So you know if the company is the company hedging the risks of corn and soya price increases

Building a feed processing plant is counter intuitive if the price rise comes from soya price increase. It could hv probably applied that capital towards hedging instead of diversifying into parallel industries

I assume if company is supplying to the likes of McDonald’s they have a guaranteed volume at a certain price per kg.

This could be a huge risk in the short term due to inflation and investors don’t like choppy margins

Posts tagged Value Pickr

Venky’s India – Leader in Chicken and Eggs (18-02-2024)

Windlas Biotech – Pure play CDMO currently at ~1.1x sales (18-02-2024)

Its not 600-750 cr per quarter it is 700-750 per year as against current TTM revenue of 600 cr.

Your statement indicates a 4-5 fold increase in revenue which is not the case.

Please see the concall extract below.

Komal Gupta: Yes, so, Nitin, as I mentioned, the current capacities we had increased and we have been

consistently working on. So we are comfortable delivering INR700 crores to INR750 crores with

some incremental expansion internally that we have been working on. We have been adding it

as needed. So we are able to do that. So we should be able to deliver INR700 crores to INR750

with that. And there is other work going on for further runway…

disc.: not invested. tracking

Rohit’s Portfolio : Requesting Feedback (18-02-2024)

Trying to follow this thumb rule of investing when taking up initial positions (inspired by SOIC):

1% – Tracking

2% – Low conviction/exploring thesis

4% – Medium conviction and results show thesis has started playing out (e.g., Aarti industries)

6%/8% – High conviction with thesis getting validated

No position >8% due to concentration risk (Learned this the hard way after Polycab fiasco)

Obviously these are very different from what you see above because the total portfolio value keeps changing but on a high-level

Tracxn Technologies (18-02-2024)

Can anyone help me understand what could be the reason for slower growth in customer addition than the competitors? Ideally for a company with such a base should show higher growth? Are they lacking in the value provided to the customer?

