Considering cash on the book I think paytm is here to stay.

In most segments it might not be no-1 but comes to close 2nd or third.

(-disc I use it as an all in one app → from stock investing to booking irctc tickets, hotels etc.)

In a country like India network effect plays for more than one player.

I always thought that paytm bank business is somewhat hampering it to reach larger audience – reason for lagging behind in UPI.

It has a vertical integration in gateway.

I see it as a holding company with many underlying businesses.

If everything is great why would market give you any opportunity.

This is my thought process.

Disc – caught the falling knife. Let’s see what will happen.

Posts tagged Value Pickr

PayTM (One 97 Communications Ltd) (22-02-2024)

PayTM (One 97 Communications Ltd) (22-02-2024)

(post deleted by author)

Ranvir’s Portfolio (22-02-2024)

Kopran Ltd –

Q3 FY 24 results and concall highlights –

Company’s business verticals –

API’s – Company has a product portfolio of 26 successfully commercialised APIs

Major APIs / segments where company is present –

Atenolol ( anti-hypertensive ) – company is one of the leaders in this molecule

Sterile Carbapenems

Sterile and Non- Sterile Cephalosporins

Macrolides

Others

Formulations – Company is only into exports of fixed dose formulations

(tablets, capsules, powders and suspensions) –

Penicillin based FDFs

Macrolides

Anti Hypertensives

Cardiovascular

Others

9M FY 24 API wise sales –

Carbapenems – 107 cr

Macrolides – 32 cr

Sterile Cephalosporins – 15 cr

Anti-Hypertensives – 32 cr

Urology antibiotics – 27 cr

Neuromodulators – 14 cr

Others – rest of API sales

Out of these, export : domestic API sales breakdown- 97 cr : 140 cr

9M FY 24 Formulation sales breakup – country wise –

South Africa – 96 cr

Africa – 53 cr

SE Asia – 20 cr

UK – 14 cr

Others – rest of formulation sales

Q3 FY 24 financial outcomes –

Revenues – 161 vs 160 cr

EBITDA – 25 vs 14 cr (huge margin expansion)

PAT – 16 vs 7 cr

Net Debt / Equity @ 0.19 pc

Margin expansion due better product mix due introduction of new products, lower RM costs, cost control initiatives. Expecting margin expansion to sustain in coming Qtrs

Company intends to get into manufacturing of KSMs to achieve better backward integration and to lower import dependence

Also intend to improve their share of sales to regulated mkts by adhering to better compliance standards

Company has invested heavily in Capex in last few years ( aprox 100 cr ). Expect Capex intensity to reduce going forward

Expect company’s new API plant at Panoli to go live in Q1 FY 25

Wrt new products, company intends to focus on anti-diabetic and cardiology products – both for regulated and unregulated markets

Company is already into contract manufacturing of APIs. This segment should expand going fwd

Once company starts making KSMs, EBITDA margins should end up touching 20 pc !!!

Company looking to clock 25-30 pc CAGR for next 2-3 yrs !!! Initially, most of this growth will be driven by semi / unregulated Mkts before the growth in regulated Mkts pick up after 2-3 yrs

Seeing very good demand outlook for Carbapenems from Domestic, Africa and LATAM mkts

Aiming to hit 1000 cr topline in 3 yrs. Additional 200-300 cr shall come from the new Panoli site. Rest from the existing facilities

These days, LATAM mkts are tightening their regulatory requirements in a meaningful way

As company improves its backward integration, aims to improve GMs beyond 40 pc for APIs and 35-40 pc for formulations

Disc: hold a small tracking position, looking to add more, biased, not SEBI registered

Ranvir’s Portfolio (22-02-2024)

