Great question !

It’d be nice info if someone can offer cost of green h2 to furnace…i think cost would be higher compared to coke.

But 30% import tax at European destination as CBAM using coke would be compensating higher cost of H2.

Posts tagged Value Pickr

Green Hydrogen as a Fuel – Indian Companies leading the Green Revolution (05-03-2024)

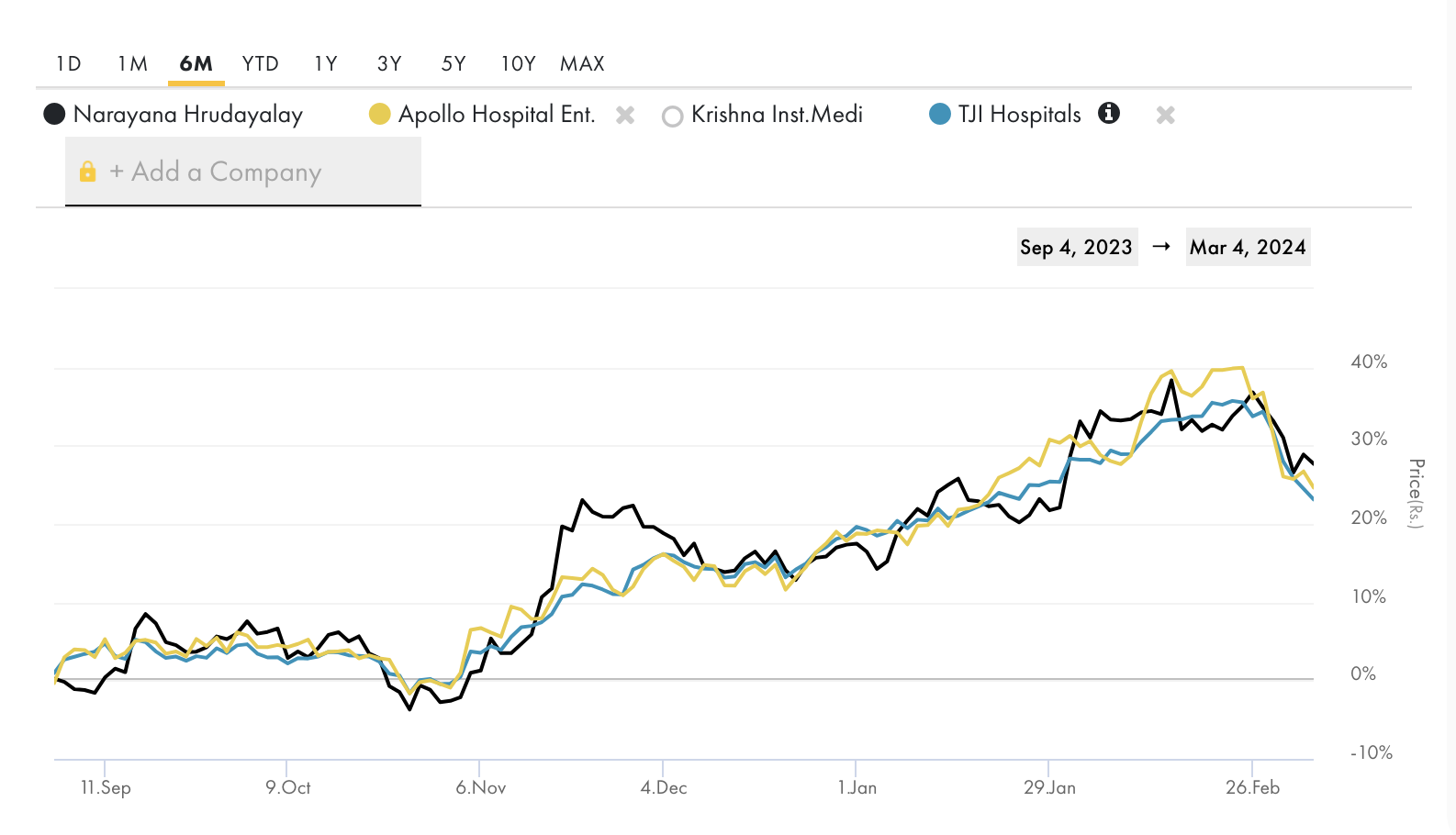

Narayana Hrudayalaya Ltd (05-03-2024)

@Yusufi_Kapadia I think the overall Hospitals index is pricing in a potential negative outcome. NH price action is inline with that of the index.

IIFL Finance (erstwhile IIFL Holdings) ~ Retail focused diversified NBFC (05-03-2024)

Can anyone who tracks Banking and finance sector tell me has similar things happened in past also with other companies. RBI is looking v strict this time, first Paytm and now IIFL. I am assuming similar cases might have happened in past also where RBI would have taken big actions and later after some time (may be few months or years) they gave some relief to the company or sector. I want to understand if this is a short-term issue which can be fixed, and company can return to normalcy (in few quarters or 1-2 years) or this is going to affect long term fundamentals of the business (just like what happened in Yes bank , not recovered after 7-8 years also).

