Hey Apurva, where did you read about 25-30% growth for 3B Blackbio? They don’t do concalls so wondering about the source.

Posts tagged Value Pickr

Eicher Motors (19-02-2024)

@laxman_sreekumar these numbers will vary month to month. I think RE intentionally keeps shifting between motorcycles and between export and domestic. For each motorcycle, they figure out what the ideal waiting period is. They don’t want to make it too long that customers lose patience nor do they want to make it too short to maintain the perception of demand supply gap. We should look at quarters or yearly numbers only.

Pyramid Technoplast – Transforming Company (19-02-2024)

Detailed risk analysis is missing.

Sandeep Kamath Portfolio | Momentum Investing (19-02-2024)

What is the reason for MRPL entry?

HDFC Asset Management Company (19-02-2024)

To add:

Hdfc Amc also declares most of it’s profits as dividends which is a good thing. MF industry has a long way to go and probably why many new companies are entering. So, the question really is why should Hdfc Amc deserve a premium / high valuation. They already lost market share. Moved to 3rd position from being no. 1 till early 2020 in total AUM and I don’t see them catch up with SBI anytime soon in terms of AUM, however lesser profitable ETF AUM is for SBI

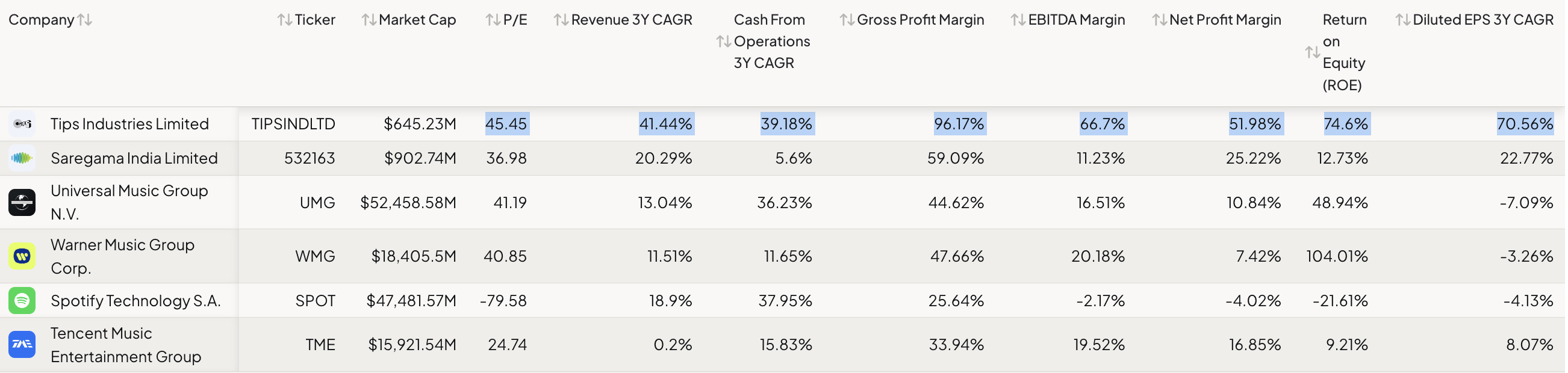

Tips Industries Limited – Ready to RACE ahead! (19-02-2024)

Did a quick survey of TIPS’ numbers and valuation w.r.t. global/domestic peers

While I have not done an in-depth study of its global peers, I am keen to do it now considering its growth has been feverish thus far and at the same time valuation has been stretching beyond its 3/5y median PE.

However, looking at the global/domestic peer set, valuation vis-a-vis growth over time is the best in class.

@ankush12495 Sorry to bother and I don’t know if you still hold but would love to hear your thoughts on the same. thanks in advance.

Disc: Invested from 2021 levels (position size here). No transactions in the last 30 days.

Senco Gold: Upcoming gold story! (19-02-2024)

Thank you so much, Sir, best of sharing your knowledge.

IRCTC: a necessity, a monopoly (19-02-2024)

Indian Railway Catering and Tourism Corporation Q3 FY24 Earnings Conference February 14, 2024

Catering segment:

The catering segment reported a 29.1% year-on-year growth in revenue, reaching Rs.507.76 crores and a 17.6% increase on a quarter-on-quarter basis.

