Dear @Rajat4636, it appears from your previous posts on IIFL and now Saregama that you are not adding any values and only looking to troll. I suggest please avoid it as there are other social media platforms where you can voice out your views. May i request the moderators to take action as such posts/users only spoil the learning experience on Valuepickr.

Posts tagged Value Pickr

Long term bonds (10-03-2024)

But Shail, I have a question. In the declining interest rate scenario even equity will also be rising, and if yes will it also not give good return? ( Apparently there are no easy answers in equity)

Regards

Gensol Engineering – A play on Energy Transition (Solar Energy & EV) (09-03-2024)

All the credits Value Pickr team for which we come to know dubious company like this and could save our money, I was about to invest in this company before searching out in VP.

![]()

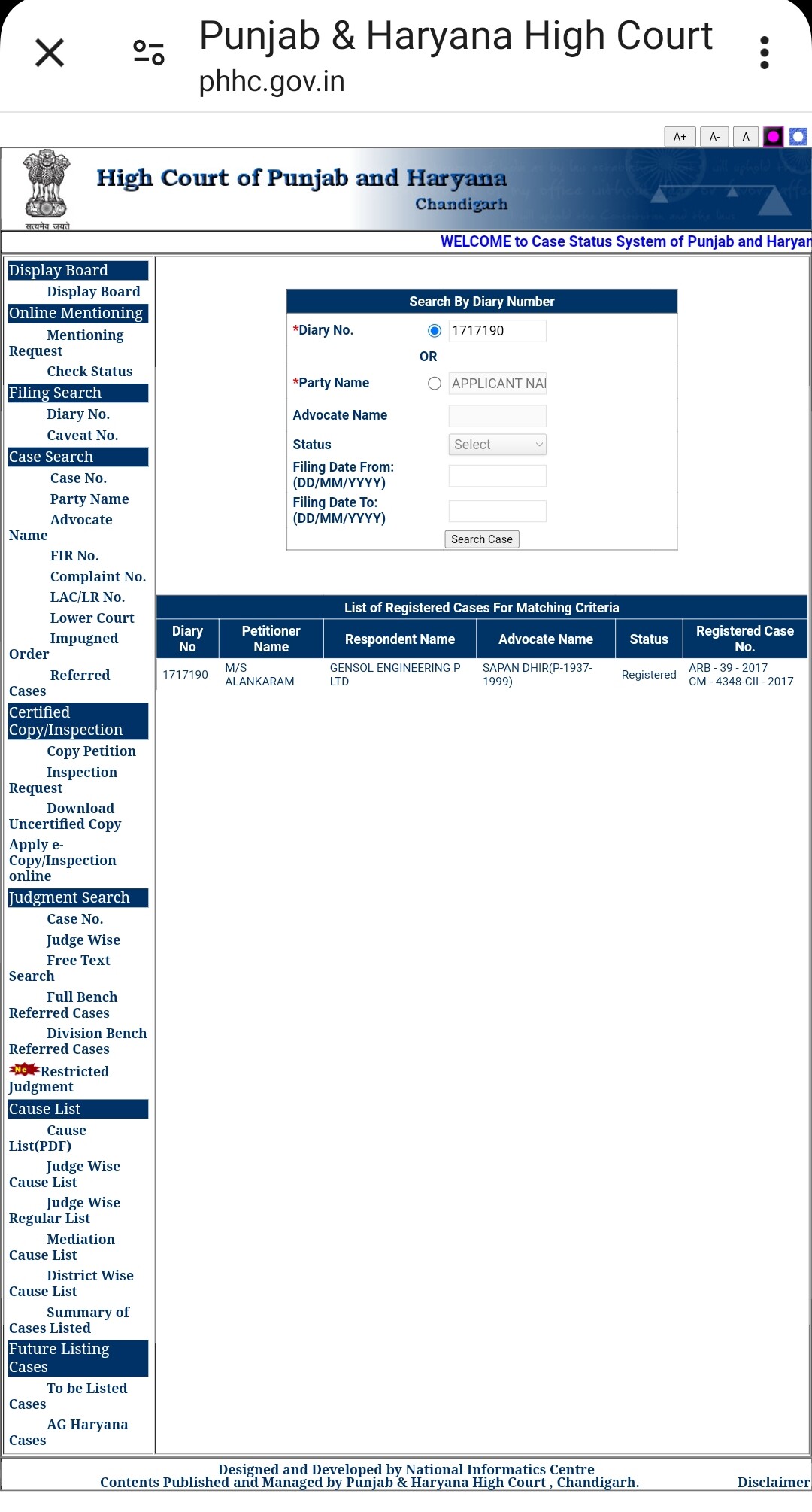

Gensol Engineering – A play on Energy Transition (Solar Energy & EV) (09-03-2024)

Following is the case screenshot

CESC LTD Demerger (09-03-2024)

Can you elaborate a bit more?

Techno electric engg ltd (09-03-2024)

I did a thesis post on Techno’s data center business on X yesterday. Here is the content:

Techno Electric is among India’s best power EPC companies by capabilities, having market leadership in 765Kv transmission, and a very good standing in smart meters, FGDs and other power EPC. But it’s their data center business plans that I am most excited about!

High level story:

A super conservative man like Mr Gupta who has been boarding cash on the balance sheet for years is talking about taking on 5000cr of debt by 2030 to make an investment of 15,000cr to develop 250MW Tier 3+ and Tier 4 data center development suitable for hyperscalers. I sense he smells a seriously disproportionate opportunity.

The present estimate:

The construction of a 24MW data center in Chennai is underway and phase 1 is near completion. In the last call, they mentioned bringing in a person from Silicon Valley for the data center business, who will probably help them broker a deal. Similar deals have been happening at 100-150cr/MW globally. So conservatively if this sells at 100cr/MW, we have a 2400cr sale right there.

Now Techno spends somewhere between 40-50cr/MW in development. If they are able to sell close to 100cr/MW, thats a very high RoE capital gain. Going forward, they will likely fund a part of future investments with debt, increasing the RoEs even more!

The analogy and model:

