Indirect Real-Estate Play

Following are the small and micro-cap companies, which are indirect real estate companies with deep valuations:

- Elpro

- Elnet

- Alembic Ltd

- Raymond

- Nirlon

- NESCO

- Century Textiles

- Accel Ltd

- Texmaco Infra

Indirect Real-Estate Play

Following are the small and micro-cap companies, which are indirect real estate companies with deep valuations:

Moreover, Pakka has an ‘Ayodhya advantage’. Pakka doesn’t sell paper like Satia does and hence deserves FMCG-like valuations.

The big problem with satia is that there is no growth plans as such. There plans to set up cutlery division has not really materialised as they had thought. For FY25 they don’t have any major capex just targeting 5-10% volume growth. The main difference between this and Pakka is that atleast Pakka has some growth triggers with new innovative products (even though that division has not really performed).

Here is one video that impressed me

Satia Industries partners with Schneider Electric to build “Automation of the future”.

Personally, I’m not looking to add to my holdings here. I’ve added Tata Elxsi at various points between the years 2016 & 2020. The valuations today are too rich for me to add more for a company poised to grow its topline by ~15-20% in the medium term and with no margin expansion. Though, I’m very comfortable holding the stock as the company has great prospects.

@Rafi_Syed what’s the source of this information?

Many thanks

As a general comment – where ‘you’ would mean ‘reader’

Perform a thought experiment :

What would you do at the black arrow? Imagine the current time was that time! Will you get out? Will you stay? If it is almost double then, at the black arrow, how confident are you based on the statement ‘bse small cap corrected to the level of nifty 50’ ![]() . Cover the picture, to the right of the black arrow and try predicting confidently.

. Cover the picture, to the right of the black arrow and try predicting confidently.

Chart reading and prediction is easier to accept in hindsight. Acting upon every signal is difficult, and if not acted upon, then the heuristic of action is weak. We can always say it will be interesting to watch what will happen in the future, but our actions of today are not commiserate of the events of the future.

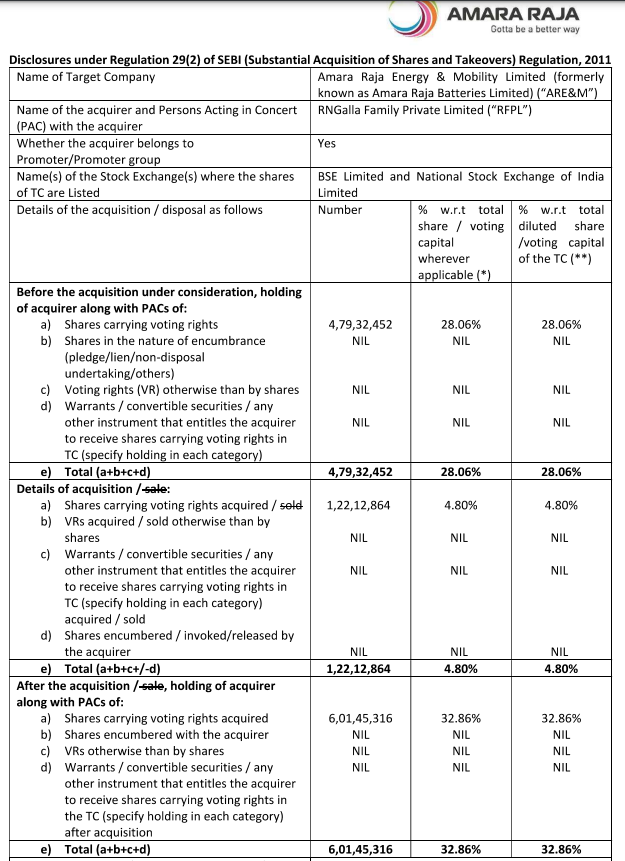

28.06% to 32.86% Shareholding promoters Risen

E-waste recycling has been made mandatory by GOI last year, this is the trigger for demand, and e-waste is a very real problem that needs to be addressed.

Mgmt is talking about growing their revenues 3.5x next year and then doubling in the subsequent year. So you can do the math.

Plus EPR revenues will also come in a major way. they have not given a figure on the EPR fees, but even if you take Rs 30/kg fees. Its still a decent number.