Thanks in advance.

IIFL Finance (erstwhile IIFL Holdings) ~ Retail focused diversified NBFC (05-03-2024)

edelweiss then, iifl finance now ![]() Some things never change

Some things never change ![]()

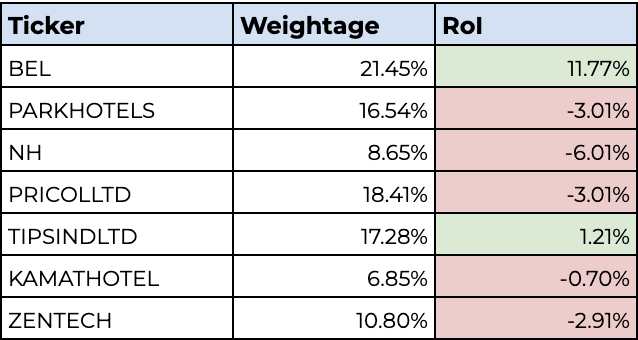

Ayan’s Portfolio (05-03-2024)

Here’s my updated holding as of today, trimmed a bit of NH due to the regulatory clouds. KAMATHOTEL looks promising as per this con-call highlights here. ZENTEC is a 3 year long bet given their management’s guidance of 50% CAGR between FY26-FY28.

Green Hydrogen as a Fuel – Indian Companies leading the Green Revolution (05-03-2024)

Good Point. Does it reduce costs also or costs between Imported Coking Coal and Green Hydrogen are similar.

IIFL Finance (erstwhile IIFL Holdings) ~ Retail focused diversified NBFC (05-03-2024)

IIFL Meeting after RBI Action 5th March 2024_.docx (23.1 KB)

Transcript of the meeting

Page industries (05-03-2024)

Since I’ve started investing in stocks (2013), PAGE had been on my watchlist. However, being a novice investor then, its valuations scared the daylights out of me. As time passed, I learnt some companies command better valuations in the market (esp. consumer facing companies) and PAGE is one of them. However, I continued to stay away from the company as the growth was faltering heading into the pandemic.

However, during COVID and maybe in 2021, the growth for the company rebounded and the valuations of the company were similar to/slightly lesser than where we are today and also similar/slightly lower than its all time avg PE (this is around Q1/Q2 FY22). At this time, the mgmt was supremely bullish about the prospects of the company and had guided for a topline of $1 billion (~INR 8,000) crores by 2026. This worked out to 15%+ growth for a beloved consumer facing company, with steady/improving margins, amazing cash flows and a great dividend yield.

I figured my years of waiting on the sidelines to pick up PAGE were finally over and I decided to dive in owing to this amazing window that had opened up – a consumer facing stalwart set to grow again and valuations being favourable (relative to what it had been for PAGE). I invested ~3% of my pf in PAGE between 2021-2022.

Circa 2024, I’m sitting on ‘no gains’ at my averaged acquisition cost between 2021-2022. So, what has gone wrong? Well it was the managements bet on their ‘Athleisure’ category. That to me has simply bombed. Just like many media based tech companies, ed tech companies made projections of growing their toplines faster than the speed of sound during/post COVID, PAGE did something similar, it projected amazing growth rates in its ‘Athleisure’ category leading into 2026. And for a while it did work, when everyone was home and later when COVID subsided, people were still home owing to the hybrid work culture and the sales kept on humming. However, the music finally stopped in 2023 when people were back in offices, all the revenge buying was done and peoples behavior more or less remained the same and everyone that made insane projections were left holding a lemon, to me PAGE seems no different.

Personally, I don’t see this changing dramatically in the near future either, I mean just go through managements latest concall and the general industry trends,

-

Athleisure is the most impacted category

-

Most of the inventory is still clearing slowly

-

Existing inventory in the market was created when raw material prices were higher, there goes any scope of margin expansion due to the cooled off raw material prices

-

Most of the industry is trying to get rid of its inventory via heavy discounting, to PAGE’s credit it isn’t doing the same, however the supply glut will take many quarters to clear

-

Won’t be able to price the products any higher in the current environment. Don’t see the need to increase it for the next 1 year. Having tracked the company for long, they’ve always taken 3-5% hikes every 12-18 months, not sure if they did that last year, they aren’t certainly doing it this year.

-

Consumer buying trends remain weak and won’t correct till the next festive season. Who is to say it’ll correct then?

Other Qs swirling in my mind,

-

Why would someone buy an overpriced ‘Jockey’ T-shirt (part of the Athleisure catalog) when one can buy a T-shirt from literaly any brand. I mean who wants an underwear brands branding on their t-shirt?? Will the growth really come from here?

-

Generally, in the Athleisure category there is an insane amount of competition. You can buy similar stuff from any of the large format stores, other brands and not to mention all the stuff available online. How powerful is the ‘Jockey’ brand will be seen in times to come. I have my doubts if the company really has an edge here. Their sales will improve when the market conditions improve, there is nothing else to it.

