Interesting insights. While researching deeper about the company I couldn’t find transcript of concalls and investor presentation (except for October 22). Are there any other sources from where we can get any idea about the management’s current view and outlook of the business?

Posts tagged Value Pickr

Narayana Hrudayalaya Ltd (24-02-2024)

Q3 FY24 Concall notes

Financial Performance:

- Consolidated Revenue: INR 12,036 million (+6.7% YoY, -7.8% QoQ).

- Consolidated EBITDA: INR 3,968 million (24.7% margin in Q3 FY24).

Cayman Units Business:

- HCCI and EICL Quarterly Revenue: USD 30.6 million (+8.5% YoY).

- Confidence in Caribbean business growth through strategic initiatives.

Financial Position:

- Strong balance sheet with INR 10.39 billion cash.

- Net cash position: INR 0.25 billion as of December 31, 2023.

Capital Expenditure:

- Outlay close to INR 5 billion till December 2023.

Clinical Achievements:

- Successful organ and bone marrow transplants, robotic procedures.

- Rare renal transplants and critical case recovery in Mumbai.

Digitization and Transformation:

- 8% QoQ throughput increase, 3.3% NH Labs turnaround time reduction.

- AADI app saves 2500 surgeon hours, NAMAH app saves 83 nursing hours monthly.

Narayana Health Integrated Care:

- Revenue crosses INR 53 million with 42,000+ patient transactions.

Q3 Domestic Business Performance

- Low Growth:

- Seasonality impact, notably in North and West regions.

- Higher impact in Gurugram; underperformance in Jaipur due to unviable RGHS reimbursements.

- Payor Mix Rationalization:

- Focus on improving payor mix (cash and insurance up by 2%, schemes down by 2%).

- Positive impact on margin despite challenges.

- Exit from M S Ramaiah and Bellary contracts for strategic focus.

- Impact of Jaipur Hospital:

- Unquantified but significant underperformance, particularly in North.

- Jaipur unit majorly contributes to the overall underperformance.

Capex Timeline:

- Cayman unit’s Capex almost complete; hospital commissioning expected in the first half of the next year.

- Bangalore and Kolkata units take 2-3 years for completion.

- Acquired land in Kolkata; permissions applied for building in Bangalore.

- Exploring additional capacity options in Bangalore and Kolkata.

New Hospitals Performance:

- Faced seasonality impact more than flagship units.

- Combined EBITDA around 4%, down from 7% in Q2.

- Dharamshila performed the best.

- Expecting a strong recovery in the last quarter to approach the target for the next two quarters.

Insurance Business Update:

- Received license in early January.

- Planning to go live next year, starting in Karnataka (Mysore) and gradually expanding to other geographies.

India Business Discharges:

- Single-digit growth observed in full-year discharges.

- Explanation: efforts to improve payor mix, focus on efficiency, and digital initiatives.

- ARPOBS growth noted despite lower discharges, attributed to throughput improvement.

Other Expenses Decrease:

- YoY decrease noted in other expenses.

- One-time factors impacting Q3, anticipation of saved expenses not necessarily deferred.

Lease Modification in Other Income:

- INR 159 million related to lease modification in other income.

- Explanation: periodic lease renegotiations with third-party partners, affecting non-owned hospitals.

Manpower Cost Increase:

- Double-digit YoY growth observed in manpower costs.

- Emphasis on challenges due to government actions on minimum wages.

- Solutions: operational efficiency, digitization, and NAMAH app implementation.

Wage Inflation History:

- 10-12% wage inflation observed for FY24, similar expectations for FY25.

- Explanation: post-COVID, increased inflation, recovery expected through efficiency and price adjustments.

Longer-Term Capital Allocation:

- Key Priorities:

- Focus on winning greater market share in Bangalore and Kolkata.

- Bulk of investment for the next decade directed to these geographies.

- Expansion Strategies:

- Strengthening existing hospital set through:

- Adding more beds.

- Adjacent capacity expansion.

- Combination of Brownfield and Greenfield investments in hospitals, clinics, and pharmacies.

- Strengthening existing hospital set through:

Assessment of Supply Side:

- Current Market Dynamics:

- Mature cities in India have an adequate supply of hospital beds.

- Shift in patient preference from unorganized to accredited hospitals.

- Majority of corporate healthcare groups concentrated in large cities.