Kopran Ltd –

Q3 FY 24 results and concall highlights –

Company’s business verticals –

API’s – Company has a product portfolio of 26 successfully commercialised APIs

Major APIs / segments where company is present –

Atenolol ( anti-hypertensive ) – company is one of the leaders in this molecule

Sterile Carbapenems

Sterile and Non- Sterile Cephalosporins

Macrolides

Others

Formulations – Company is only into exports of fixed dose formulations

(tablets, capsules, powders and suspensions) –

Penicillin based FDFs

Macrolides

Anti Hypertensives

Cardiovascular

Others

9M FY 24 API wise sales –

Carbapenems – 107 cr

Macrolides – 32 cr

Sterile Cephalosporins – 15 cr

Anti-Hypertensives – 32 cr

Urology antibiotics – 27 cr

Neuromodulators – 14 cr

Others – rest of API sales

Out of these, export : domestic API sales breakdown- 97 cr : 140 cr

9M FY 24 Formulation sales breakup – country wise –

South Africa – 96 cr

Africa – 53 cr

SE Asia – 20 cr

UK – 14 cr

Others – rest of formulation sales

Q3 FY 24 financial outcomes –

Revenues – 161 vs 160 cr

EBITDA – 25 vs 14 cr (huge margin expansion)

PAT – 16 vs 7 cr

Net Debt / Equity @ 0.19 pc

Margin expansion due better product mix due introduction of new products, lower RM costs, cost control initiatives. Expecting margin expansion to sustain in coming Qtrs

Company intends to get into manufacturing of KSMs to achieve better backward integration and to lower import dependence

Also intend to improve their share of sales to regulated mkts by adhering to better compliance standards

Company has invested heavily in Capex in last few years ( aprox 100 cr ). Expect Capex intensity to reduce going forward

Expect company’s new API plant at Panoli to go live in Q1 FY 25

Wrt new products, company intends to focus on anti-diabetic and cardiology products – both for regulated and unregulated markets

Company is already into contract manufacturing of APIs. This segment should expand going fwd

Once company starts making KSMs, EBITDA margins should end up touching 20 pc !!!

Company looking to clock 25-30 pc CAGR for next 2-3 yrs !!! Initially, most of this growth will be driven by semi / unregulated Mkts before the growth in regulated Mkts pick up after 2-3 yrs

Seeing very good demand outlook for Carbapenems from Domestic, Africa and LATAM mkts

Aiming to hit 1000 cr topline in 3 yrs. Additional 200-300 cr shall come from the new Panoli site. Rest from the existing facilities

These days, LATAM mkts are tightening their regulatory requirements in a meaningful way

As company improves its backward integration, aims to improve GMs beyond 40 pc for APIs and 35-40 pc for formulations

Disc: hold a small tracking position, looking to add more, biased, not SEBI registered

