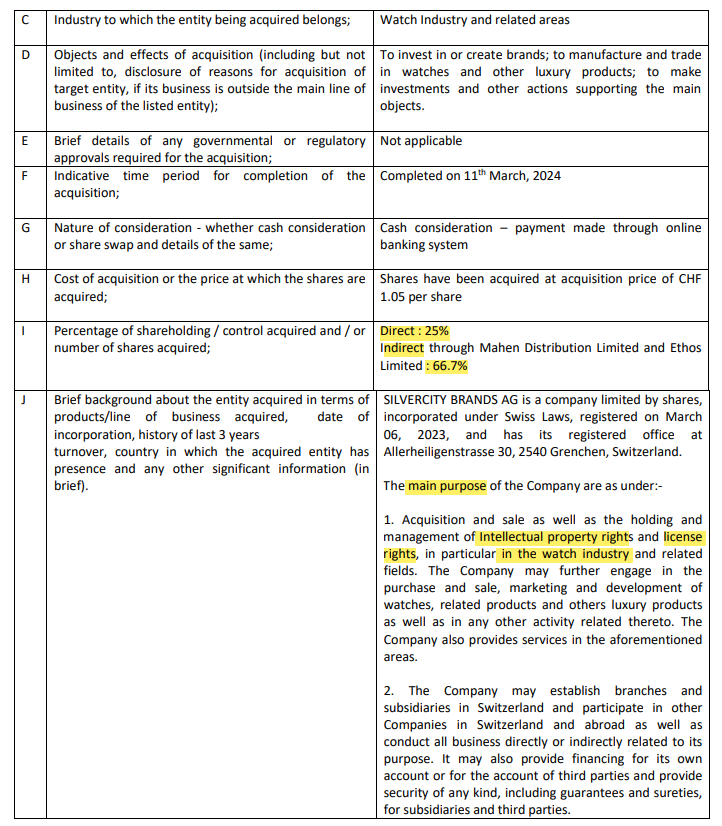

KDDL (Ethos Watches) – Scalable business model at an inflection point? (14-03-2024)

Thanks for clarification. will delete as well as my earlier post shortly

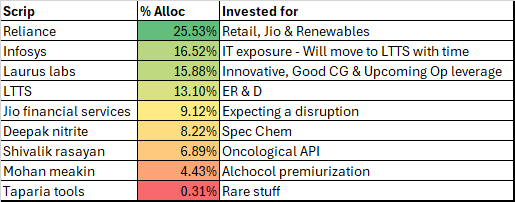

Voldemort’s Portfolio (14-03-2024)

Multiple exits – Mar 23

Natural capsules is off – My buying price is ≈ 310, Sold it off as i did not want to ride it in loss. Predominantly as my confidence in the stuff their management is telling is waning off. Eg: They have been postponing the API facility 2 years now, the approval for 8 months now ?

I expected them to get approved when govt came up with multiple approvals on mar first week. Hence, Suspect there might be greater issues. Was one of my highest smallcap exposures, Sold off with 1% returns ![]()

Cash will be withdrawn.

Ramkrishna Forgings (14-03-2024)

It’s quite unusual that it hasn’t quite bounced back from yesterday’s level when the when the mid cap index is 2.25% up , any news associated with the stock which I might be missing?

KDDL (Ethos Watches) – Scalable business model at an inflection point? (14-03-2024)

(post deleted by author)

KDDL (Ethos Watches) – Scalable business model at an inflection point? (14-03-2024)

What is it with Ethos suddenly reducing their stake in Silver City? That recent notification was really perplexing, and the market doesn’t seem to like it either? Anyone got any clue kn this?

Shivalik Bimetal Controls Ltd (SBCL) (14-03-2024)

Q3FY24 update from Dalal & Broacha.

Shivalik Bimetals_Q3FY24_Dalal&Broacha.pdf (481.7 KB)

Disc: Invested

Sandhar Technologies – An emerging market leader (14-03-2024)

Few thesis pointers which look interesting:

- Sitting on operating leverage with a good order book and visibility.

- Management has guided for a strong Q4.

- Margins are on the improving trajectory and shall gradually move towards 12-13% in the next few quarters.

- Company is slowly deleveraging as well.

- Solar power integration for cost savings.

- Plant consolidation for cost savings and efficiency.

- Topline growth of 16-20% with gradual margin improvement may lead to a PAT of around 250-300Cr

- Exit multiple in the range of 25-30x is a reasonable expectation

- If the numbers play out then the odds do seem to be good at the moment

Disc: Invested and biased