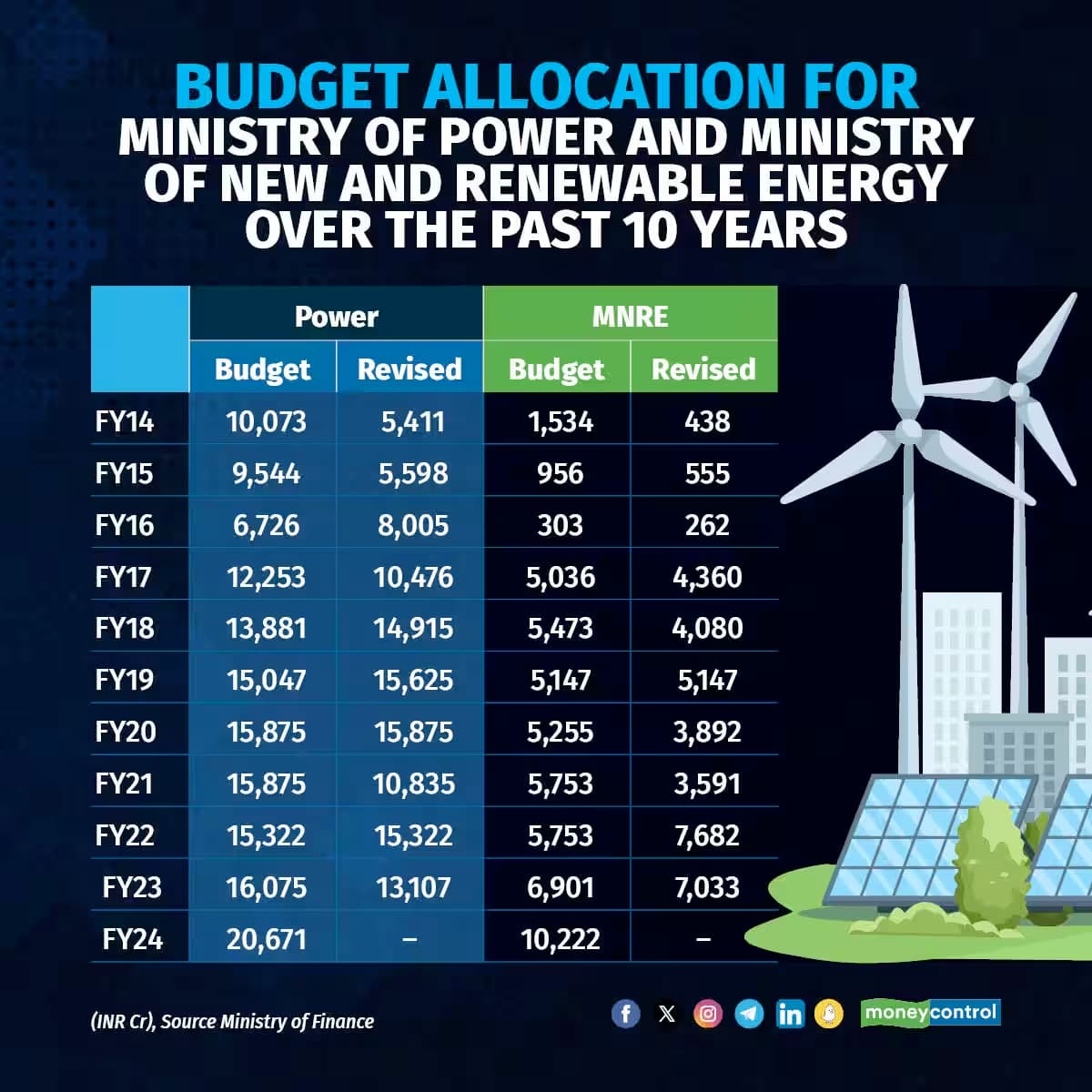

NTPC – Thermal Power (18-02-2024)

To meet the growing demand, the government has announced to continue relying on coal with nearly 80 GW of new coal-fired capacity planned by 2030

Scaling up renewable energy: The allocation to the new and renewable energy sector increased 99 percent to Rs 10,222 crore in 2023 from Rs 956 crore in 2014-15. Between 2013-14 and now, India’s installed pure renewable energy capacity (excluding hydropower) has almost quadrupled to reach 132 GW from 28 GW in 2013-14.

National Green Hydrogen Mission (NGHM): Since renewable energy alone would not be enough to meet India’s energy needs, the central government has attempted to get into new energy sources such as green hydrogen. The Union Cabinet approved the NGHM on January 4, 2023, with an initial outlay of Rs 19,744 crore, including Rs 17,490 crore for incentives. The government’s aim to produce at least 5 MMT of green hydrogen annually by 2030 under the NGHM would require 60-100 GW electrolyser capacity and 125 GW renewable energy.

India’s power sector is regulated by the CERC with an availability-based earnings model (fixed RoE on power generation assets) and, thus, the regulated tariff model provides strong earnings visibility for power-generation companies.

Additionally, with improved coal stocks at thermal power plants, plant availability factor (PAF) has improved and, thus, we expect fixed cost under-recoveries to decline for power companies.

NTPC

- Healthy expansion plans with significant capacities under construction

- NTPC has also entered into a JV for nuclear power generation.

- The PLF of NTPC’s coal stations was 76.40% as against the national average of 68.51%.

- MoU with the Maharashtra government for green hydrogen projects

- NGEL plans for green hydrogen and derivatives (green ammonia, green methanol)

- With renewed focus on RE (130 GW by FY32), we believe re-rating drivers like improving ESG scores

Quick notes on some terms:

PLF – Plant load factors (PLFs)

A cost-plus basis is a way of charging for a product or service where the price includes the cost of production or service plus a profit

Indiabulls Housing – A compounder from here? (18-02-2024)

Overtly optimistic. The truth is that most of their loans are stuck. They are not able to raise money easily!! They issued ncds many times. At the interest rate of 10.75 percent and yet they barely get subscribed to the minimum. They try to raise for 1k cr and it barely gets subscribed 110-120 cr!! The issue cost takes the effective interest rate for money raise to 12.5-13 percent!!