- Demand Dynamics:

- Demographics favor growth with rising incomes and aging population.

- Opportunity set deemed tremendous despite existing competition.

Anticipating Insured Mix vs. Out-of-Pocket:

- Current Scenario:

- Organized payors constitute 20%-22% of the mix.

- Aspiration to reach industry peers’ numbers (40%-50%).

- Evolution Timeline:

- Acknowledgment that achieving peer numbers may take longer.

- Aspiration to transition from a legacy of providing low-cost, subsidized services.

Overall Strategy:

- Long-Term Focus:

- Commitment to long-term growth in key markets.

- Balancing expansion between existing and new facilities.

- Quality Over Quantity:

- Emphasis on high-quality beds rather than sheer quantity.

- Recognition of a shifting preference towards accredited healthcare providers.

- Demographic Advantage:

- Leveraging favorable demographics for sustained demand.

- Viewing competition as a part of the overall growth narrative.

Changing Patient Demand:

- Shift towards seeking routine surgeries closer to home.

- Corporate hospitals adapting to advanced procedures like heart and cancer surgeries.

- Strategic investments to expand accessibility for diverse diseases.

Impact on ROCE:

- Short-term dilution due to expansion efforts and increased footprint.

- Balancing financial considerations with growth opportunities.

- Moderate acquisitions to manage financial impact.

Tech Initiatives:

- Patient-facing app, NH Care, centralizes hospital services for convenience.

- Features include appointment booking, test payment, results viewing, and doctor information.

- Integration into NH Integrated Care Plan and QR code system in progress.

Research and Publications:

- Robust medical research wing with a focus on clinical and basic science research.

- Incentives for staff engagement in research, resulting in 200+ publications last year.

- Leveraging electronic medical records for comprehensive data analysis and clinical trials.

Tax Rate:

- Similar tax rate expected next year.

- Moderated by the mix between India and Cayman operations.

Capex:

- Next year’s capex around INR 1000-1200 crores.

- Funding through bank borrowings, NCD raise, and internal accruals.

- Higher debt-to-EBITDA ratio expected in the medium term.

Capex Composition:

- General capex of approx. INR 450 crores. (India focused)

- Expansion-focused capex in Bangalore, Kolkata, and Raipur.

- Cayman-specific capex includes regular and new hospital expenses.

Sparsh Acquisition:

- Sparsh meeting projections, maintaining margins.

- Acquisition benefits include cost rationalization and additional capacity creation.

Cayman Expansion:

- New hospital in Cayman aiming to start by June.

- Frontloaded fixed costs mitigated by market familiarity.

- Anticipating swift climb over initial fixed costs due to high operating leverage.

Narayana Hrudayalaya Ltd (24-02-2024)

Q3 FY24 Concall notes

Financial Performance:

- Consolidated Revenue: INR 12,036 million (+6.7% YoY, -7.8% QoQ).

- Consolidated EBITDA: INR 3,968 million (24.7% margin in Q3 FY24).

Cayman Units Business:

- HCCI and EICL Quarterly Revenue: USD 30.6 million (+8.5% YoY).

- Confidence in Caribbean business growth through strategic initiatives.

Financial Position:

- Strong balance sheet with INR 10.39 billion cash.

- Net cash position: INR 0.25 billion as of December 31, 2023.

Capital Expenditure:

- Outlay close to INR 5 billion till December 2023.

Clinical Achievements:

- Successful organ and bone marrow transplants, robotic procedures.

- Rare renal transplants and critical case recovery in Mumbai.

Digitization and Transformation:

- 8% QoQ throughput increase, 3.3% NH Labs turnaround time reduction.

- AADI app saves 2500 surgeon hours, NAMAH app saves 83 nursing hours monthly.

Narayana Health Integrated Care:

- Revenue crosses INR 53 million with 42,000+ patient transactions.

Q3 Domestic Business Performance

- Low Growth:

- Seasonality impact, notably in North and West regions.

- Higher impact in Gurugram; underperformance in Jaipur due to unviable RGHS reimbursements.

- Payor Mix Rationalization:

- Focus on improving payor mix (cash and insurance up by 2%, schemes down by 2%).

- Positive impact on margin despite challenges.

- Exit from M S Ramaiah and Bellary contracts for strategic focus.

- Impact of Jaipur Hospital:

- Unquantified but significant underperformance, particularly in North.

- Jaipur unit majorly contributes to the overall underperformance.

