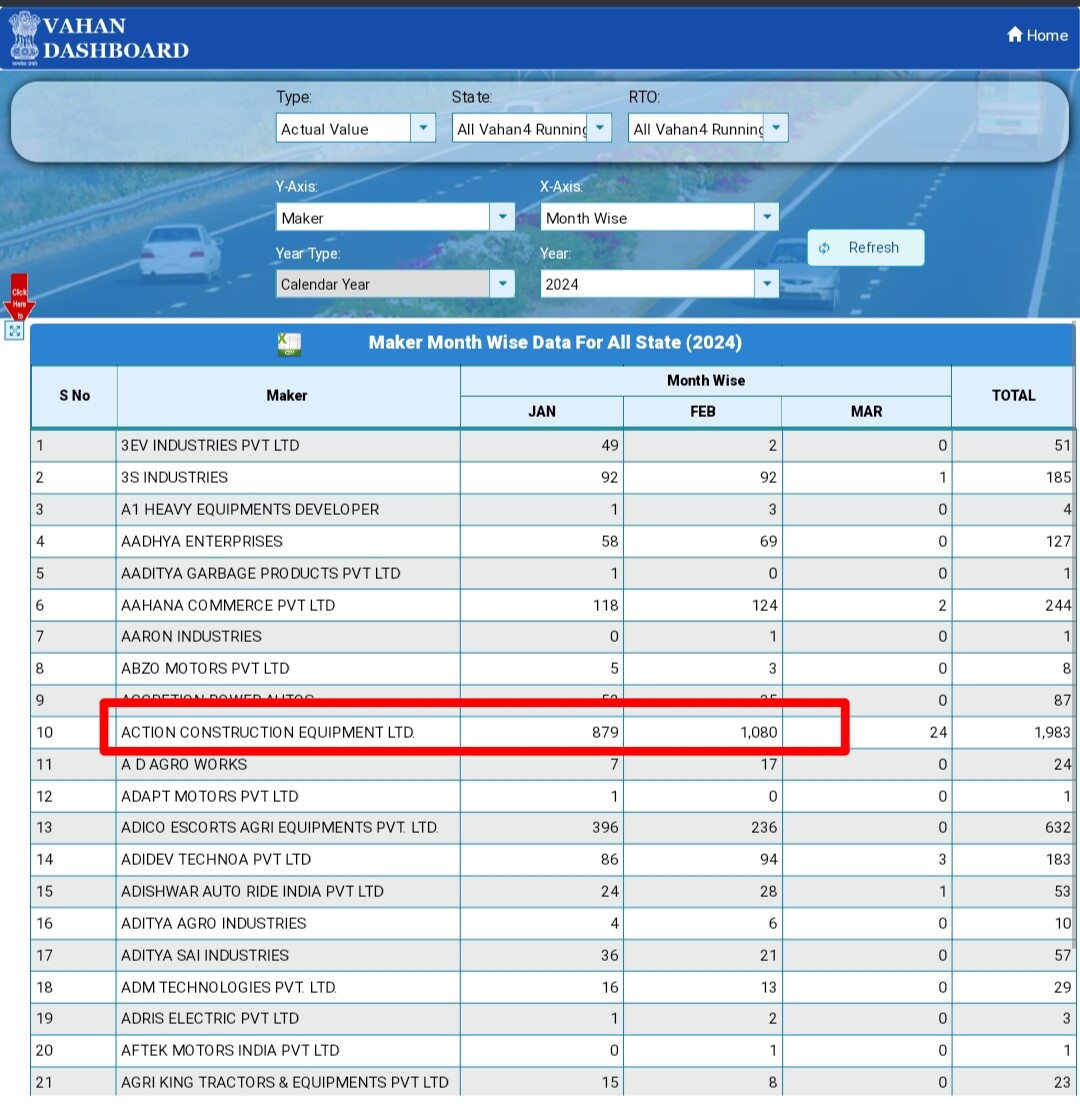

As per vahan data, good growth in Feb sales.

