kindly suggest some books to learn sector analysis ?

Posts tagged Value Pickr

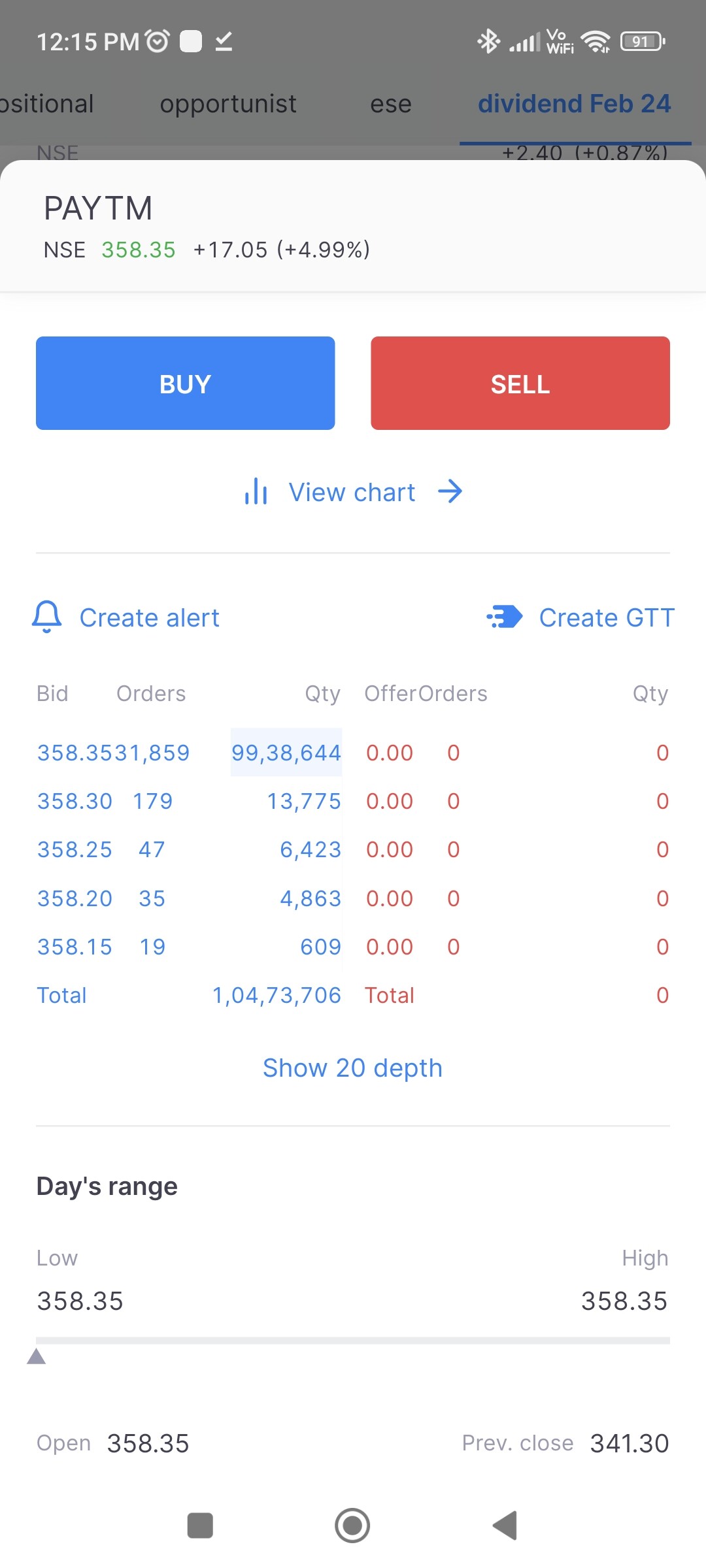

PayTM (One 97 Communications Ltd) (19-02-2024)

Look at the qty ? Does it mean someone trying to buy big ? Almost 350cr value order. Can somebody explain?

Divi’s Laboratories (19-02-2024)

Divi’s Laboratories Limited Q3 FY24 Earnings Conference Call February 10, 2024

Generic business segment:

We expect the products with recent regulatory filings to fuel our growth beyond the Financial Year 2025

The custom synthesis segment is on the rise, particularly with the 2 major projects from the big pharma entering into full-scale production where we expect their contribution to increase further in the coming quarters.

