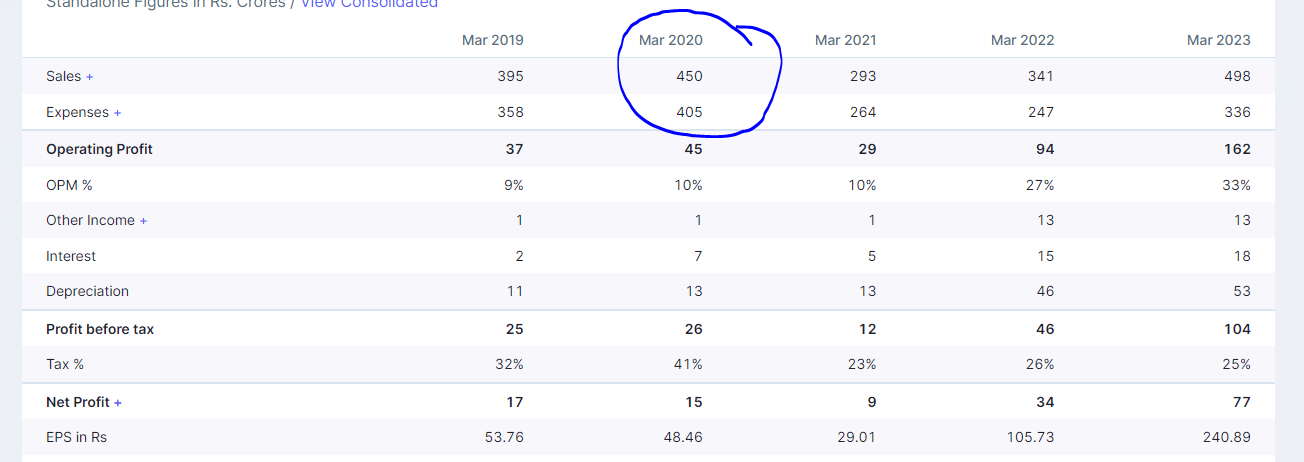

Hi Varun,

Please see, sales has not doubled in two years. Even in 2020 sales were 450cr

Also company is confident of margin to be at 28 to 30 percent range . the reason being

Hi Varun,

Please see, sales has not doubled in two years. Even in 2020 sales were 450cr

Also company is confident of margin to be at 28 to 30 percent range . the reason being

Couple of more questions here :-

1.) Has the Tata Chemicals mgmt indicated selling shares in IPO and sharing/distributing the proceeds ? If no, then the value doesn’t unlock truly and it remains as Ben G said – “Frozen Corporation”

