With 200klpd coming live in this quarter from mp and 250klpd coming live from Assam (April) will boost up top line and the recent increase in price by omc’s will start reflecting in bottom line from this quarter only… so we have to wait and watch atleast for next 5-6 months…

Posts tagged Value Pickr

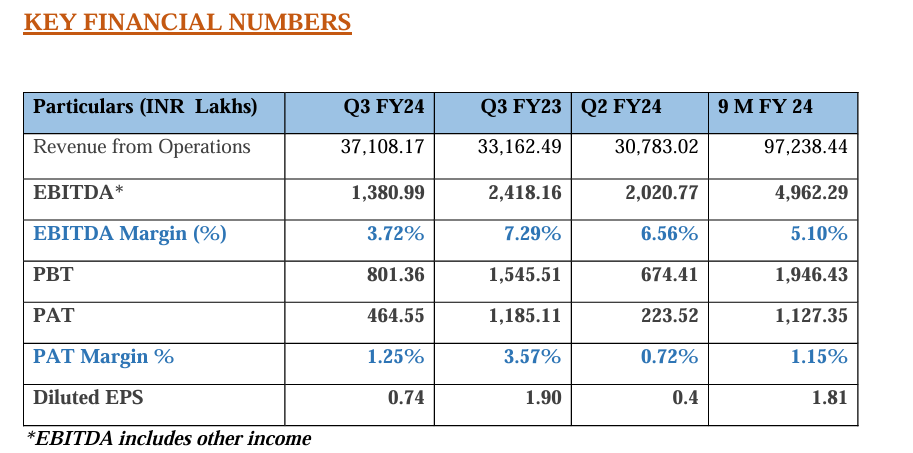

Gulshan Polyols(GPL) – Business by FMCG and Valuation by Commodity (19-02-2024)

Great work, fluctuating PAT margin, and EPS dilution, raises concern, your views.

Request for Information on Indian Companies Involved in Accounting Fraud (19-02-2024)

Just went through the video linked by @sudhakar_maradana which analyses Rajesh Exports. The analyst in the video never mentions Rajesh Exports as a fraud company nor does he strongly suggest any wrongdoing. He mostly gives his reasons for not investing in the company with a skin deep analysis of the last annual report. Does not even attempt to analyze the business model or the management quality in detail.

On a lighter note, definitely needs to add a few more colors in his presentation (he only catches the red flags at the moment).

Disc: invested.

Bajaj Finance Limited (19-02-2024)

We should learn to draw our lines somewhere. Yet we will always justify our holdings. That’s just innate human psychology.

Gulshan Polyols(GPL) – Business by FMCG and Valuation by Commodity (19-02-2024)

Q3FY24 could be the lowest ever margins in the companies history.

Even though margins are down, absolute number is increased as compared to Q2 due to incremental ethanol revenues.

Q4 can add 50-60 cr due to increase in capacity utilizations and increase in the ethanol selling price. PAT can double in Q4 as compared to Q3.

Balaxi Pharmaceuticals (19-02-2024)

Recently, huge (all-time high) volumes on this counter. Can’t find any bulk, or block trades either. Mixed Q3 FY24 results. Are the conditions in Angola getting better or something else?

Few developments:

- Raised capital through preferential allotment for capex – formulation plant. 32 Cr for phase-1 which will be completed in 1 year time. Funding secured for this.

- 15 Cr for phase-2 which will double phase-1 capacities. This will be secured by incremental preferential warrant issues.

- Incorporation of a step-down subsidiary in Chile and acquisition in Ecuador. Will help in expanding in South America.

Anyone tracking Balaxi Pharma?

Great Eastern Shipping (GE Shipping) – Possible Sleeper? (19-02-2024)

Consolidated NAV as mentioned in the Nov 2023 concall is Rs.1263 a share whilst standalone NAV/share > 1000. Current CMP is 925. Price to book value as per screener currently is 1.18 so the story does look interesting for sure.

Pricol limited – OEM automotive (19-02-2024)

Pricol limited Q3 FY24 concall notes:

Financials:

| Q3 FY24 | Q3 FY23 | YOY | Q2 FY24 | QOQ | 9M FY24 | 9M FY23 | YOY | |

|---|---|---|---|---|---|---|---|---|

| Revenue | 572.59 | 479.04 | 19.53% | 577.82 | -0.91% | 1687.62 | 1435.08 | 17.60% |

| EBITDA | 69.75 | 51.76 | 34.76% | 70.47 | -1.02% | 207.72 | 169.76 | 22.36% |

| EBITDA % | 12.18% | 10.80% | 12.74% | 12.20% | -0.12% | 12.31% | 11.83% | 4.05% |

| PAT | 34.02 | 26.76 | 27.13% | 33.15 | 2.62% | 99.11 | 94.88 | 4.46% |

| PAT % | 5.94% | 5.59% | 6.36% | 5.74% | 3.56% | 5.87% | 6.61% | -11.17% |

Revenue distribution:

- 70% from driver information systems and connected vehicle solutions(DISCVS). 30% from actuation, control and fluid management systems(ACFMS).

- With in DISCVS:

- Around 67% from two wheelers

- 15% from commercial vehicles

- 7-8% from passenger vehicles

- Remaining (~10%) tractors & off road vehicles

- 90% revenue comes from the domestic market & 10% from exports.

Product launches in Q3 fy24:

- Launched a number of products in the last quarter.