There should be significant demand for Tier 3+ and Tier 4 data centers. Mr Gupta has not been very clear on whether they plan to build and sell / build and lease themselves, or if they want to use this first project to prove capabilities and then take on high end data center EPC work. If it’s the former (I hope it is), I’d think of this business analogous to a high end real estate (high RoEs) where only a few players can compete and demand is not a problem. If it’s the latter, then it’s analogous to a specialist high margin construction company in a booming construction cycle. It could be a monstor of a business if they are serious about the 250MW plan over the next 5 years. It could dwarf the existing EPC business in scale and valuation.

Their right to win:

Robust and reliable power infra is one of the main competencies needed for hyperscaler data centers as downtimes are not an option for Tier 3+ and Tier 4. Techno has this covered better than anyone else I would imagine. The other competemcies like internal connections, cooling systems, rack reconfiguration etc are probably easier to master with the right investments is my understanding – happy to learn more about this from domain experts.

Valuation and risk-reward:

This when the entire company is at 6500cr EV with a rapidly growing and profitable EPC business which they are guiding will do sales of 2500cr (~40% growth) in FY25 and 3200cr in FY26. So the EPC business alone is valued at 2 times EV to FY26 sales, for an industry leader in a sector experiencing massive tailwinds. The story will obviously come down to execution, and this is the main risk.

Please do your own research. I am invested and biased, and as you can see, I’ve done a lot of protecting and guess work. I could be completely wrong in my assumptions.

Disclosure: Invested in the last couple of weeks with a mid sized allocation for now (5%).

Maharashtra Scooters : Value of Listed Investments Make it a great value pick? (09-03-2024)

Apart from Tata Investment which is trading at a premium, all the holding companies generally trade at a discount(20-80%).

Have a look at this:

Is TATA Investments a Big Bubble? 🫧

To compare it with Tata Investment that is an anomaly (w.r.t. holding company vs underlying assets valuations) does not look justified in my opinion.

Newgen Software (09-03-2024)

Newgen software has been affected by a ransomware incident. They have notified CERT-IN as per regulations. Further information on this to arrive

Why companies show negatives taxes? (09-03-2024)

but why it is show much in adani stocks only ?