-

Overall trends in the consumer facing industry remains weak. I own and have owned a lot of consumer facing stocks, most of them have said the same thing. Be it Nestle, P&G, HUL, La Opala, RBA (and other QSR players), Hawkins etc. I keep wondering if all the amazing economic data coming through from the government spending is papering over the stress the households are facing in buying everyday or more frequently used products. Is the economy really purring? I’m personally very confused.

I had purchased PAGE as part of my coffee can pf with an intention to own it for the 5 years that they had provided the projections for, from 2021 – 2026 (and maybe beyond depending on performance). Just like the management’s projection, I feel, I’m also left holding a lemon now. I have waited here 2 years without any growth. Will give it a few more quarters to see if things turnaround, otherwise, I feel the base created by the ‘one-time’ Athleisure sales during COVID will take a long time to be replaced by the growth in other categories and the stock will meander and go nowhere for some more years. At such point in time, I think, it’ll be best to deploy this money elsewhere.

For the time being, I’m in wait and watch mode with very low expectations that the company will be able to meet its expected goal of $1 billion in sales even by 2028/29. I simply feel the category they’ve bet on won’t fire as expected and I would love for the management to prove me wrong and make me richer ![]()

IIFL Finance (erstwhile IIFL Holdings) ~ Retail focused diversified NBFC (05-03-2024)

Should you have seen it coming? Here’s a short and sweet analysis of what’s up at IIFL Finance and whether this is a falling knife you want to catch (Hint : Absolutely not).

I also think the Concall has very less Quality information to offer. It is largely a Disaster management attempt in my humble opinion.

P.S – It’s unfair to blame Anyone else when your decisions go South. Take Responsibility. Own up and move on.

Rahul

IIFL Finance (erstwhile IIFL Holdings) ~ Retail focused diversified NBFC (05-03-2024)

The call is uploaded on the website but here is some autogenerated summary.

IIFL Call after RBI Action – 5th March 2024

RBI’s Concerns about IIFL Finance’s Gold Loan Portfolio:

-

Deviations in assesing and certifying gold purity.

-

Breaches in loan-to-value (LTV) ratios.

-

Excess cash beyond statutory limits.

Corrective Actions Taken by IIFL Finance:

-

Minimizing deviations in gold assessment between branches and the audit team.

-

Implementing stronger systems to ensure compliance with LTV norms.

-

Aligning cash disbursement practices with the Income Tax Act interpretation.

-

Ensuring comparability of auctions as per RBI’s circular.

-

Clarifying the purpose of the ₹200 option notice or option intermission charge.

Operational and Procedural Issues:

-

Addressing operational and procedural issues with sincerity and effort.

-

Emphasizing the absence of governance or ethical issues.

-

Reiterating the company’s solid foundation built on trust and support.

Commitment to Compliance and Transparency:

-

Taking immediate and comprehensive steps to address RBI’s concerns.

-

Implementing necessary remedial measures to comply with and exceed regulatory standards.

-

Navigating the situation with transparency, integrity, and respect for compliance standards and regulations.

Stakeholder Support and Appreciation:

-

Expressing gratitude and admiration for RBI’s commitment to financial system stability and integrity.

-

Acknowledging the value of RBI’s guidance and oversight in fostering trust, transparency, and resilience.

-

Emphasizing the importance of continued support from stakeholders, customers, employees, and partners.

Gold Securitization and Assignments:

-

Gold remains with the company during securitization and assignments.

-

Assessment is done by the company.

-

Assignment partners or co-lending partners have access to data and can audit the gold packets.

-

Securitization is mostly done through the PTC route, while assignments account for 90% of transactions.

-

The company has 15 co-lending partners.

Deviations in Gold Weight and Valuation:

-

Deviations in the net weight of gold between disbursement and auction identified by the audit team.

-

Deviations found in 55,000 cases, but most of the money has been recovered.

-

Engaging with RBI to address valuation concerns and requesting a meeting.

-

RBI has been highlighting valuation observations in previous engagements, and corrective actions are being taken.

Cash Disbursement and Opex:

-

Cash disbursements have been stopped, but earlier disbursements up to two lakh rupees were happening through cash mode.

-

Banks are allowed to do cash disbursement up to two lakh rupees, but they can’t do more than one piece.

-

Monthly opex of the branches for gold is around 65 to 70 crores, and the monthly collection growth on the golden portfolio is more than 135 crores.

RBI’s Inspection Report and Corrective Actions:

-

Received an inspection report from RBI in January and taking corrective actions.

-

No other ongoing inspections or inquiries by RBI for any other products.

-

Planning to revamp processes to address issues identified in the RBI’s inspection report.

-

No penalties or actions taken by RBI against the company prior to this inspection.

Financial Impact and Gold Loan Portfolio:

-

Financial impact of RBI’s action is uncertain and depends on the time taken to resolve the issues.

-

Gold loan business incrementally adds about 5% to the portfolio in a quarter and runs down about 10-12% every month, making it difficult to determine the overall impact on asset quality.