Posts tagged Value Pickr

Senco Gold: Upcoming gold story! (17-02-2024)

Stud is short of studded jewelry (i.e. fixed into the gold) which includes diamond and precious stone jewelry. The margin is higher is higher in it versus pure gold jewelry. Ratio of stud to gold jewelry is known as stud ratio.

Shankara Build Pro – Building Materials Organised Retail (17-02-2024)

They already have enough working capital. They don’t use it as fund based working capital, which is why you see low working capital in their balance sheet

Fairchem Organics – Previously “Adi Finechem” (17-02-2024)

Fairchem came out with a decent set of results, with sales growing by 45% and margins reviving to 13%. Management is very bullish on quick scaleup in isostearic acid which seems to be the near term growth driver, along with continued margin revival. Concall notes below.

FY24Q3

-

Sales volume increased by 2.64% and value decreased by 2.8% quarter-to-quarter

-

Process quantity was 15,277 MT (4.9% lower on Q-o-Q). 15% higher on 9MFY24 vs 9MFY23

-

Q3 Dimer acid: 2,000 tons, linoleic acid: 7,000 tons

-

9M Dimer acid: 6,000 tons, linoleic acid: 22,000 tons

-

Isostearic acid :

-

10 MT export shipment to EU in December, revenues not booked as they book revenue once customer receives shipment (CIF basis)

-

Overall capacity of 2000 MT and hope to reach full utilization in December 2024

-

Croda, Arizona have higher capacities

-

Will allow them to better compete with Chinese on dimer acid as isostearic acid scales

-

Differentiated product, required 5-6 years of development to manufacture because technology is not available off the shelf

-

-

Export : 10% of sales in Q3. Will not face delay due to Red sea crisis for US exports

-

Linoleic acid : China doesn’t compete because of high freight component

-

Overall capacity: 120,000 MTPA. 80,000 MTPA dedicated towards current products including isostearic acid and 40,000 MTPA are earmarked for new projects. Have adjoining land for expansion if required

-

Growth focus will not shift towards introducing higher value items than just processing more input material

Disclosure: Invested (position size here, bought shares in last-30 days)

Indian Defense Sector (17-02-2024)

defence-psu-midhani-enters-the-global-supply-chain-for-aero-engine-critical-materials

Senco Gold: Upcoming gold story! (17-02-2024)

Stud are jewellery which are kind of fast fashion and light in size like light earrings.

Studs generally has higher margin.

Shankara Build Pro – Building Materials Organised Retail (17-02-2024)

As per this data,stores are on rent and leases.i think this is due to pursuance of asset light model

KDDL (Ethos Watches) – Scalable business model at an inflection point? (17-02-2024)

Ethos Limited Q3FY24 concall summary, please add your thoughts or any corrections

Key Financial Highlights – Q3 FY24

● Revenue of Rs. 281.2 crore with 22.4% YoY growth

● EBITDA of Rs. 50.8 crore with EBITDA margin of 17.7%

● PAT grows to Rs. 25.5 crores in Q3FY24 vs Rs. 20.7 crore in Q3FY23

● Strong revenue growth across offline and online channels

● A higher share of in-house brand sales continues to aid margin expansion

- Potential benefits from an India-Swiss FTA could aid Ethos in saving currency rate costs, targeting 13-14% SSG for the decade, and 46% repeat customers. RIMOWA store profitable from the 1st month, CPO rev 49cr for 9mFY24

-

Planning to launch Favre leuba globally by Aug24 at a watch event.

-

Guidance of 25% rev growth for decade, aims to be top 3 retailer by this decade and currently has 20% market share in luxury watch segment.

-

Plans to open 15-20 new stores in FY26, with 25 planned for FY25; still in the testing phase for jewelry; considering adding a maximum of 2 more boutique luggage stores in the next 12-15 months.

-

Opened 1 new store in Q3, unaffected by inflation, and witnessed bumper earnings from the stock market.

-

Exclusive brand contracts range from 5-9 years, with marketing costs shared, aiming for >40% market share by the decade.

-

Payback period for stores is 3 years, with a CAPEX and WCInv of 7.5Cr per store (same guided in last call).

-

Margin expansion strategies include leveraging operating leverage, normalizing CHF/INR rates, and increasing EB watch sales.

-

CPO growth is gradual, focusing on building relationships; RF Brands (which ethos incorporated it this month Feb24) will distribute watches below 1 lac price point to retailers (expect high sales but lower margins going ahead on a consolidated basis).