It may also be noted that the Q3 and nine months’ revenue in FY’24 is the highest ever recorded in the catering segment. The EBITDA margin continued to show substantial improvement reaching 15.44% compared to 10.73% year-on-year. However, there was a slight decrease compared to the 17.21% quarter-on-quarter margin, mainly due to changes in the product mix within the catering vertical as the prepaid trains revenue having low EBITDA, has increased Q3 to Rs.59.76 crores from Q2 Rs.207 crores.

Internet Ticketing:

- This segment continues to demonstrate resilience amid the conversion of the reserve to tickets back to the early reserve tickets during the pre-pandemic period. The revenue for the quarter was Rs.335.31 crores growing by 11.4% year-on-year and 2.39% quarter-on-quarter. The EBITDA margin for the quarter came at 83.02% versus 83.7% quarter-on-quarter and 84.15% year-on-year.

Tourism and state distance:

- That segment saw strong growth in revenue for the quarter at Rs.195.47 crores, implying a growth of 32.28% year-on-year and 21.11% quarter-on-quarter. Given the revenue growth, the segment reported a positive EBITDA margin of 12.10% versus 3.6% on a quarter-on-quarter and 10.79% year-on-year basis.

Rail Neer:

- Q3 FY’24, reported a value of Rs.83.76 crores marking a sequential growth quarter-on-quarter of 7.39% and a year-on-year increase of 6.05%. The reported EBITDA margin stood at 13.43% representing an improvement compared to both the year-on-year figures of 11.20% and the quarter-on-quarter figure of 12.43%. However, the segment’s quarterly profit showed a negative return of minus 3.3 crores contrasting with the previous quarter’s profit of 8.8 crores. This decline was primarily attributed to an adjustment of an exceptional item amounting to Rs.14.51 crores in this quarter.

- For Q3 FY’24, the cash and bank balances and the net worth of the Company at the end of the quarter is Rs.2,258 crores and Rs.2,946 crores respectively

Bajaj Finance Limited (19-02-2024)

I am sure that in financial sector you have to do things which don’t look ethical.

Giving a personal loan at 24 perc+ interest is not ethical. Creating mounting pressure on an individual to repay a loan is not ethical, calling millions of people and convincing them to take a loan is not ethical. But doing all of this makes money.

Also, is giving loans at higher interest rate to needy people ethical? But will we ever invest in a company giving loans to needy people at 10 percent? We won’t be able to, such a company will not survive.

A finance company takes all opportunities available to it for growth, optimising its own risk reward ratio.

As a share holder you will like a company growing at 25 perc rather than an ethical company growing at 10 percent, sometimes going into losses so that it can give some leeway to people who might be facing difficulties repaying loans.

Pyramid Technoplast – Transforming Company (19-02-2024)

Industry Overview

The size of the global intermediate bulk container market, which was estimated to be worth USD 13.5 billion in 2021, is expected to increase from that amount to USD 14 billion in 2022 to USD 22 billion by 2030, growing at a CAGR of 5.5% over the forecast period (2023-2030).

The market for steel drums was valued at USD 11.53 billion in 2022 and is anticipated to grow to USD 18.87 billion by 2030. Steel drums, also referred to as steel barrels, are cylindrical steel storage and transportation containers that are frequently used for a variety of materials.

During the forecast period of 2023–2030, the global steel drum market is anticipated to expand yearly at a promising CAGR of about 5.75%.

The size of the global Plastic Drums market was estimated at USD 2757.95 million in 2022 and is projected to grow at a CAGR of 2.45% during the forecast period, reaching USD 3189.37 million by 2028. Industrial-grade plastic drums made of polyethylene or polypropylene are containers.

The current Indian industry size of plastic barrels is estimated to be around USD 13.13 billion in 2023. It is expected to grow at a CAGR of 9.36% from 2023 to 2028, reaching a value of USD 17.03 billion by 2028.