Capex Timeline:

- Cayman unit’s Capex almost complete; hospital commissioning expected in the first half of the next year.

- Bangalore and Kolkata units take 2-3 years for completion.

- Acquired land in Kolkata; permissions applied for building in Bangalore.

- Exploring additional capacity options in Bangalore and Kolkata.

New Hospitals Performance:

- Faced seasonality impact more than flagship units.

- Combined EBITDA around 4%, down from 7% in Q2.

- Dharamshila performed the best.

- Expecting a strong recovery in the last quarter to approach the target for the next two quarters.

Insurance Business Update:

- Received license in early January.

- Planning to go live next year, starting in Karnataka (Mysore) and gradually expanding to other geographies.

India Business Discharges:

- Single-digit growth observed in full-year discharges.

- Explanation: efforts to improve payor mix, focus on efficiency, and digital initiatives.

- ARPOBS growth noted despite lower discharges, attributed to throughput improvement.

Other Expenses Decrease:

- YoY decrease noted in other expenses.

- One-time factors impacting Q3, anticipation of saved expenses not necessarily deferred.

Lease Modification in Other Income:

- INR 159 million related to lease modification in other income.

- Explanation: periodic lease renegotiations with third-party partners, affecting non-owned hospitals.

Manpower Cost Increase:

- Double-digit YoY growth observed in manpower costs.

- Emphasis on challenges due to government actions on minimum wages.

- Solutions: operational efficiency, digitization, and NAMAH app implementation.

Wage Inflation History:

- 10-12% wage inflation observed for FY24, similar expectations for FY25.

- Explanation: post-COVID, increased inflation, recovery expected through efficiency and price adjustments.

Longer-Term Capital Allocation:

- Key Priorities:

- Focus on winning greater market share in Bangalore and Kolkata.

- Bulk of investment for the next decade directed to these geographies.

- Expansion Strategies:

- Strengthening existing hospital set through:

- Adding more beds.

- Adjacent capacity expansion.

- Combination of Brownfield and Greenfield investments in hospitals, clinics, and pharmacies.

- Strengthening existing hospital set through:

Assessment of Supply Side:

- Current Market Dynamics:

- Mature cities in India have an adequate supply of hospital beds.

- Shift in patient preference from unorganized to accredited hospitals.

- Majority of corporate healthcare groups concentrated in large cities.

- Demand Dynamics:

- Demographics favor growth with rising incomes and aging population.

- Opportunity set deemed tremendous despite existing competition.

Anticipating Insured Mix vs. Out-of-Pocket:

- Current Scenario:

- Organized payors constitute 20%-22% of the mix.

- Aspiration to reach industry peers’ numbers (40%-50%).

- Evolution Timeline:

- Acknowledgment that achieving peer numbers may take longer.

- Aspiration to transition from a legacy of providing low-cost, subsidized services.

Overall Strategy:

- Long-Term Focus:

- Commitment to long-term growth in key markets.

- Balancing expansion between existing and new facilities.

- Quality Over Quantity:

- Emphasis on high-quality beds rather than sheer quantity.

- Recognition of a shifting preference towards accredited healthcare providers.

- Demographic Advantage:

- Leveraging favorable demographics for sustained demand.

- Viewing competition as a part of the overall growth narrative.

Changing Patient Demand:

- Shift towards seeking routine surgeries closer to home.

- Corporate hospitals adapting to advanced procedures like heart and cancer surgeries.

- Strategic investments to expand accessibility for diverse diseases.

Impact on ROCE:

- Short-term dilution due to expansion efforts and increased footprint.

- Balancing financial considerations with growth opportunities.

- Moderate acquisitions to manage financial impact.

Tech Initiatives:

- Patient-facing app, NH Care, centralizes hospital services for convenience.

- Features include appointment booking, test payment, results viewing, and doctor information.

- Integration into NH Integrated Care Plan and QR code system in progress.

Research and Publications:

- Robust medical research wing with a focus on clinical and basic science research.

- Incentives for staff engagement in research, resulting in 200+ publications last year.

- Leveraging electronic medical records for comprehensive data analysis and clinical trials.

Tax Rate:

- Similar tax rate expected next year.

- Moderated by the mix between India and Cayman operations.

Capex:

- Next year’s capex around INR 1000-1200 crores.

- Funding through bank borrowings, NCD raise, and internal accruals.

