Does anybody know what happened with the EGM? There were proposal for stock split and bonus shares in January. Does anybody know what happened to that?

Posts tagged Value Pickr

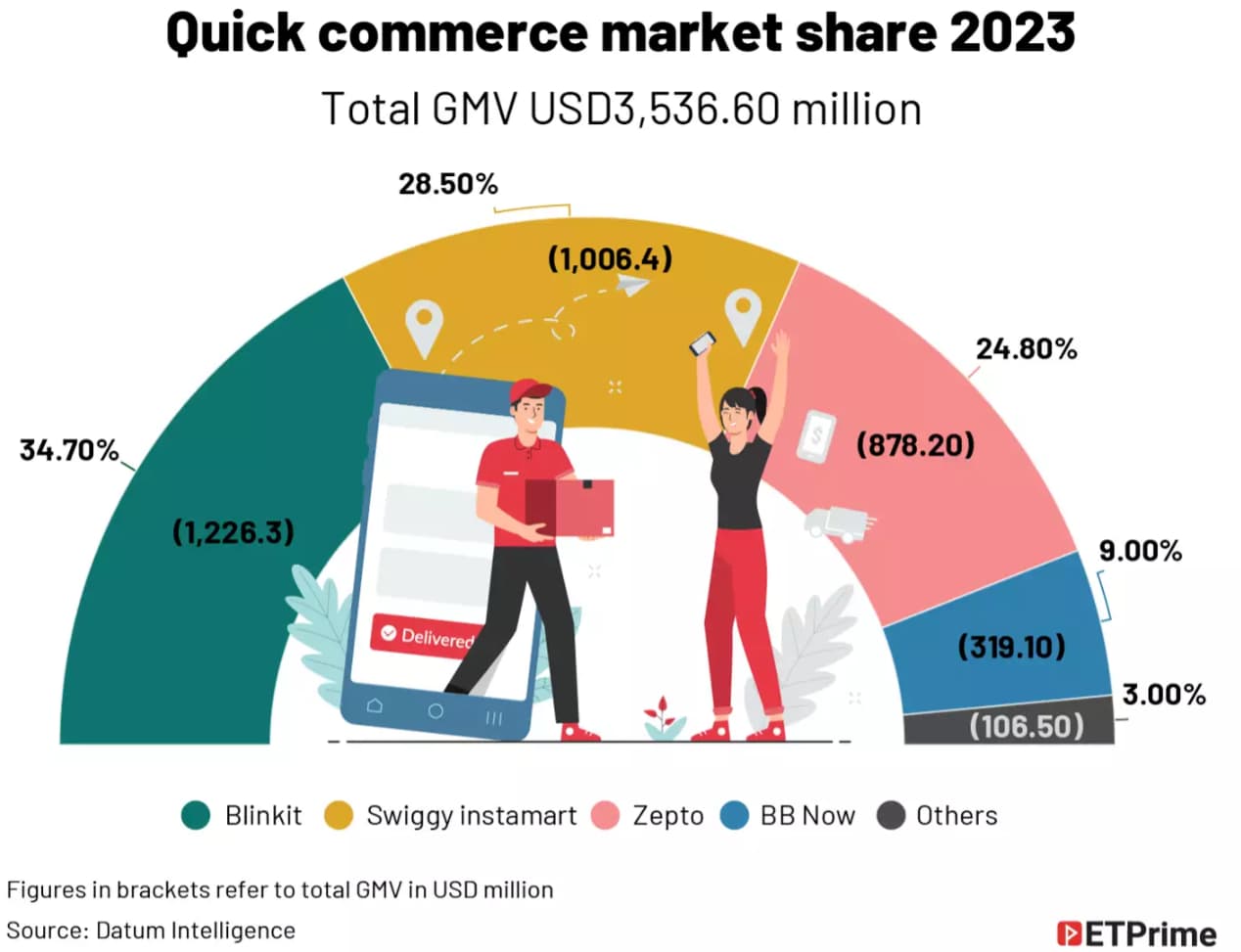

Buy Unlisted Shares (29-02-2024)

When was this? I got quoted 4050 but it was 2 weeks back.

How to register with SEBI as a Research Analyst? (29-02-2024)

any other courses for Research analyst for job any one knows please guide me

What’s the right price to enter? (29-02-2024)

Great question since it forces us to think on 2 critical dimensions – How to value?, and How to think about the prices?