As per vahan data, good growth in Feb sales.

I am holding this stock for couple of years and the only reason is management. Vishnu raju garu and his father is a very popular and known educationalist and have multiple colleges. They were also doing subcontracting for Cera and other main tile manufactures but later sold the plant i think.

Vishnu Raju son aditya vissam is managing the company but could not see agressive exapnsion plans or reorganization plans. The growth is very slow and invest with risks known

At a business level, they are catering to small geography area and operating in retail and distribution model. Margins are not that great. Need to see how they are gng to progress.

Please read the annual report

All resolutions were passed

https://www.bseindia.com/xml-data/corpfiling/AttachHis/3b4e4f90-1152-4ffd-9c2f-092b2357e883.pdf

More Selling by Peterhouse.

Notes from the Transcript of Management Commentary on Annual Audited Financial Results

Margins

2023 review

Outlook

External challenges

CAQM relief and impact

(Commission for Air Quality Management)

Reason for poor performance vis-a-vis competition

Muje Aesi Company Ke Nam Janane Hai Ki

Jis Company Ki Product Ko Aap Use Kar Rahe Ho

Aor Us Company Ki Product Apako Bahot Hi Jada Pasand A Rahi Hai

Aor

Abhi Voh Company Bahot Choti Ho

Aor

Share Market Mai Listed Bhi Ho

Aesi

Bhavishya Me Apako Lagata Hai Ki Voh Company Multibagger Ban Sakati Hai Aesi Hiden Company Ke Nam Comment Mai Bataye

If the Supreme Court’s main concern is ensuring right to healthcare, that is a very complex issue that simply cannot be solved just by capping consultation fees and bed charges. The biggest hurdle in my opinion is the grossly skewed distribution of clinics, nursing homes and hospitals across rural and urban areas. Large swathes of the population in rural India have no access to even primary care. At the same time, big cities are swamped with more hospitals than the local population needs, leading to cut-throat competition and unethical practises just to survive. The reason for this is a big difference in the quality of life between these two places. Poor infrastructure, lack of good schools, employment opportunities for spouses, comfort amenities–all of these factors cause doctors to flock to the cities and grind it out rather than go to underserved areas where they will be not only be respected more, but earn more as well.

Solving discrepancy in healthcare access and availability is more than just making it cheap. It will require a general upliftment of the underserved regions. Capping charges is not going to do it.

Sold off Roto pumps, exports focused business can face issues due to shipping rates increase. Also I need to sell in order to buy.

Bought Time technoplast, it has been selling off weak parts of it’s global business, promising to reward share holders with the money and pay off debt partly. Mainly just bulk plastic containers and more recently composite gas cylinders, cng, lng, oxygen as of now, maybe even hydrogen. Doing some capex too. Demand has been strong with 80% capacity utilisation. Seems bit on cheaper side since natural gas prices are at record lows and composite cylinders are safer and lighter than steel, other businesses are also doing ok.

An updated chart,

2 points/ risks here to watch out for,

WMAs are looking to start into a declining slope, which never is a good sign from a momentum point of view.

RSI also is showing a declining trend. Still above 50 but close watch needs to be maintained.

As described in the post earlier, big red volume candle was not so encouraging. Might enter a consolidation stage if not further degradation.

A big green candle as a shoot up from 30 WMA might be encouraging in coming days. Of course this has to be after very low red candles (Signaling reduced volatility).

Disc. – No positions. Only for study purpose.

An updated chart,

2 points/ risks here to watch out for,

WMAs are looking to start into a declining slope, which never is a good sign from a momentum point of view.

RSI also is showing a declining trend. Still above 50 but close watch needs to be maintained.

As described in the post earlier, big red volume candle was not so encouraging. Might enter a consolidation stage if not further degradation.

A big green candle as a shoot up from 30 WMA might be encouraging in coming days. Of course this has to be after very low red candles (Signaling reduced volatility).

Disc. – No positions. Only for study purpose.