We have several molecules at various regulatory stages for our customers. With the expanded production capacity for both large and small-volume products, we are ready for new opportunities.

We are actively involved in the peptide building blocks used in the new anti-diabetic and anti-obesity drugs and are strategically focused on developing this specialized portfolio.

On the CAPEX front:

- Our forward momentum continues with unit 3 infrastructural establishments. The production activity in the 200-acre phase I greenfield project will commence in Q2 of 2024-25.

- Exports for the quarter continued to be around 87%. Exports to Europe and America are about 71% for the quarter. The product mix for generics to custom synthesis is 54% and 46% for the quarter.

Vaibhav Global ~ Vertically integrated value e-tailer of Jewellery and Lifestyle Products (19-02-2024)

earlier management has said that due to such economic situation, people tend to move from brands to low cost value provider like Vaibhav.

Great articles to read on the web (19-02-2024)

Have been reading this over the weekend. A lot of the thought process is completely opposite of how we retailers react and read.

A guide to navigating quarterly noise-flow (substack.com)

Pointing out couple of core paras rather than making my points, Below is taken verbatim from the essay.

View each quarter as one more datapoint in a continuing trajectory, not in isolation.

“”Answer starts with making such pictures, so as to internalise inherent lumpiness of long-run trajectories of good businesses. And then incorporate the same into short-run expectations. Use business history, rather than strangers’ estimates, as our guide to analysis of quarterly financials. Realize that that even the act of producing precise quarterly estimates is as arrogant as it is futile. Over the long run, good business invariably do fine, while following a path that is assuredly and extremely volatile. To borrow Pulak’s quote, “Nothing goes up in a straight line”.

Since all trajectories are bumpy, keep wide bands.

Awareness of long-run trajectory makes a compelling case for banning ‘basis points’ as unit of financial analysis. Plus or minus 25% swings in typically tracked metrics (revenue growth, EBITDA margin %) are a feature not a bug. For a company with 15% long-run average margin, a 12% or 18% quarter is normal, not exceptional. Ditto for revenue growth or working capital intensity. Explanations for deviations sound plausible but are actually made-up, usually to fob off pesky questioners on conference calls.

Approach financial results with wide error bands around a general long-term trend. Swings within this band generally merit a shrug of the shoulders, not activation of neurons.

Focus on controllables: relative over absolute performance, balance sheet over P&L.

Companies have little control over the metrics we obsess over – revenue and profit growth – at least over the short run. These are determined by industry growth, stage of business cycle, commodity inflation, exchange rates and base-period. Often, these effects are extreme.

The HS Portfolio (19-02-2024)

Have been reading this over the weekend. A lot of the thought process is completely opposite of how we retailers react and read.

A guide to navigating quarterly noise-flow (substack.com)

Pointing out couple of core paras rather than making my points, Below is taken verbatim from the essay.

View each quarter as one more datapoint in a continuing trajectory, not in isolation.

“”Answer starts with making such pictures, so as to internalise inherent lumpiness of long-run trajectories of good businesses. And then incorporate the same into short-run expectations. Use business history, rather than strangers’ estimates, as our guide to analysis of quarterly financials. Realize that that even the act of producing precise quarterly estimates is as arrogant as it is futile. Over the long run, good business invariably do fine, while following a path that is assuredly and extremely volatile. To borrow Pulak’s quote, “Nothing goes up in a straight line”.

Since all trajectories are bumpy, keep wide bands.

Awareness of long-run trajectory makes a compelling case for banning ‘basis points’ as unit of financial analysis. Plus or minus 25% swings in typically tracked metrics (revenue growth, EBITDA margin %) are a feature not a bug. For a company with 15% long-run average margin, a 12% or 18% quarter is normal, not exceptional. Ditto for revenue growth or working capital intensity. Explanations for deviations sound plausible but are actually made-up, usually to fob off pesky questioners on conference calls.

Approach financial results with wide error bands around a general long-term trend. Swings within this band generally merit a shrug of the shoulders, not activation of neurons.

Focus on controllables: relative over absolute performance, balance sheet over P&L.

Companies have little control over the metrics we obsess over – revenue and profit growth – at least over the short run. These are determined by industry growth, stage of business cycle, commodity inflation, exchange rates and base-period. Often, these effects are extreme.

