Posts tagged Value Pickr

NCC: Extremely undervalued (22-02-2024)

At the same time, NCC is in a much better position than ever so far

They have consistently brought down the debt levels

They have sold off most of their non core business and is focussing primarily on core business (more than 90% of the revenue, the remaining in mines & realty)

Unlike the inefficient planning & execution of 2007/08 infrastructure projects from the then government, the current govt seems to be good in planning & execution of the same (at least so far and I hope it continues at least for next 5 – 10 years

If NCC had a PE multiple of around 14 earlier, should the above mentioned positives warrant a better valuation multiple?

(Al though, I personally feel Price to book is a better mechanism for EPC companies as they don’t have much assets)

Shilchar Technologies – Power & Distribution Transformers – Sunrise Sector? (22-02-2024)

What is the lifespan of the kind of transformer used in Solar & Wind? As per different articles, it seems to be 25 years, but would be helpful if someone knows more on it.

That would help us understand the repeatability of orders.

Himachal Futuristic communication (22-02-2024)

From my understanding, every stock has an operator, an operator can be an individual, group or institution who have major stake in any company. And they have control over the price because they have the funds and the volume.

For example if I have 10-15% stake in a company and I sell all at once, the price will drop drastically and it will create further panic among retailers or other institutions dragging the price further. Then, once the stock is down 30-40% , I can get back in and buy my shares if I am sure of the fundamentals.

Pump and dump are operated stocks but are used for smaller market cap companies with very bad fundamentals.

Tata Investment Corporation: Unusual discount to NAV (22-02-2024)

Maybe some news on Tata Asset Management is possible as it owns 32% in TAM.

No other reason i can think of.