- Higher debt-to-EBITDA ratio expected in the medium term.

Capex Composition:

- General capex of approx. INR 450 crores. (India focused)

- Expansion-focused capex in Bangalore, Kolkata, and Raipur.

- Cayman-specific capex includes regular and new hospital expenses.

Sparsh Acquisition:

- Sparsh meeting projections, maintaining margins.

- Acquisition benefits include cost rationalization and additional capacity creation.

Cayman Expansion:

- New hospital in Cayman aiming to start by June.

- Frontloaded fixed costs mitigated by market familiarity.

- Anticipating swift climb over initial fixed costs due to high operating leverage.

Jindal Stainless (Hisar) (24-02-2024)

Factor investing in railways – Jindal Stainless website

Jindal Stainless (Hisar) (24-02-2024)

Factor investing in railways – Jindal Stainless website

MTAR Technologies – A wager on innovation meeting economies of scale (24-02-2024)

Thank you @siddybee for typing these answers ![]() . Overall, I have to say that I was quite pleased with the concall.

. Overall, I have to say that I was quite pleased with the concall.

I am very excited about answer number 5. Electrolyzers, given the way the world is evolving, are going to be a big deal. At this stage, I believe only one company manufactures electrolyzers at scale in this country. There is a lot of talk among other players, but no one else has started mass manufacturing them, to my knowledge (please correct me if I am wrong).

MTAR has proven that they can batch manufacture electrolyzers for Bloom Energy. So, contingent on Bloom Energy getting orders for these devices, I expect that the transition to mass manufacturing on MTAR’s end should be fairly smooth.

I agree with @murali603 that there will be some contribution from this vertical in FY24-25, and I also appreciate that management is being very conservative with guidance this time around. Personally, I hope that we have a hockey stick growth moment late in FY24-25 over here, but that’s just me being bullish.

Disclosure of holding: I started buying MTAR Technologies in August 2022, at a price of ₹1422. My cost basis has moved up to ₹1555. I have a fairly concentrated portfolio, and do not hold more than 10 companies at any given time.

MTAR Technologies – A wager on innovation meeting economies of scale (24-02-2024)

Thank you @siddybee for typing these answers ![]() . Overall, I have to say that I was quite pleased with the concall.

. Overall, I have to say that I was quite pleased with the concall.

I am very excited about answer number 5. Electrolyzers, given the way the world is evolving, are going to be a big deal. At this stage, I believe only one company manufactures electrolyzers at scale in this country. There is a lot of talk among other players, but no one else has started mass manufacturing them, to my knowledge (please correct me if I am wrong).

MTAR has proven that they can batch manufacture electrolyzers for Bloom Energy. So, contingent on Bloom Energy getting orders for these devices, I expect that the transition to mass manufacturing on MTAR’s end should be fairly smooth.

I agree with @murali603 that there will be some contribution from this vertical in FY24-25, and I also appreciate that management is being very conservative with guidance this time around. Personally, I hope that we have a hockey stick growth moment late in FY24-25 over here, but that’s just me being bullish.

Disclosure of holding: I started buying MTAR Technologies in August 2022, at a price of ₹1422. My cost basis has moved up to ₹1555. I have a fairly concentrated portfolio, and do not hold more than 10 companies at any given time.

Deepak’s portfolio requesting feed back (24-02-2024)

Past performance is no guarantee for future years. The main issue is with no order bidding in the pipeline or no big order wins in recent history. Also they have ventured in to EPC recently to bid orders from railways. Otherwise road construction is not a niche business with so many competition(especially NCC with huge order backlog). I’m just saying there is a perfect explanation why market have rated it low. Especially with no order bidding pipeline with elections looming one can revisit this counter at leisure. Upside is limited and downside seems protected (due to lot of MF holdings) . I’m offloading at my own pace.