India’s MS-Drums market revenue is expected to grow at a CAGR of 9.14% from ₹ 280714.74 lakhs in FY22 to ₹ 517794.61 lakhs in FY30

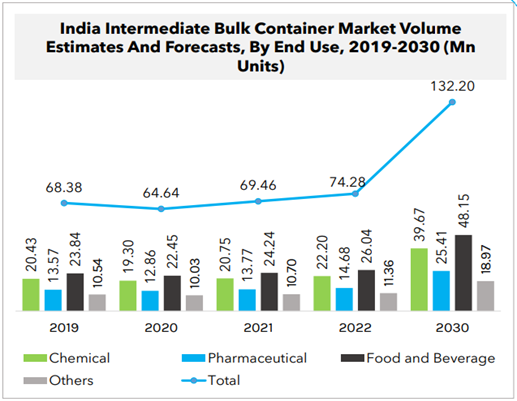

India’s Intermediate Bulk Container (IBC) market revenue is expected to grow at a CAGR of 10.56% from ₹ 4,001,261.80 lakhs in FY22 to ₹ 8,931,901.94 lakhs in FY30

India’s polymer drums market revenue is expected to grow at a CAGR of 9.87% from ₹ 127,584.77 lakhs in FY22 to ₹ 270,937.39 lakhs in FY30

Company Profile

Pyramid Technoplast Limited (PTL), which was founded on December 30, 1997, is a company that produces industrial packaging and specialises in the moulding of polymer-based products, especially Polymer Drums. These goods meet the packaging requirements of businesses involved in chemicals, agrochemicals, specialty chemicals, and pharmaceuticals.

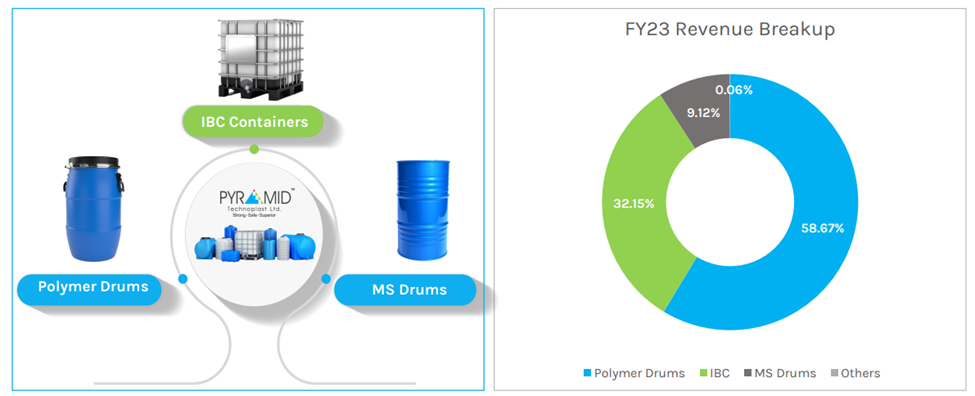

In India, the company is well-known for its production of rigid Intermediate Bulk Containers (IBCs), with a focus on IBCs with a 1,000-liter capacity.

Company also produces MS Drums, which are containers made of mild steel (MS) and designed for the secure transportation of chemicals, agrochemicals, and specialty chemicals.

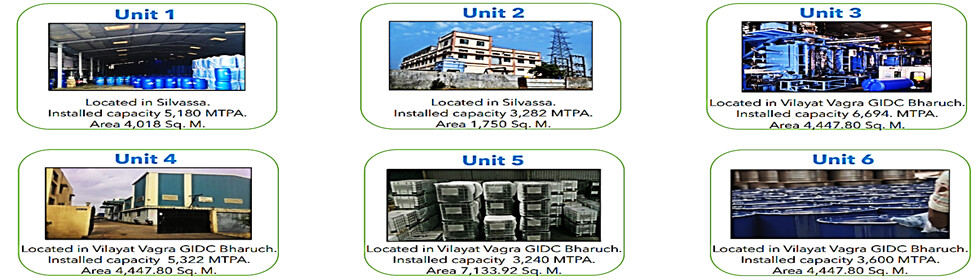

In 1998, the business commenced commercial production in Unit I. At the moment, it has six manufacturing facilities, of which two are in Silvassa and Nagar Haveli and two are located in Bharuch GIDC. Gujarat is building a seventh manufacturing facility next to the current one.

Pyramid operates across 7 manufacturing units with capacities of 22,818 MTPA for Polymer Drums, 420,000 Units of IBC, and 10,800 MTPA for MS Drums …

Why We Are Studying?