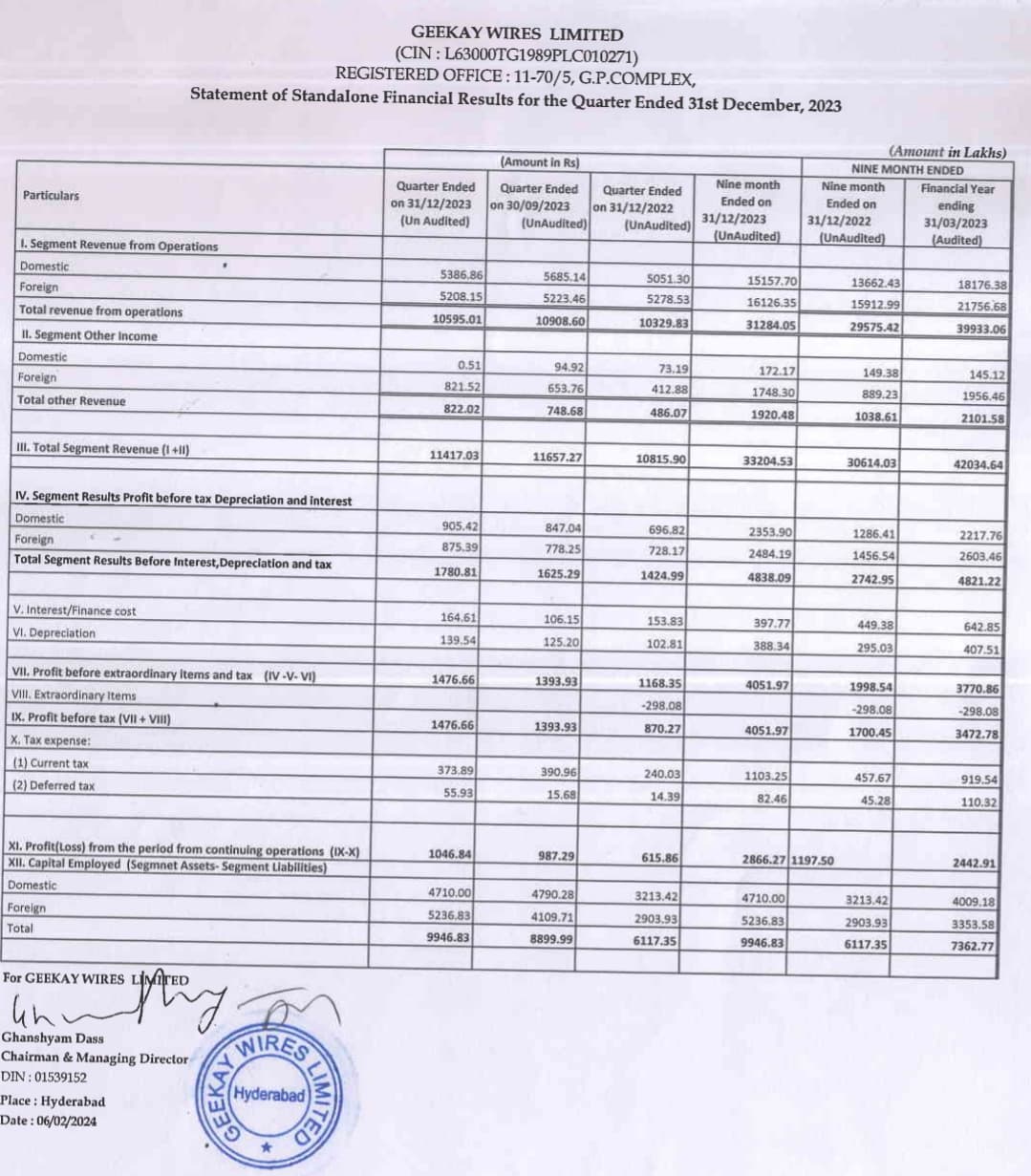

Geekay Wires Ltd (22-02-2024)

Q3FY24 Results update:

-The concern is same, topline growth is flate in last 4-6 Qtr

-Domestic sales increased by 6.5%, whereas exports are almost flat YoY

-Domestic is still okay, but exports are concern as foreign markets lacks Capex

-In AGM told peak revenue can be 10% higher

-Doing Capex but very less I feel

-Margin has also started stabilizing around 8-10%

-OI is volatile

-The game of valuation is almost played out; while investing my peak PE estimate was 15-18x as products are commodity in nature (also biz out of 2% circuit limit)

-Next Qtr is a high base Qtr (has high PAT & Sales)

-Next Qtr will decide, whether stock would be peak or new things emerges

Disc: Invested (No transaction in last 30 days)

PayTM (One 97 Communications Ltd) (22-02-2024)

Why do you think Paytm bank was the reason for it lagging behind in upi

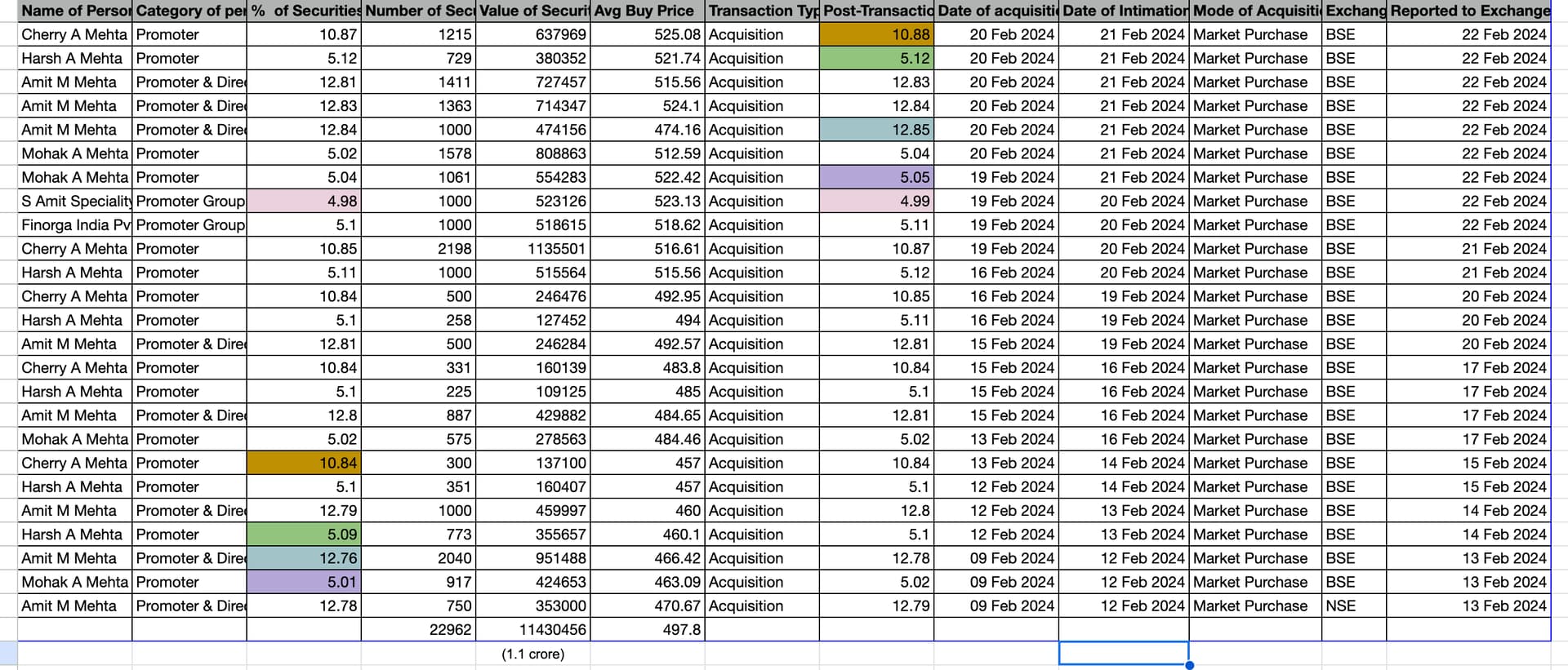

Diamines and Chemicals Ltd – Navigating for a long-term growth (22-02-2024)

I have been following this company for over 6 months now.