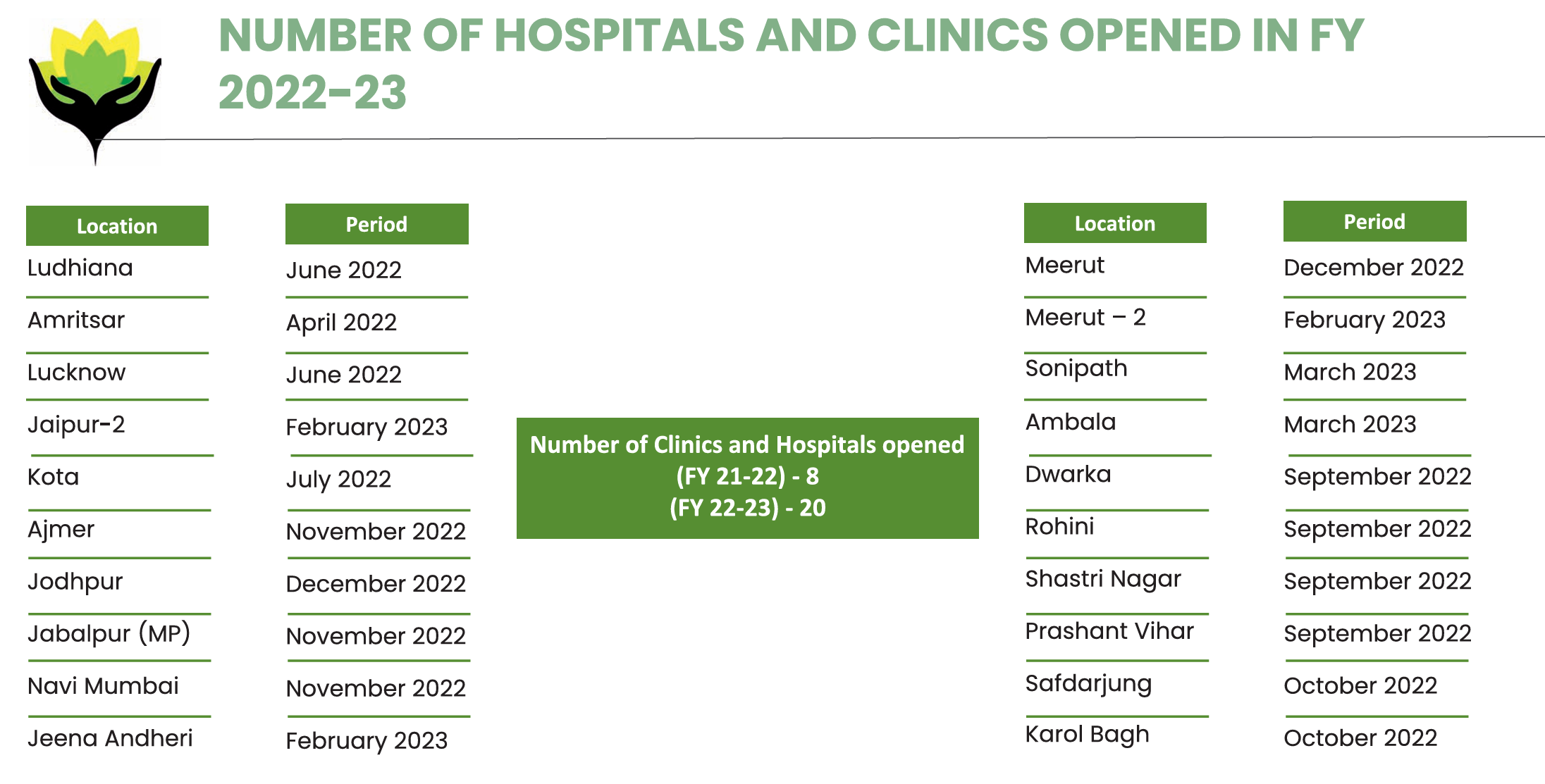

JEENA SIKHO- seems shady, one off? (24-02-2024)

25 Clinics/hosps added in the CFY till date…thats approx an increase of 320 rooms

12 Clinics/105 rooms in H2… still a month plus to go!

Rush of updates on empanelment with Health Ins Firms (a few major ones), probably this expands the possibility of increase in footfall (being cashless transactions).

Intellect Design Arena (24-02-2024)

In case you have not heard why Teminos woes Nilesh Shah is referring here it is. This is the best thing that could have happened to Intellect the last few months.

This report will report create doubts in the minds of perspective customer which are being targeted by Intellect as well. Plus Teminos has a large user base in Europe, which is focus area for Intellect.

Key beneficiaries of this will be for large deal. However due to size, it takes long time to seal a deal. Looking at the trouble of Teminos, I think IDA shall report better deal win in the next 3/4 quarters IMO.

https://hindenburgresearch.com/temenos/

Note: Invested