- Hero Xtreme 125 cc

- Hero Maverick 440cc

- Tata motors punch (EV & IC)

- Switch mobility (EV wing of Ashok Leyland, IeV3/V4 series)

- Daimler (Prime model)

New products/solutions being worked upon:

- Majority of these products are being worked upon(in development), some of them are in the proof of concept stage. Most of these products contribute to revenue from Q4 FY25. So significant upside can be seen in FY26 revenues and could be a contributor to the FY26 guidance of 3600 crores.

- E-cockpit with one of the major customer

- Battery management system

- Disc brakes

- SIBROS partnership.

- This is not exclusive to Pricol but the solution that Pricol is working upon is kind of exclusive and Sibros telematics in the cloud is one part of it. Pricol is working on an end to end solution and Sibros will be part of it.

- Oil & air pumps

- Launched with Tata motors and Ashok Leyland last quarter

- Telematics solution

Top customers:

- 2 wheeler:

- TVS, Hero, Bajaj, Royal Enfield, Honda & Suzuki

- Passenger vehicles:

- Tata motors, Ashok Leyland, Volvo & Eicher

- Off-road: JCB

Guidance

- Order book is looking healthy & very strong. Guidance of 3600 crores by FY26 is intact and depends on the customer launches & how market is going to be. As I mentioned above there are a number of products being worked up on which should cater to this guidance starting Q4 FY25.

- Company is also looking for inorganic growth in the non auto segment, nothing at the moment to speak of.

- Red sea impact: There is a couple of weeks of delay in shipping and the company has rerouted and now came to normalcy. Export is 10% of revenues, so not much of an impact.

Margins:

- EBITDA margins 9M FY24: 12.31% vs 11.83% same period last year

- Company guiding a 13.5% EBITDA margins and is expected to reach before FY26.

- There was a question on margins being affected when they enter into ore electronics, to which management answered that they are transitioning into a solutions company from a product company (providing end to end support). Company is working on the off the shelf component which customers can easily plugin.

- A similar question is being asked on E-cockpit solution where Visteon is a competitor, management agrees that there is competition and focuses on quality of the solution/innovation to win customers and penetrate. For e.g. they entered into passenger vehicles in 2020 and are doing quite well winning customers in the segment. They are doing good in the EV segment as well.

What’s Pricol moat?

- One of the questions was about Pricol’s moat in winning new customers/penetration in the market. Below is what management said:

- 4.5% of revenue spent on R&D for the last 5-7 years.

- In-house machine building (they do their own tools, own lines, own plastic injection molding & own PCB population)

- Exclusive tie up with many of the chip manufacturers & have long term contracts with them.

- A little bit of research is needed to see if these are really the moats and compare this with some of the best in the industry (say Sona comstar, UNO Minda etc.)

- Industry is moving from mechanical to digital to tft to high end digital information systems. This helps increase kit value and Pricol is innovating in this segment and in the sweet spot to capture the market.

Awards received in Q3fy24:

- Technology & Innovation award from Daimler trucks.

- Best quality performance from JCB

- Gold award from Tata motors.

Answers to “things to look for in the coming quarters from Q2 fy24” update:

- Improvement in EBITDA margins (they are a bit lower compared to last year numbers as against management commentary of this going up)

- 9M FY24 EBITDA increased by 48bps and 119bps short of guidance of 13.5%

- EV sales pick up in coming quarters

- There are some hiccups in EV sales this year but this should do very well starting next year. Management mentioned a number of products they are working upon for EVs.

- Minda corp stake increase related issues

- Minda corp fully sold its stake and this issue is gone now. They made a good profit though (but may have gotten a bad name?).

- An eye on the growth as this year it seems to be doing less than what is required to reach fy26 target.

- My guess is FY26 will be a good revenue generating year compared to FY25 as several new product launches are going to happen from Q4FY25.

Things to look for in the coming quarters:

- EBITDA margins : guidance of 13.5%

- EV sales pickup/penetration.

- Revenue target of 3600 crs by FY26.

- Inorganic growth by acquiring something from non-auto space (management mentioned about 4000 crs by FY26 out of which they expect 400 crores through inorganically).

Disclosure:

Invested and have been buying after Q2 results. Currently forms about 5.66% of the overall portfolio with average purchase price of 305.

Atirek portfolio (19-02-2024)

Thanks @hardik_shah1 for asking.

I am still not sure about the optimum percentage for the high conviction stock and I am still observing myself and learning.

All the comments below are based on my observations of my behaviours and I like experimenting.

I manage multiple portfolios – my sister, my mother, my father and mine.

I don’t remember putting more than 7 percentage at buy price of my net worth at any time in any of the stock in my portfolio. Reason behind not putting a lot of money in one stock is that I am not confident of my abilities.

With time I have started taking bigger position in stocks at my net worth level as I am learning with time.

I use SOIC allocation framework of 2-4-6-8 as the starting point for deciding allocation.

I don’t understand the companies in too much depth to take 8 percent allocation at the buy price of net worth. Though someday, I aspire to reach there.

Mostly I don’t hold the company with 2-3 percent allocation at buy price of my networth due to efforts invested in tracking and understanding the company. It either scales to 4-5 percent or I take the exit as my understanding improves.

The other reason is that I don’t get many stocks to invest.

I have 5 stocks in my Indian portfolio.

Other than 5 stocks, I also have 1 share of protean just to understand the business through the investor relations.

In my US portfolio, I have underperformed the US nasdaq 100 and due to tax complications, I am not looking forward to put more money in US stocks and hence not discussing about its allocation.

Not discussing the portfolio allocation of other members of my family due to privacy concerns.

Archean Chemical – Specialty Chemical Leader (19-02-2024)

Why promoters pledged 4.55% of its holding in Dec ’23 quarter? Any info?