-

Previously were not focusing on >1 lac watches but the watch brands find them as preferred brand to distribute their watches, therefore incorporated RF brand where they will act as a distributor to distribute to other retailers in the >1 lac price point watches, RF brand will hold inventory of 2 months, sale to be on hand and inventory risk to be brone by the retailer means planning no credit sales . Therefore high sales but expect less margin.

-

Hiring 6 people per store for FY25 (as they planned 25 stores for FY25), with 60 people hired this fiscal year, therefore expect the employee cost to be high for Q3 and Q4 of FY24.

-

Favre Leuba targets 100,000 volume sales at CHF 2500 ex-factory price in FY25-26, aiming for higher margins.

-

Top cities: Delhi with 9 stores, Mumbai with 10 stores.

-

No issues with watch shipment due to the Red Sea situation.

-

Focus on expanding watch and store offerings; facing challenges in hiring skilled watchmakers for CPO therefore not focusing much on it.

-

Their framework is to maintained long term relationships with brands; they have 60 brands as of now which have been for a long time in the middle just signed out 7 brands.

-

The CPO business is usually 35% of luxury watch retailers, refer Ahmed Seddiqui for Middle east and Hourglass for South East Asia which had first mover advantage in their region for luxury watches, study their case studies for more idea on how ethos can move ahead.

Senco Gold: Upcoming gold story! (17-02-2024)

meaning of Stud ratio plz explean

Star Health & Allied Insurance Company – Leader In Retail Health (17-02-2024)

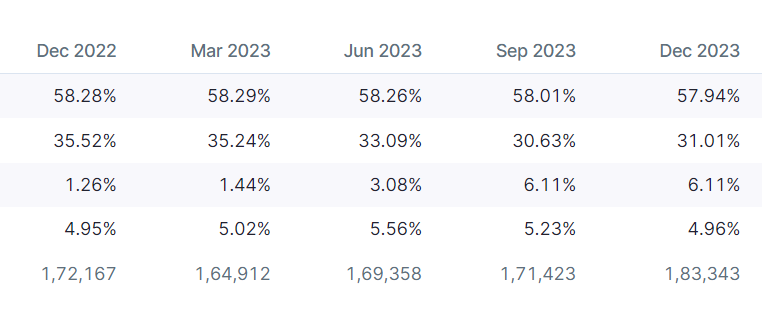

FII’s have been reducing their stake till last quarter. In the latest quarter, they have increased their stake.

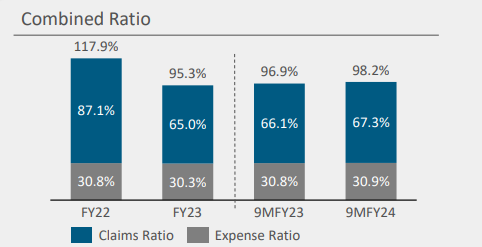

As per the latest financial report, Combined ratio of the company is increasing which is concerning.

PAT is increasing at modest rate.

Lower than expected growth and higher than expected combined ratio could be the reason for the downfall and sideways trend.

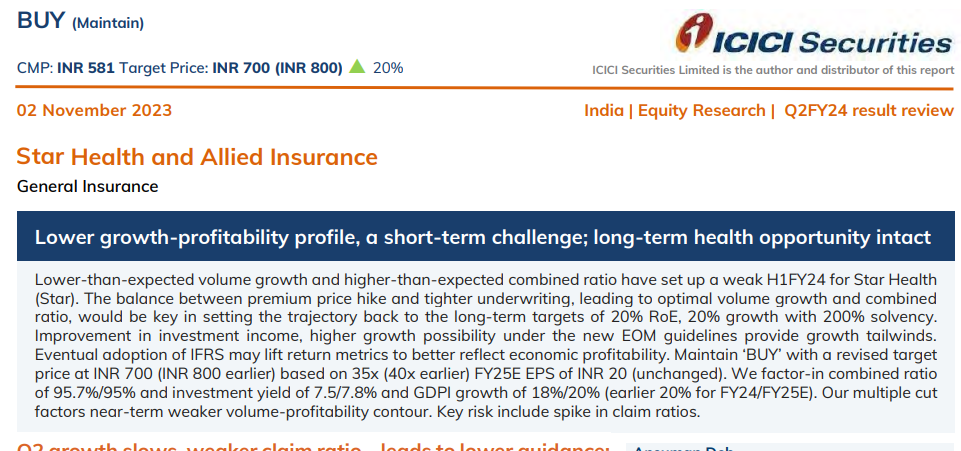

Source: HSIE results daily