thank you for the great review & summary.

Posts tagged Value Pickr

Skipper Ltd., (Power and Water) a moat in making? (22-02-2024)

Somehow I see my funds are still blocked by bank and no update on RE allocation.

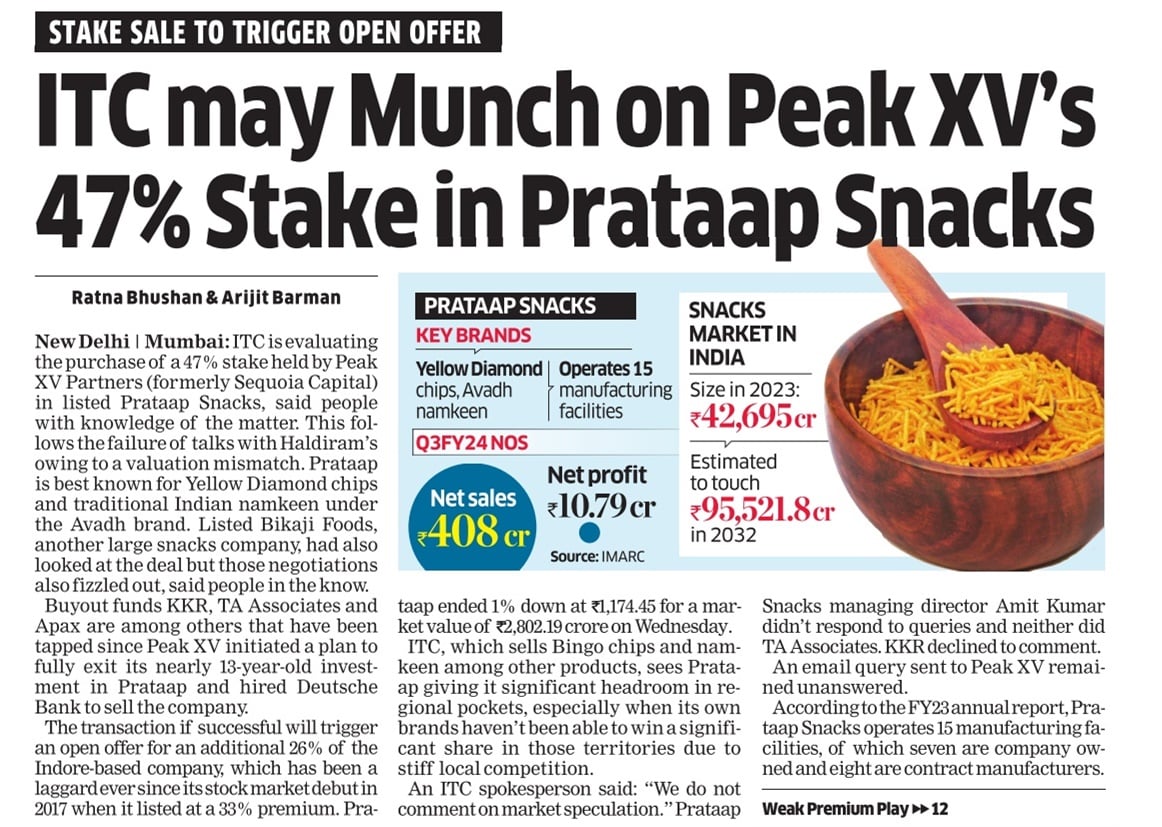

ITC: “Will”(s) “Gold Flake” assist “Ashirwad” to win “Bingo!”? (22-02-2024)

Chatters about buying Pratap Snacks.

Ujjivan Financial – Small Finance Bank (22-02-2024)

Since both the mgmt. are same this not a normal merger between 2 different set of promoters/ SHs running different business. This is a simple reverse merger with holdco. Mgmt. teams deliberate before taking such actions. There is no reason to cancel the merger.

SmallCap Hunter : Trying to find the dark horses with triggers (22-02-2024)

what is the CAGR or rolling return of small cap index against sensex for the same time duration?

Samhi Hotels – Turnaround with Tailwinds (22-02-2024)

To add to the Cons: Company is depreciating a lower percentage of assets. This is contributing to an increase in Net Profit

Ambika Cotton Mills (22-02-2024)

The reduce in Import duty would definitely be an improvement going forward , however considering they have a huge stock pile of old inventory on which they have already paid the duty this may be a bit counterintuitive. Their competitors will be producing with the lower cost raw material.

Welspun India – most vertically integrated textile co (22-02-2024)

What explains the valuation gap between Welspun & Trident? Both are close in terms of operations except that Trident is backward integrated into Yarn (which is at best 4-5% EBITDA business).

- Welspun’s EBITDA margin 15.5% vs 15.1% for Trident.

- Welspun has a higher B2C share vis-a-vis Trident which is more B2B

- Welspun has higher Bed Linen capacity vis-a-vis Trident and hence greater operating leverage in play

- Similar net debt levels (1540crs for Welspun vs 1450 for Trident). Infact, the debt ratios are better for Welspun due to higher absolute EBITDA (1114 crs for Welspun vs 766crs for Trident)

In terms of valuation

If anything its Trident that had an income tax raid recently. Can’t understand the gap.

What’s the logic?

Marksans Pharma- Can it be the next Pharma Biggie? (22-02-2024)

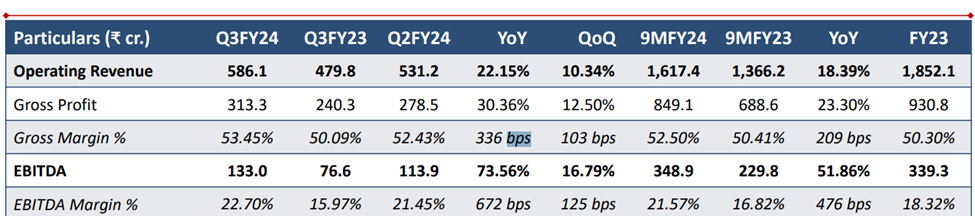

Highest ever quarterly sales at 586 crores.

US market grew by 16 % QoQ

Filed DMF for one products and planning to file another DMF for backward integration this quarter.

Cash balance at 688 crores

Consistent improvement in gross and EBITDA margins.

Teva facility is yet to break even. Operating leverage will kick in once sales increase at Teva facility. Expecting more contribution from Teva in Q4. The company seemed confident in future growth.

Expecting 600 crores sales from Teva facility in FY 25. Management sees a lot of prospects in US markets. Mentioned that they had just touched the tip of an iceberg. Sees a lot of prospects in the US market. Focussing on cough, allergy, digestive and cold OTC markets.

Spent 29.4 crores on R & D which is 1.8 % of sales.

Capex of 160 crores for the 9 months. Expecting a total capex of 250 – 300 crores over the next 2 years including the cost of acquisition of Teva. Nothing concrete on acquisition in Europe.

In US, the flu season starts in winter and a part of the QoQ growth could be attributed to this.