Your primary question focuses on the outcome. Hence, it is easy to answer: Buy at a price which will remain the least price among all the future quotations. But, I agree that’s impossible. So, I think a better question to contemplate would be: How to judge that dream price? To do so, it becomes imperative to focus on the process, which is very specific to every individual and needs continuous refinement. Here is my thinking that precedes the process/approach:

- Firstly, no silver bullet exists.

- Secondly, price TREND [of excessive optimism and pessimism] in the near-term follows the technical and prevailing psychological factors [supply-demand, narratives, recent performance compared to prior expectations and adjusted earnings expectations]. However, Price CAGR follows the evolving fundamentals [earnings performance] in the long-term.

- Thirdly, analyze fundamentals to develop conviction. Look for mispriced opportunity, basis fundamentals [earnings growth, optionalities, nature of the business(terminal value, B2B Vs B2C, type of product(need-want-wish), opportunity size, Cyclical Vs. Structural demand, reliability of the cash flows), capital allocation etc.] that are yet be priced in.

- Finally, bear in thoughts that future outcomes are uncertain [amount and the timing of the cash flows, financial shenanigans, unexpected economic shocks such as COVID, red sea tension] and valuation is not only subjective [Investment horizon, Expected Returns] but also relative [current market state (bullish/bearish), sectoral tailwinds, liquidity in the system, intangibles (competitive advantages, financial strength, management) of the business that are very important but can’t be counted in the mathematical models].

What’s my approach? I start with a price chart to judge the current trend. It helps on 2 aspects: Easier to turn many names in a short span of time compared to pure fundamental based approach, & Forces to focus on the opportunities that are likely to provide better return in the current market environment. Trend will be one among below three:

- Up: Analyze fundamentals. Story seems interesting but the price has already run up too much. Start tracking and wait for price pull back (continuation patterns). Take position as and when opportunity knocks.

- Down: Analyze fundamentals. Story seems interesting but ignored by the market participants due to XYZ reasons. Start tracking. Wait for the completion and confirmation of the base formation patterns. On pattern confirmation, take position if fundamentals are still in place.

- Rangebound: Analyze fundamentals. Story seems interesting but undergoing time correction. Start tracking. Wait for the completion and confirmation of the trend. On pattern confirmation, take position if fundamentals are still in place.

In a nutshell, I suggest analyzing both fundamentals and technicals to improve your ability of stock picking. Basing the decision on this hybrid approach reduces the uncertainty and helps to ride the uptrend with better confidence. However, even the above approach is not a silver bullet. Ultimately, one will attain the best path to follow if one continues to work on his/her process with enthusiasm.

Corporate Fraud/Misdemeanor – Public Domain – India lessons (29-02-2024)

Sebi order. V-marc India SME listed. promoter provide finance to purchase own stock to manupulate price. wrongful gain of 6.38 cr.

Apar Industries (29-02-2024)

Notes of February 2024 concall –

(View : Bullish)

Cables: Elastomeric products and exports increased.

US and EU enquiries increased.

Increasing interest in HTLS lines:

Tenders are lined up.

Trend is positive but awarding of tenders may get delayed due to election.

High Temperature Low Sag Conductors (HTLS) can withstand operating temperatures of up to 210 °C, thus carrying higher power compared to conventional conductors.

Standardisation of conductors:

A transition is happening from ACSR to AL-59 alloys.

The upgrade in the specifications ACSR to AL-59 alloy has actually created a win-win situation for manufacturers like APAR as well as for transmission line owners. This results in a reduction in the total cost of ownership of the transmission lines. So, this effect may play out over the next few years. Few players are there in AL 59 products.

Higher technonolgy is involved in providing those products, the competitive intensity is lower. This product has lower weight and less corrosive properties. It’s already become now the default product.

EBIDTA could be 28500 Rs. Per metric ton for longer term.

Conductor division : Management expects 15% Volume growth next year.

Transformer oil:

Management is expecting double digit growth from domestic and export point of view.

APAR has higher market share in power transformer oils than distribution oils. It is prefered oil in higher capacity transformers. 800 kV HVDC which is the highest voltage type of transformer, APAR has more than 90% market share.

Cable business:

Management is expecting more orders from medium volatage cables ( high value product) than building wire / simple type of cable.

25-30% out of total sales come from elastomeric cables. Used in solar, wind, railway, defence, mining etc.

10% from OFC cables and remaining from power cables.

In FY 2023, cable exports contributed for 16% of total revenue. Cable business is expected to grow 25% for next few years.

