True…Hope so then I would be very happy… any way will hold for few more years. I think we have margin of safety.

Posts tagged Value Pickr

Green Hydrogen as a Fuel – Indian Companies leading the Green Revolution (16-02-2024)

Govt issues guidelines for using Green Hydrogen as a Fuel in 4-wheelers/ Trucks, buses at a budgetary outlay of INR 496 Crores till the financial year 2025-26

The scheme will support development of technologies for use of Green Hydrogen

based on fuel cell propulsion technology/internal combustion engine-based on 4 wheelers trucks / buses.

While the budgetary allowance is a miniscule, but it is good that the govt at least looking forward to implement it. The budget allowance is to develop hydrogen fueling stations to start with

Read more at:

Satia Industries – Journey towards Cyclical to Shallow Cyclical? (16-02-2024)

True that… however pakka is moving based on the futuristic products…it’s not apple to apple comparison.

On a side note…even Pakka was languishing at single digit pe 6 months ago!!

If Pakka can get rerated so can Satia!

Cash rich…debt free…buybacks… efficieny… futuristic products…

Long list for Satia…it can achieve in coming times.

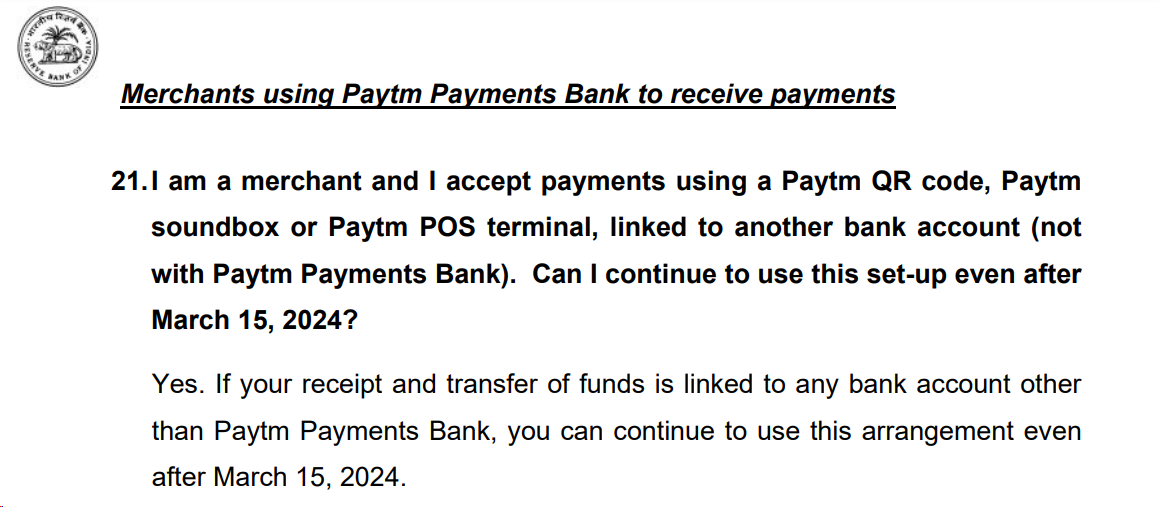

PayTM (One 97 Communications Ltd) (16-02-2024)

RBI has released FAQ and have extended deadline to 15th March for all things related (inbound trxn) Paytm Payment bank but for me below is the most important question.

https://rbidocs.rbi.org.in/rdocs/content/pdfs/PaytmPaymentsBankLtdFAQ16022024.pdf

https://rbidocs.rbi.org.in/rdocs/PressRelease/PDFs/PR1895ACTIONAGAINSTPAYTMPAYMENTSBANK0F4E6B2C2EFB4907A705CB81013AA24D.PDF

Disc. Have holding it in core portfolio.

Satia Industries – Journey towards Cyclical to Shallow Cyclical? (16-02-2024)

If Satia valued at Pakka base share price would have touched 500. Best example for theory does not work always in the market for me

Bull therapy 101-thread for technical analysis with the fundamentals (16-02-2024)

Shaily, Monthly – Broke out of the two year downward trend last month and continuing the trend post results. The business on the surface has been consolidating last 2 years and growth is back in the recent few quarters.

Shaily is into multiple segments of business from home furnishing, toys, steel furniture, automotive plastics and healthcare. Of interest to me is the last since it can be very high growth and also high margin business. It is a business where Shaily has strong moats due to the nature of business.

In healthcare division, there are multiple streams of revenue – from pharma devices to pharma packaging. Packaging is straight-forward as its containers for sterile liquids etc. (like eye drops) which is still not so exciting. The devices which involves, inhalers, pumps and pens (both contract manufacturing as well as own IP) is where possibly good growth lies in the future.

Shaily has 5 platforms of pen devices, used for different purposes from delivering insulin, GLP-1 molecules (semaglutide, liraglutide) and synthetic parathyroid hormones like teriparatide.

In insulin glargine, among the top 3 which is Novo Nordisk, Sanofi and Eli Lily, Shaily supplies the All Star line of pens to Sanofi. (they also supply for Wockhardt)

Bigger future growth could come from Semaglutide as Ozempic loses exclusivity where the management thinks they have 70% share in semaglutide generics market. This could be as big as half a billion pens in market size as per management. Current run rate for pens is at 14 million if am not mistaken (used to be 6 million 2 yrs back and scaling quite well)

Going forward the contribution from own IP pens will go up above contract manufacturing which will improve the margins. Also since Shaily owns the IP of these pens and the generic players who tie-up with Shaily for delivering their molecule end up paying a platform access fee which somewhat de-risks Shaily’s design and development efforts. This is fairly high margin (difference between consol and standalone is what is contributed by Shaily innovation UK is essentially platform access fee income) amounting to 14 Cr topline and 11 Cr at EBITDA level. As per management this accrues over 9-12 months and as they keep signing up new Customers, they have good visibility over next 2-3 years.

Actual sales of Semaglutide pens would happen from FY27 onward in RoW markets and FY29 in US where actual explosive growth could come. Until then, the design and development work has good near-term triggers.

It is a bit harder to model what numbers will be like without knowing what molecules they have signed on for what Customers (and what stage of approval they are in). This information might be available in next quarter and can provide much better visibility.

Valuation appears fair given the growth. Capacity utilisation is at low levels and utilisation levels are going to increase across segments as per management, so it doesn’t appear like any further capex is required in the near-term. Recent pens capex is about 125 Cr (done in last 2 yrs) and will be sufficient to do about 300 Cr topline. Cashflows could be used to pay off debt which can improve bottomline further in the future. Depreciation for new capex has already started hitting (capitalised in Oct ’23) so current rate can be projected to the future as well.

Risks:

- The rest of the business can be a drag. It still is ~85-90% of revenues. But healthcare will be 25% of topline by FY27 (this is ~30% margin in their own IP pens). Already topline growth is flat as their Ikea and toys business is degrowing but still performance is shining despite that as healthcare business grows 35-40%+ or so

- FDA risk – both from Shaily’s side and at innovator/generic manufacturer side

- Management has taken some steps in the past and reverted. Eg. Toys business seems to be winding down as customers are not sticky. Its good that they are course-correcting soon and focusing on what works. (Toys capex of 25 Cr seems to be used for appliances now)

- Management has overpromised and underdelivered in the past. This however might be changing as management appears almost scared and guarded these days

Also due credits to Aman Vij (@Rokrdude) who has been following this business for a long time and helped me get a quick grasp of things both directly and indirectly (from his insightful queries in the concalls across the years)

Disc: Invested between 460-470 levels. Am not qualified to advise and just sharing my trade note

I G Petrochemicals Ltd (16-02-2024)

I do not understand the cyclical part of it. Nor will I comment on the valuation bit. However, what I do know is that the company is very well managed! I’ve been supplying cables to them for the last decade or so.

I G Petrochemicals Ltd (16-02-2024)

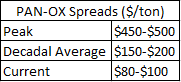

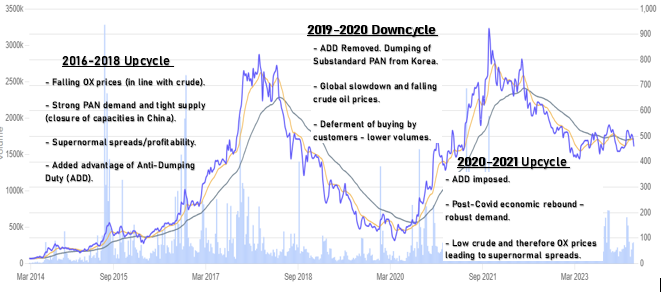

Things seem to be getting interesting here – one of the lowest cost producers (IG Petro) in a cyclical industry has now posted a loss at the EBITDA level. A further reduction in spreads would lead to shut-down of capacities in Taiwan, Korea & China.