- Pyramid has a 40% market share in IBC in India

- Company Runing at 80% Capacity

- Deleveraging Balance Sheet

- Company Product Mix Shifting to Grow the Margin

- High Inventory Turnover Compared To Peers

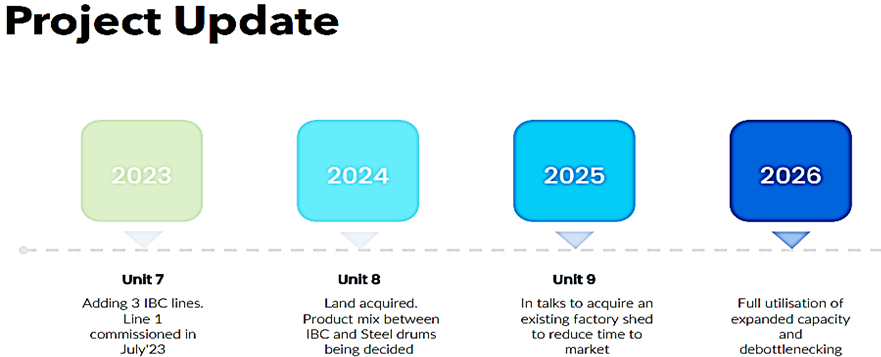

- Company Laid Out the Capex for Plant 8 & 9 To Grow Further

- Company in Next 3 Years Plan to Double the Revenue

Business Model

Manufacturing Process

Polymer drums and IBCs are produced by the company using blow moulding technology. Caps, closures, bungs, lids, handles, lugs, and other internal components are produced using injection moulding technology. Pyramid is the brand name used for marketing and sales of its goods.

Manufacturing Unit

With an industry-leading asset turnover of about 5x, all plants are running at between 75% and 80% of their potential.

Product Portfolio

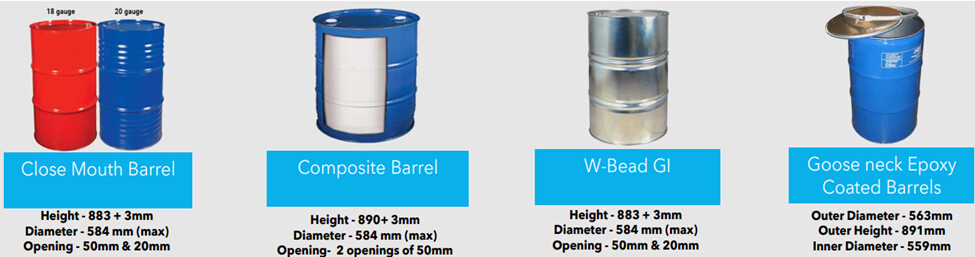

IBC Containers:

Plastic Barrels:

MS Drums:

Clientele

Asian Paints, Adani Wilmar, Patanjali, JSW, Deepak Nitrate, Unites Phosphorous, GACL , etc. are the key client of the company. In the most recent fiscal year, they provided services to about 376 clients.

Revenue Split

Competitive Strength

- The company provides Polymer Drums, IBCs, and MS drums to meet the bulk packaging needs of its customers from a variety of industries, including chemicals, agrochemicals, pharmaceuticals, lubricants, and edible oil.

- The business has developed relationships with numerous clients in these industries over the years and has continued to provide them with its product offerings. During the last three financial years, the company regularly served more than 376 customers.

- In order to transport dangerous goods safely (by road, rail, sea, and air), the company has obtained UN certification for IBC and MS Drums.

- 75%-80% Business Recurring

- Import of IBC is Not Possible as the transportation cost is higher

- Pyramid has a 40% market share in India , and the company is concentrating on value-added products like IBC by expanding existing facilities.

- The development of the Indian paint and chemical industries is anticipated to be favourable for the IBC segment. The company has no seasonality, and revenue is distributed fairly throughout the year.

Future Outlook

- Chemical sector demand has picked up in Q2. Volume outlook strong.

- For proposed Unit 8 and Unit 9, the capex budget is between Rs. 40 and 50 crores (FY24–FY26). There will be a five-fold asset turnover. Plans and configuration for Unit 8’s Capex are being considered. Unit 9 is considering a number of locations.

- For the IBC plant, the company recently put Line 1 into service. The company’s main goal is to make metal drums more automated.

- Within three years, the company hopes to have doubled its revenue. A 25% return on equity is what the company wants to keep maintaining. A focus is being placed on growing the IBC segment’s market share

- Expecting that in the next three years our revenue will come from 40% IBC, 50% from plastic drum and 10% from metal drum

- The development of the Indian paint and chemical industries is anticipated to be favourable for the IBC segment.The company has no seasonality, and revenue is distributed fairly throughout the year.

Disc : For Learning No Buy Sell Rico****