There’s a big revival happening in the wind sector. And also, the government has recently come up with a new scheme where you can upgrade your old wind farms. Windmills of smaller capacity will be replaced by big capacity windmills.

Current capacity is 2,05,000 metric tons. Capacity will be added as per expected volume growth. Acquired properties/ cable manufacturers in Silvassa for scaling up business.

Red Sea crisis:

Exports to USA is less affected. Exports to west Africa and EU are taking 15-16 extra sailing days.

Deinventorization: APAR’s customers and distributors held inventory to avoid supply chain issues existed before.

APAR has kept almost 9 to 10 months of inventory, whereas the law has normally been holding 2 to 3 months. Customers are increasingly giving DDP dates. APAR is exporting that product 15-20 days early.

The DDP Incoterm, or “Delivery Duty Paid” Incoterm, states that the seller must make the goods available to the buyer at a prearranged location (buyer’s factory, warehouse etc.) and cover all associated expenses including unloading the goods from the carrier and any customs procedure costs and tariffs that may apply.

Under the DDP Incoterm, the seller bears full responsibility for all costs and risks until the goods have been unloaded at the agreed-upon location.

US Exports:

Management has confidence that US will be strategic market for them as they have received positive feedback from servicing customers. In EU still they are developing.

US imports cables worth of $19 billion. It is huge opportunity. APAR can cater to real estate sector and low voltage segment. Also approval is received for medium voltage cables upto 40,000 volts.

APAR is largest exporter to US, Polycab is close second. KEI caters to Australia.

Going forward company plans do capex of 300 Cr on annual basis. It will be Combination of brownfield expansion and debottlenecking. QIP money raised 1000 Cr will be utilised.

In Europe, APAR is focused more around the renewable energy side. In the US, there more sectors that are covering. APAR has contract with Enel (Italian utility)

Outlook for the year ahead would be conductors 15% plus, cables-20-25%.

In oils – transformer oils double digit.

Transformer oil : Guidance of EBIDTA of 5500 Rs per KL already achieved. Current EBIDTA is 6125 Rs per KL.

Lubricant: Volume are always under pressure because of drain intervals of oil products. Volume growth could be in the range 2-3%.

Chinese competition:

In certain simple construction conductors the US market is still not flooded with Chinese products. It will not be that easy for them to sell in large quantities there.

Chinese are trying to route products through Vietnam and some of these other geographies. Moment the Chinese try to route it through another geography it adds significantly to the supply chain costs. They no longer can be as competitive as they are from China.

In January, February the profitability and the margin will come down.

Disclaimer: Invested

Apar Industries Feb 2024 concall notes.docx (352.6 KB)

SKM Egg Products – thinking out of the shell (29-02-2024)

Hi What is the source of Information details

Gulshan Polyols(GPL) – Business by FMCG and Valuation by Commodity (29-02-2024)

Gulshan Polyols Ltd

Gulshan Polyols Ltd, with over 30 years of expertise, specializes in Ethanol/Bio-fuel, Grain, and Mineral-based products, and is expanding its operations, especially in the Indian bio-ethanol sector, under its commitment to sustainable growth themed “Expanding Potential”.

MCap: Rs 1,308

Sales (TTM): Rs 1,234 Cr

Sales:MCap 0.95 times

CMP: Rs 210

PE: 39.60 times

PB: 2.26 times

BV: Rs 92.80

EPS: 5.29

ROCE: 8.68%

ROE: 7.81%

Sales Growth 3 yrs CAGR: 23.90 %

Profit Growth 3 yrs CAGR: 28.20 %

Borrowings: Rs 358 Cr & Reserve and Capital : Rs 579 Cr.

Financial Performance:

![]() Q2 FY23 income from operations was ₹277.38 crores, stable due to high capacity utilization and strong product demand.

Q2 FY23 income from operations was ₹277.38 crores, stable due to high capacity utilization and strong product demand.

![]() Input costs increased by 13.2% YoY, mainly due to higher raw material and power costs.

Input costs increased by 13.2% YoY, mainly due to higher raw material and power costs.

![]() EBITDA for the quarter was ₹20 crores (7.3%), net profit ₹9 crores with a PAT margin of 3.3%.

EBITDA for the quarter was ₹20 crores (7.3%), net profit ₹9 crores with a PAT margin of 3.3%.

![]() H1 FY23 revenue was ₹548 crores, up 6% YoY.

H1 FY23 revenue was ₹548 crores, up 6% YoY.

![]() The company targets a sustainable margin of 10-12%.