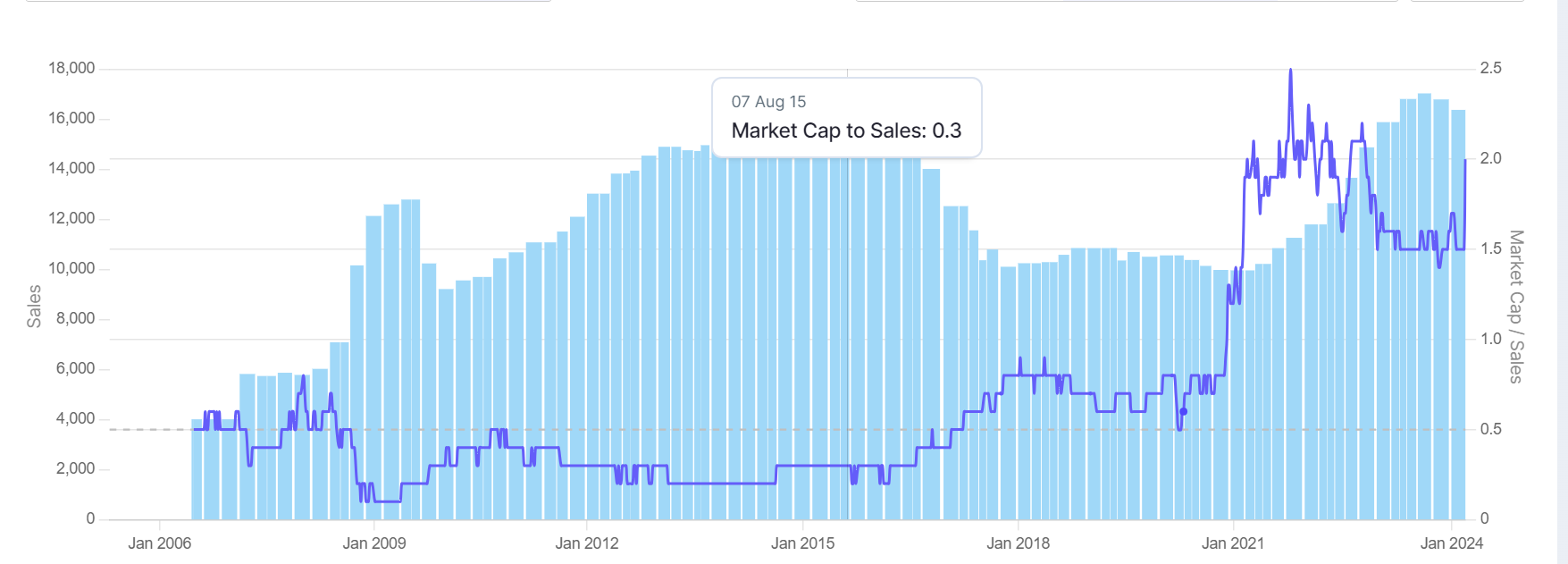

2.) Have u checked the P/S of standalone biz on historic basis – I blv the company has always traded at this avg P/S barring the COVID demand-supply mismatch period. If anything has changed in fundamentals of base biz to command higher valuation, plz share

Attaching the chart for your reference :-:

Disc :- Not invested

I haven’t analysed in detail. But here are my thoughts:

Credo Brands reported doubling of sales in 2023 as compared to 2021. What caused this sudden spike in sales and OPM to zoom to 30+ from 18-20 percent?

If I am being totally conservative and assign pre 2021 OPM of 20 percent on sales of 500 crore, PBT will be around 50-60 crores and PAT to be 40-45 crores based on 25 percent tax. Total number of outstanding shares are 6.5 crores. That gives us an EPS of 6-7 and P/E of about 30 on CMP. Things to ponder:

Disc – No holding.

Thanks,

Varun

(topic deleted by author)

Does anyone have any clue as to why NH is still continuing to fall with no bottom in sight? For all the other hospital sector players like Apollo, Fortis, Max, etc., I can see the intensity of the fall somewhat tapering down and indications of a bottom forming, while NH continues to fall steeply every single day.

Given that their P/E multiple is lower than other competitors and that their strategy is primarily centered around patient volumes and not pricing, I would think that any regulatory setback should affect them to a lesser degree. Am I getting something wrong here? Is NH overvalued with respect to competition?

I track sugar wholesale prices here: Sugar Talk – India’s Largest Sugar Trade Community

After having two consecutive 40% of draw down, it was expected IIFL to bounce back. This is the market for you. The day RBI lifts ban, hopefully sooner, it may reach to the level of 600+. Now they have a support of $200 M support for the liquidity and gold hitting the all time high!

whats the upside for the stock?

326 shares or 326K shares? On the same topic, saw this in ET and thought of sharing.

Tata investment has 6% stake in Tata Chemicals.

VV says :

That he is aware of the cost to income ratio although it did not merit any concern as everything is going as per plan. To assuage the concern he says Growth in number of branches will be as per deposit requirement and branch target may be scaled down.

The next 5 year targets of liability and assets are conservative targets and easily achievable keeping past performance in mind. Some of these targets like asset quality, recoveries, GNPA etc are already achieved and bank has to only strive to improve further.

No worry on sustainability of High NIM of 6.3% as it is primarily due to business structure, and faithful implementation.

Completion of reverse merger, expected by June – July.

In my opinion, banking sector is a reflection of the state of economy and governance. As the economic performance is continuing to give positive surprises, good banks should perform well in the next five years. As usual, Private banks will perform better and out of these, smaller well run banks like IDFCF should do even better.

The monitoring by the regulator RBI is better than I have ever seen in last 30 years, which is a big comfort.