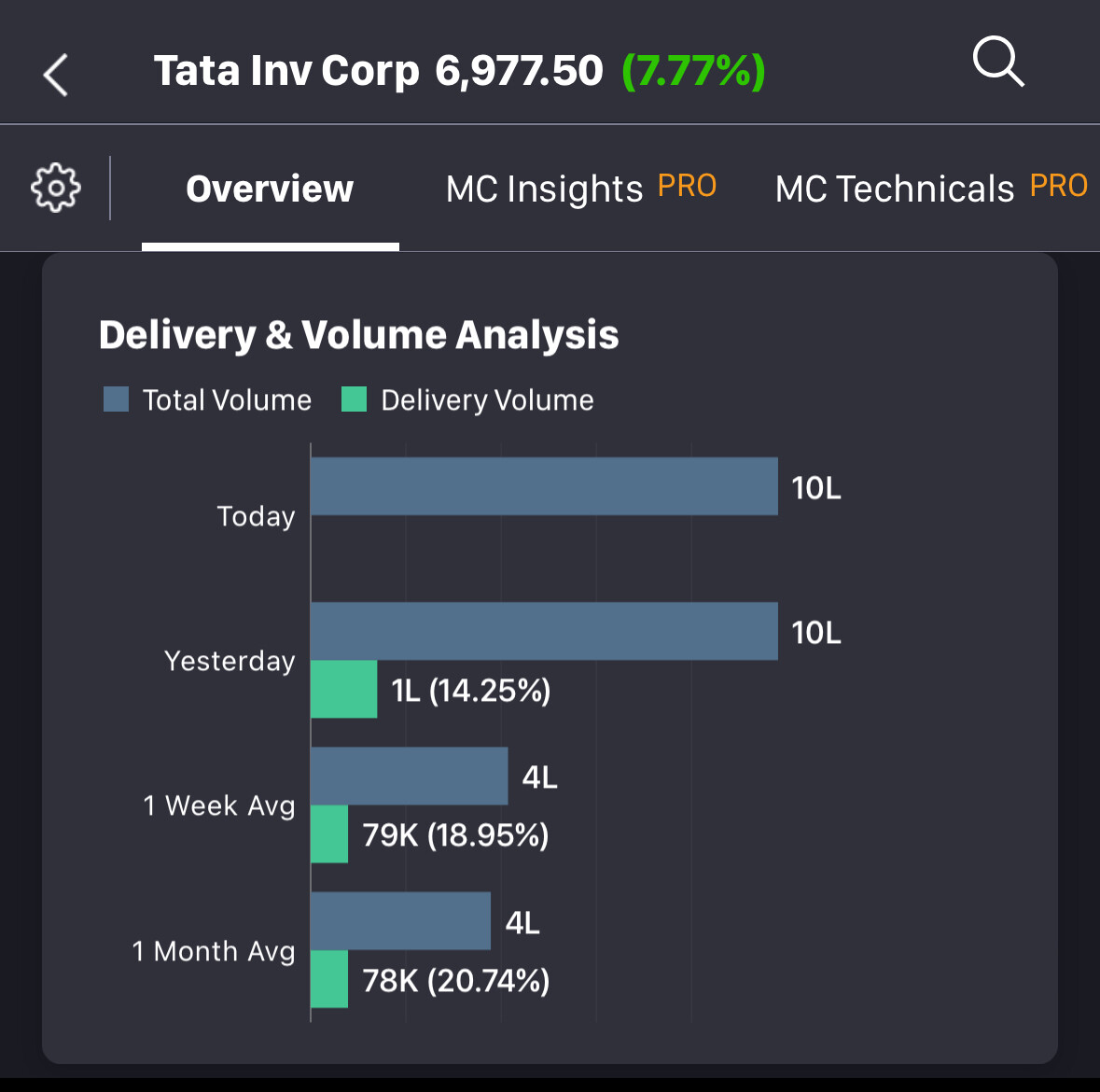

Tata Investment Corporation: Unusual discount to NAV (22-02-2024)

Considering such huge volumes and positive closing, something interesting is going on which we retail investors are ignorant about

Just a personal opinion

Tata Investment Corporation: Unusual discount to NAV (22-02-2024)

Considering such huge volumes and positive closing, something interesting is going on which we retail investors are ignorant about

Just a personal opinion

Fine Organics – Niche Player in Specialty Chemical (22-02-2024)

Nirmal_Bang_sees_38%_UPSIDE_in_Fine_Organic_Industries_Overseas.pdf (1001.4 KB)

please refer to attached Nirmal Bang report on Fine Organics

The management expects at least one quarter of pain in the US and

Europe markets due to subdued demand in the respective segment(s).

Considering the near-term demand outlook, we believe that capacity

shortage is not really very bad news. However, timely commissioning of

Maharashtra SEZ capacity is the key.

As far as expansion in

Maharashtra SEZ is concerned, the management expects final go-ahead for

land allotment in Mar’24. Post completion of EC, the new capacity spread over

30 acres can take 18-24 months for commissioning.

Target price of 6000, based on 40x PE on Dec’25 earning.

Fine Organics – Niche Player in Specialty Chemical (22-02-2024)

Nirmal_Bang_sees_38%_UPSIDE_in_Fine_Organic_Industries_Overseas.pdf (1001.4 KB)

please refer to attached Nirmal Bang report on Fine Organics

The management expects at least one quarter of pain in the US and

Europe markets due to subdued demand in the respective segment(s).

Considering the near-term demand outlook, we believe that capacity

shortage is not really very bad news. However, timely commissioning of

Maharashtra SEZ capacity is the key.

As far as expansion in

Maharashtra SEZ is concerned, the management expects final go-ahead for

land allotment in Mar’24. Post completion of EC, the new capacity spread over

30 acres can take 18-24 months for commissioning.

Target price of 6000, based on 40x PE on Dec’25 earning.

Shalimar Paints Ltd. — Worth a Serious Look — Significant Rerating Triggers Inplace (22-02-2024)

can be tracked

Whirlpool of India (22-02-2024)

it could be a good buy