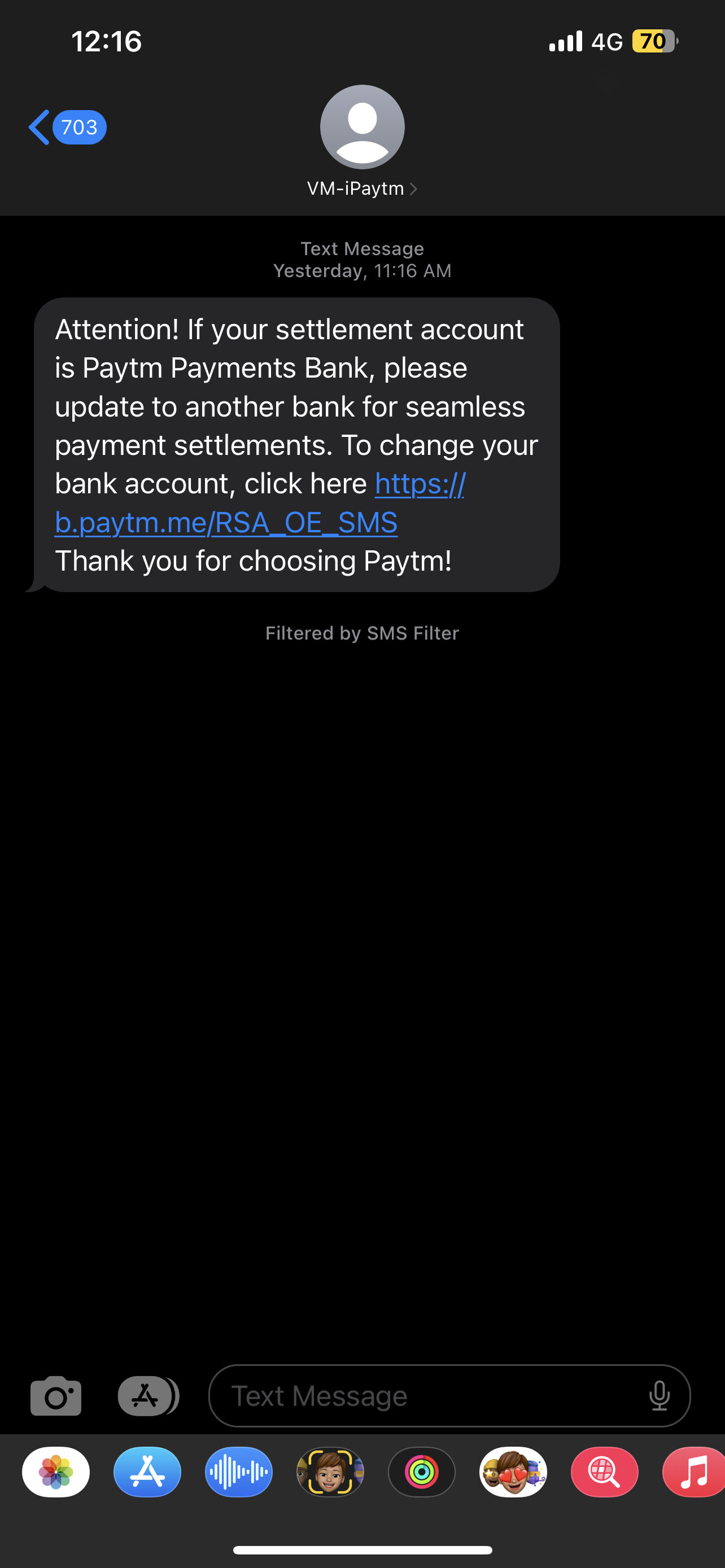

PayTM (One 97 Communications Ltd) (18-02-2024)

Please look at the below screenshot

OCL is reaching out to all their merchants and asking them to change their settlement bank account from PPBL to something else. Please note that KYC for these merchants in order to accept payments was done by OCL and not the Paytm Payments Bank. So all these merchants still continue to be eligible to accept digital payments through a QR code or soundbox.

Once merchants change their settlement bank account (this can be done easily without a physical visit), merchant’s life will carry on as is.

Rohit’s Portfolio : Requesting Feedback (18-02-2024)

Hi Rohit,

Great set of stocks!

Two points if you have please suggest your thought process about –

- Prakash – If you can share your hypothesis for taking exposure to Prakash

- Globus – How the hypothesis in this got broken

Thanks

-Manohar

Avantel Limited – Views please (18-02-2024)

Hi All,

I am a beginner in the forum and also in investing. Just want to run through my understanding for this stock. Opinions on what have not been considered and should be evaluated before buying this stock is welcome.

I generally evaluate a stock for the following:

- Market w.r.t demand or supported by government policies

- ROCE – growing/stable in last 3/5 years

- Operating Margins – Growing/stable in last 5-8 quarters

Basis the above criteria, this company seems to be good investment. Want to get views for the following:

- The PE is high which is at 51.50

- Since the margins have shown a growth trajectory for quite few quarters, is it fair to assume that the market has already absorbed this in the current price?

I want to invest in this company for 2 quarters to 1 year.

TAAL Enterprise – cheap valueations (18-02-2024)

some children flourish when away from parents.

In detail, Taal Ent had two business, air flight charter (not so good due to multiple factors, and having only 1 Cessna plane), and a Technology Engg Service subsidiary. The Air flight charter business was closed after accident to the plane, and now the Engg Service subsidiary is being merged with Taal Ent. This Engg Service Tech business has grown quite well, and is the main reason. Earlier this was very small (hardly 12 Cr/qtr) and now over the years it had grown to nearly 45Cr/qtr. Employee strength has grown from 100 odd to 690 in FY’23.