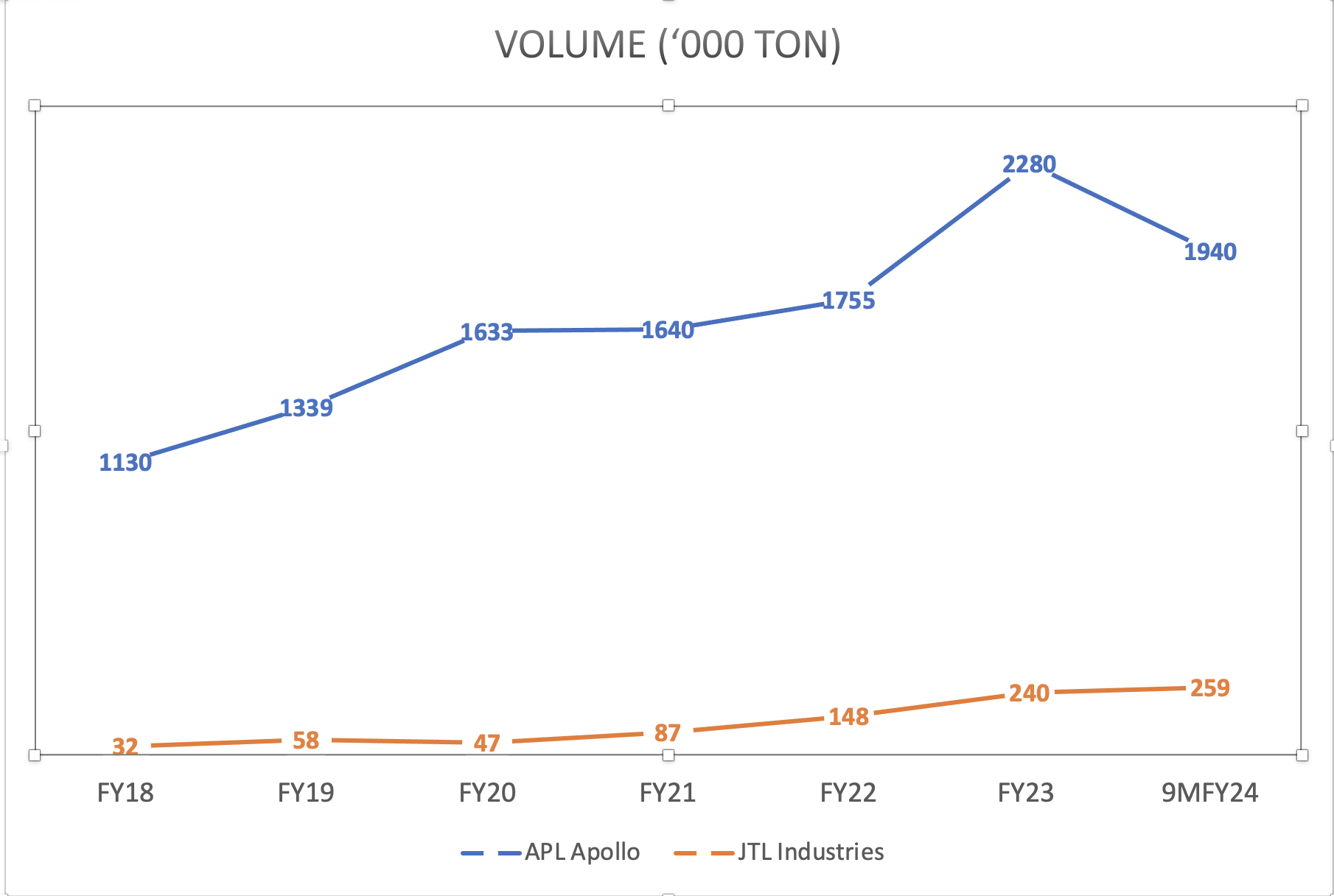

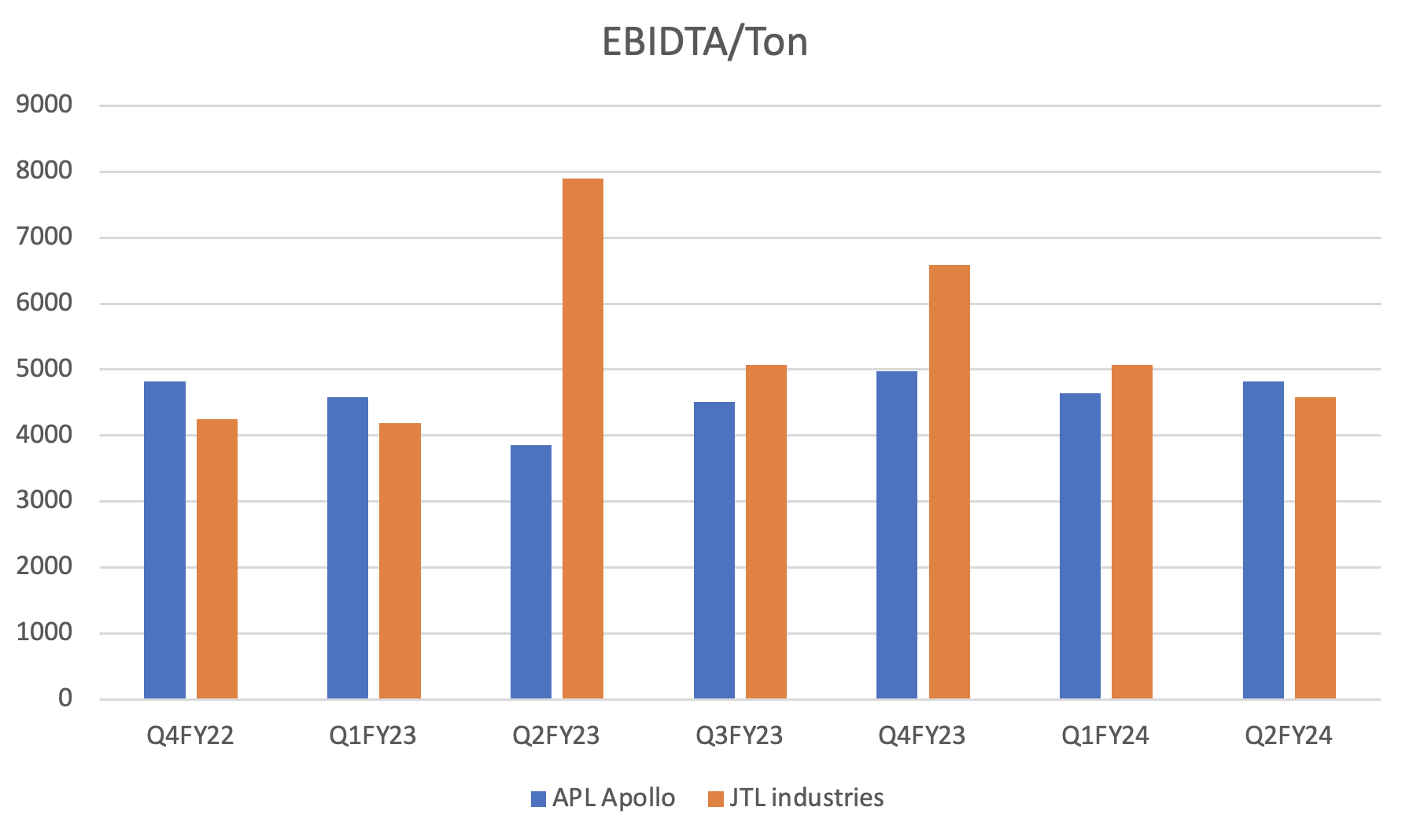

JTL Industries – Fast Grower at an inflexion point (19-02-2024)

I have done some comparison with APL Apollo for volume growth and EBIDTA/ton.

Pace of growth has been phenomenal while maintaining EBIDTA levels.

Atirek portfolio (19-02-2024)

I like the thought process. What do you think would be optimum percentage you would allot in the PF for a high conviction stock. And do you have a plan as to how much a median stock gets alloted in the PF.

Sula vineyards – pioneers in indian wines (19-02-2024)

No doubt that this is peak valuation if we go by sales figures, growth % and tax subsidy.

But wines seem to be on a long term track of adoption. I have heard many a times that India is not a wine country but things always change. With more women coming in work force (easy access to money), nuclear families (easy to keep wines on shelf at home), people becoming health conscious (even if its a perception that wine is healthy), sula vineyard becoming tourist hotspot and lot more wines on OTT & movies – wine has just one way to go as far as adoption is concerned. Sula being market leader should also gain sales / profitability.

It seems to be a multi decadal opportunity, hence invested from 3xx levels.