Execution is something we as an investor we are betting on.

SO even if you ascribe a 25 P/E on FY25 earnings, which is very fair given the growth prospects. There is a lot of upside

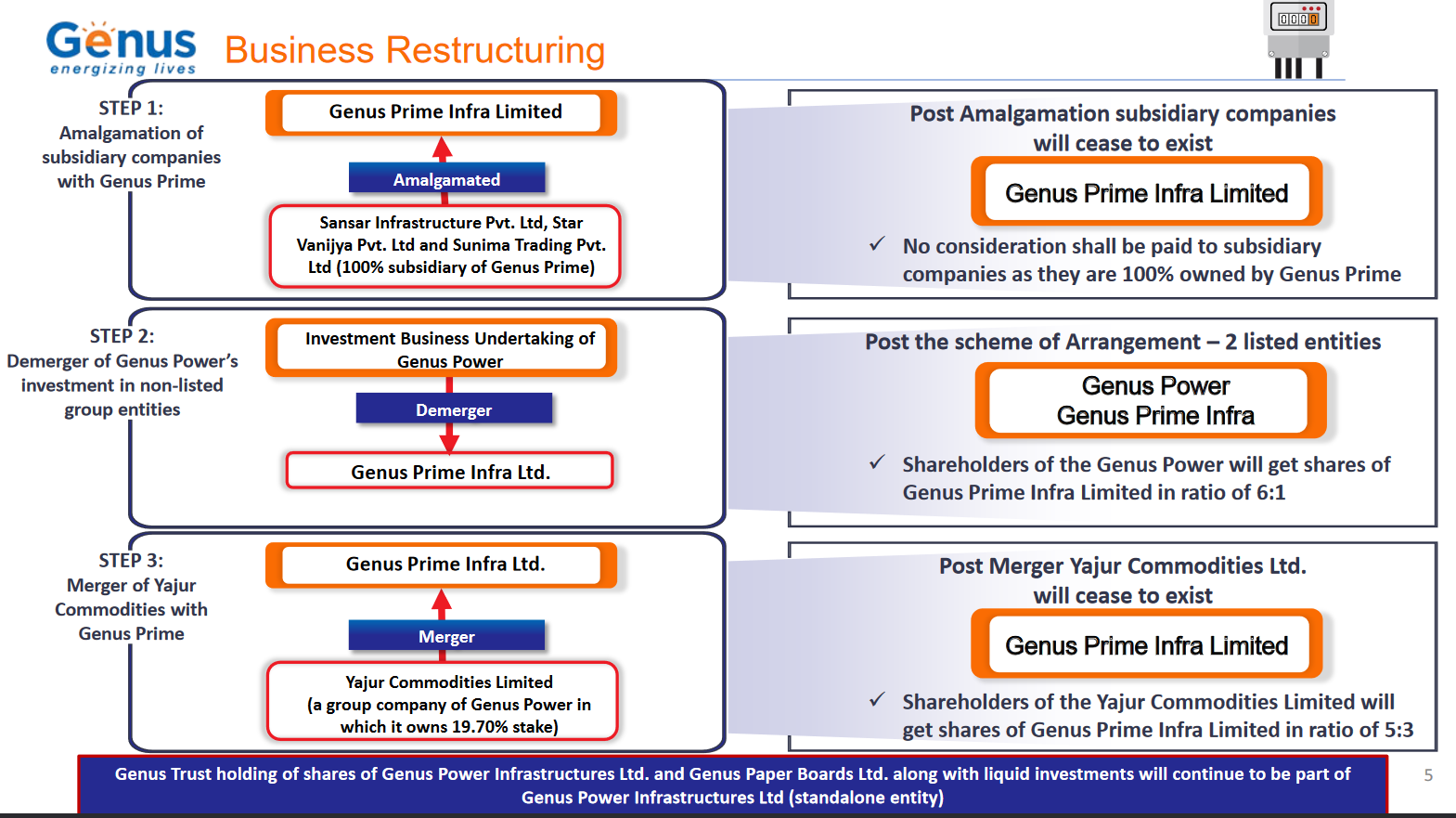

Genus Power: Business Restructuring

The recent presentation shows restructure of the company as shows in the image below.

I have a few questions which are as follows: