ED freezes account of Zenith multi trading that could the reason.

Posts tagged Value Pickr

Smallcap momentum portfolio (11-03-2024)

@mrlearner Last couple of weeks it has given -ve returns. Today also it is in red. But over 16 months the XIRR is still close to 95%.

SmallCap Hunter : Trying to find the dark horses with triggers (11-03-2024)

There is nothing like that. Pockets of overvaluation will revert to mean, there is still value if you have a stock specific approach. Additionally, every March there is tons of profit booking due to income tax and advance tax payments. We will get attractive valuations to add to existing positions and entry points for watchlisted stocks

Marksans Pharma- Can it be the next Pharma Biggie? (11-03-2024)

I think they have good regulatory compliance record and mainly have OTC products. Their Formulations are sold in highly regulated market and that speaks for the quality. I think they are growing well. I think they are likely to double the revenue in less than 4 years. With margins increasing because of economies of scale as well as operating leverage I think their profits are likely to grow faster than revenue. Management looks capable and are very careful of what they say about the future.

Disclosed. Invested

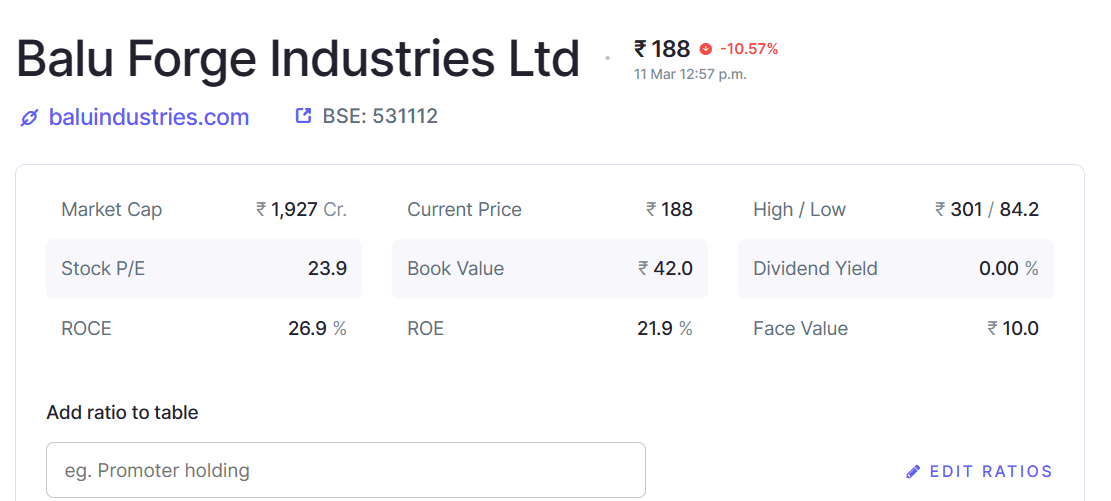

Why is Balu forge declining? (11-03-2024)

I don’t get it, why balu forge is declining.?

I have seen this thing that forging industry generally has a good amount of fixed asset but why there Fixed asset is so low.

After 2020 Jaspal Singh came right? that’s why it is showing FA after that .

JTL Industries – Fast Grower at an inflexion point (11-03-2024)

(post deleted by author)

Narayana Hrudayalaya Ltd (11-03-2024)

Why look at historical per bed metric to determine valuation? It’s like trying to determine hero motor’s valuation by looking at historical average price of their bikes.

Average revenue per bed has been trending up for all hospitals which could be due to just inflation, operating leverage or product mix change or all of them. EBITDA for leading hospitals including NH has also been steadily increasing with only exception of Apollo. So there is no reason to believe why earning per bed of hospitals will remain at historical levels.

Coming to NH, it trades at some 30 p/e against a sector average of 70 with leading hospitals such as Apolo, Medanta, Max all trading at 70 p/e. Interestingly NH stock prices have trailed earning growth which means stock is heavily derated (guess something to do with Cayman overhang).

Gulf Oil Lubricants – A low risk way to play the economic cycle? (11-03-2024)

Hi,

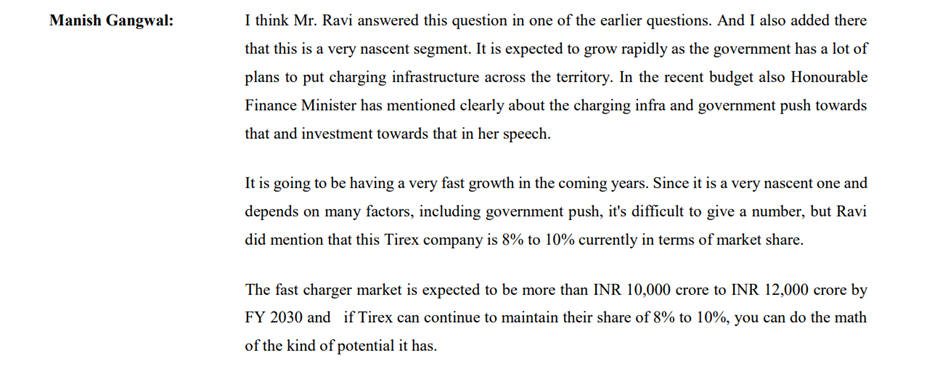

What the management has said is that the fast charger market is expected to be more than INR 10,000 crore to INR 12,000 crore by FY 2030. So if Tirex can continue to maintain their share of 8 % to 10 %, Tirex revenue at the lower end would be Rs.1000 crore in FY2030.

And at 51 % stake, that is Rs.500 crores. Note that Tirex will be making 240 kW chargers, these cost upwards of Rs.20 lac to 30 lac per piece based on a google search for similar products.

Truck Exicom 240 kW EV DC Charger, For Buses,Trucks And Cars at Rs 2130000 in Thane (indiamart.com)

So assuming an average of Rs.25 lac per piece, you will need to sell about 4,000 chargers to make Rs.1,000 crore revenue for the company. Now whether this pricing will hold is anybody’s guess. In any case, more recently the company seems to have broad-based their plans since the MoU signed with the Government of Gujarat mentions producing 10,000 chargers annually. We will have to wait for the next concall to get additional details on this I think.