The company targets a sustainable margin of 10-12%.

Expansion Plans:

Grain Processing Segment:

![]() Products: This segment includes sorbitol, maize starch, liquid glucose, fructose syrup, and other starch derivatives such as Malto Dextrine and Dextrose Monohydrate, along with agro-based animal feed.

Products: This segment includes sorbitol, maize starch, liquid glucose, fructose syrup, and other starch derivatives such as Malto Dextrine and Dextrose Monohydrate, along with agro-based animal feed.

![]() Facilities and Capacities: The company has production facilities in Muzaffarnagar, Uttar Pradesh, and Bharuch, Gujarat. Muzaffarnagar specializes in producing maize starch (70,000 metric tons per annum) and fructose syrup (36,000 metric tons per annum), while the Bharuch facility focuses on sorbitol production (72,000 metric tons per annum).

Facilities and Capacities: The company has production facilities in Muzaffarnagar, Uttar Pradesh, and Bharuch, Gujarat. Muzaffarnagar specializes in producing maize starch (70,000 metric tons per annum) and fructose syrup (36,000 metric tons per annum), while the Bharuch facility focuses on sorbitol production (72,000 metric tons per annum).

![]() Capacity Utilization and Expansion: The combined capacities in this segment are about 150,000 metric tons per annum. Currently operating at full capacity, the company plans a 20% capacity expansion to meet growing domestic and export demand.

Capacity Utilization and Expansion: The combined capacities in this segment are about 150,000 metric tons per annum. Currently operating at full capacity, the company plans a 20% capacity expansion to meet growing domestic and export demand.

![]() Customer Base: The segment serves a strong customer base, including FMCG companies like Lever, Dabur, Asian Paint, and Patanjali. The products are also exported to over 35 countries. Starch, particularly, sees robust demand from the semi-craft paper industry, driven by e-commerce growth.

Customer Base: The segment serves a strong customer base, including FMCG companies like Lever, Dabur, Asian Paint, and Patanjali. The products are also exported to over 35 countries. Starch, particularly, sees robust demand from the semi-craft paper industry, driven by e-commerce growth.

Ethanol and Distillery Segment:

![]() Current Operations: The company operates a 60 KLPD grain-based ethanol plant and distillery in Chhindwara, Madhya Pradesh, running at 110% capacity utilization. This facility was set up in 2020.

Current Operations: The company operates a 60 KLPD grain-based ethanol plant and distillery in Chhindwara, Madhya Pradesh, running at 110% capacity utilization. This facility was set up in 2020.

![]() Expansion Plans: As part of the government’s Ethanol Blended Petrol Program (EBPP), the company plans to enhance capacity from 60KLPD to 500 KLPD by Quarter 4 of the current financial year. Additionally, a new 250 KLPD grain-based ethanol plant is being set up in Goalpara, Assam, expected to be operational by FY25.

Expansion Plans: As part of the government’s Ethanol Blended Petrol Program (EBPP), the company plans to enhance capacity from 60KLPD to 500 KLPD by Quarter 4 of the current financial year. Additionally, a new 250 KLPD grain-based ethanol plant is being set up in Goalpara, Assam, expected to be operational by FY25.

Mineral Processing Segment:

![]() Products: This segment produces various grades of calcium carbonate, including precipitated and brown calcium carbonate.

Products: This segment produces various grades of calcium carbonate, including precipitated and brown calcium carbonate.

![]() Applications: The calcium carbonate products are primarily used in the paper and PVC industries.

Applications: The calcium carbonate products are primarily used in the paper and PVC industries.

![]() Contribution: Though smaller compared to the other segments, this segment makes a significant contribution to the business.

Contribution: Though smaller compared to the other segments, this segment makes a significant contribution to the business.

CAPEX and Funding:

![]() Spent INR 250 crore of a total INR 600 crore CAPEX, with INR 350 crore pending.

Spent INR 250 crore of a total INR 600 crore CAPEX, with INR 350 crore pending.

![]() Ethanol expansion funded through term loans, QIP, and internal accruals.

Ethanol expansion funded through term loans, QIP, and internal accruals.

![]() Eligible for Production Linked Fiscal Assistance for Greenfield ethanol plants in Madhya Pradesh and Assam.

Eligible for Production Linked Fiscal Assistance for Greenfield ethanol plants in Madhya Pradesh and Assam.

![]() ISS approval from DFPD for bank funding reduces funding costs.

ISS approval from DFPD for bank funding reduces funding costs.