Recently (this month), the promoter group has been buying almost everyday.

They have directly bought from market during 7 trading days this month.

In the attached image, one can find the buying transactions.

I have one question, why are they buying everyday, instead they could have bought one single day.

One likeable reason could be, very less liquidity of shares that trade on a daily basis.

There was a rise in daily volumes today.

On normal days the daily volume would be around 15k

Today it touched 150k with 40% delivery.

I have taken a tracking position today at 550 level and plan to buy at bulk around 480 levels.

Anyone else here actively following this co.? Any insights will be highly appreciable.

Thanks.

Ujjivan Financial – Small Finance Bank (22-02-2024)

Hindu Interview by CEO Summary

Net NPA in Q3 From 0 → 0.16 per cent

Industry high growth for two years + two festival months in Q3.

Collections began to slacken a little bit

Punjab situation and TN floods → there’s a more bit of stress to come

60:40 mix unsecured vs secured is taking time.

last year we put together a changed model; introduced this year.

We have done that with MSME and housing;

gold is relatively new.

Model → FY25 and will begin to push the secured portfolio at a faster rate wrt FY24.

We have 16 area offices which will work like hubs and spokes.

Where – business, credit, legal, and operations teams work to get TAT (turnaround time) reduces.

Better credit monitoring.

In FY25, should see 66:33 as a split unsecured vs secured loans.

New product launches ?

Coming out in a new avatar with our secured products.

For MSME: product focus wrt working capital against long-term

Working with a couple of fintechs.

Reintroducing vehicle loans, (few pockets initially – do it well then go deep).

Focus next 2-3 yrs on our digital offering.

Would you look at acquisitions to boost your secured book?

If the secured (book) growth is not keeping pace with the targets, we will,

if secured products start firing , we may be able to delay the process.

At what stage are we in the reverse merger?

final approval from NCLT – 2-3 months.

Your universal bank aspirations?

For next three years, we will continue to be a small finance bank.

be the best small finance bank. THen we’ll find favor with the RBI for the next level.

roadmap → eventually a universal bank

There are talks of rate cuts now?

SFBs, private banks/ nationalized banks will have higher rates, irrespective of the repo rate.

For SFBs, the premium is there to stay, (we’d like to reduce that gap).

Smaller private banks are overtaking us + have reached our deposit rates.

It’s no longer a level playing field.

It depends on each one’s books and requirements.

you’re 70-years age. What after Dec 2024?

extension (for me) is out of question.

The NRC (nomination and remuneration committee) has started finding a successor.

Person is able to fall in line with the requirements and is ‘fit and proper’ , we can have external person.

Creative Peripherals (now Creative Newtech) – Micro cap with big ambitions (22-02-2024)

| Description | Net profit | Rationale |

|---|---|---|

| Enterprise Business | 35 | Steady Cash cow business the company can do 2% margin and management has presented it’s content to continue to do the same since the same is -Ve working capital cycle business Implying the growth rate of 4-5% the company can do 1750 crores of EB sale which is bare minimum |

| Brand Licensing Business | 60.9 | Assuming that company does 500 crores of honeywell business and 300 crores of Cyber power business the NP margin can be 12% (15% EBITDA and 16% tax for Hongkong) @77% stake and for cyberpower @51% stake doing 10% PAT margins |

| 95.9 |

Did a bit modeling for picture how the same will look 2.25 years down the line

I think 1750 crores of sales is extremely possible in EB segment can even go above 2000 crores

Now for Honeywell They have targeted the sales of 500 crores 2.25 years down the line but 270 crores 1 year down the line, couldn’t get the chance to ask non linear Jump in earnings

Execution to be tracked in Cyber power did some review check from gamer friends of US who said it’s comparatively cheap and hence less performance but low or middle income house hold in US prefer the same buying the same from Costco

One thing to be kept in mind that there is still B2B market place model Just like Indiamart which is capitvely used and management have given their intention to expand it or spin it off

B2B startup generated around 400 crores of internal revenue (notional revenue) for Creative the same if valued at 2.5x will be 1000 crores and if not listed safely applying 50% DLOM it’ll still be worth 500 crores

So if you are valuing using Table above please include above 2 lines also

Disclaimer – Invested, Biased and Can sell anytime

Please do your own Due diligence