Gross/EBITDA margins are at their lowest in recent history – main reason being…

Phthalic Anhydride-Orthoxylene (PAN-OX) spreads have almost come down to the company’s conversion cost of ~$85/ton. Further, Maleic Anhydride prices (where company earns an EBITDA margin of ~95%) are 10%-15% lower than PAN prices (compared to 10%-15% higher historically).

While domestic demand for PAN continues to grow (accounts for ~90% of the company’s revenue), geopolitical issues have temporarily impacted the key end-user industries (Pigments, Paints, Plasticizer, Specialty Chemicals). Rising Orthoxylene prices (key raw material – a derivative of crude oil), excess supply of Maleic Anhydride (MAN) are further reasons.

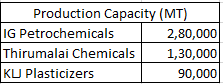

Virtual duopoly in the domestic market (IG Petro & Thirumalai), while KLJ has now backward integrated (used to import earlier). IG Petro is the second largest PAN manufacturer globally. This is predominantly a regional business and setting up a new plant takes 3-4 years (availability of raw material is a constraint).

Company has also forward integrated into Diethyl Phthalate (DEP) where EBITDA margins are relatively stable (in the range of 10%-15%).

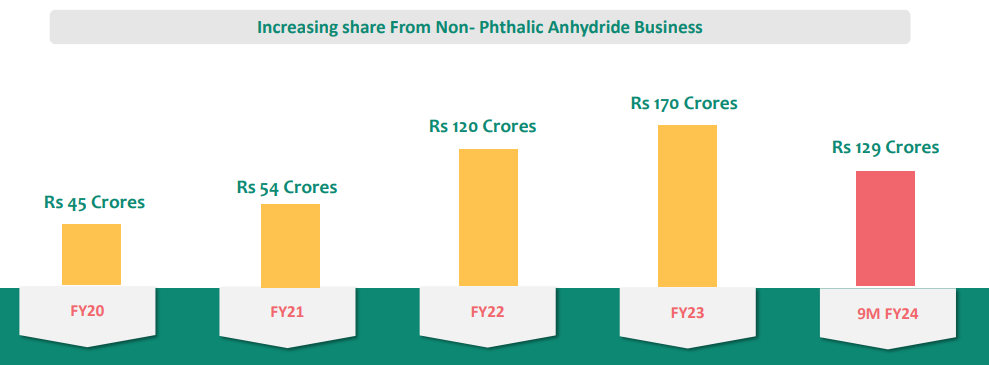

The share of Non-PAN business in the company’s revenue has been steadily increasing.

Meanwhile the company’s new plant has just commenced production and is expected to add ~Rs. 500 crores to the topline. Another Rs. 200 crore capacity expansion in DEP is being planned, with potential for Rs.800 crores in revenue. Demand for DEP is growing at 10%-15% annually.

Both IG Petro and Thirumalai have increased capacity. They expect the capacities to be absorbed given the strong domestic demand and growing use of PAN. China has built up 2 MT of MAN capacity for use in downstream capacities which are coming up (expected – Jan 2025). In the interim, this excess supply is leading to depressed prices. Overall things should only get better from here?

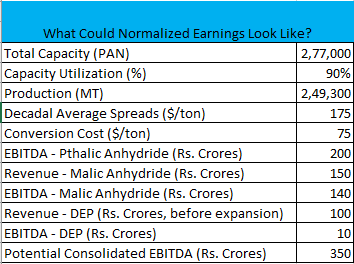

While the pain may last for a while, can the company do an EBITDA of ~Rs. 350 crores once the situation normalizes? If we assume this, company’s Profit After Tax should be around Rs. 200 crores (Other Income offsetting interest expense and depreciation of around Rs. 70 crores).

Brief Context on Past Cycles

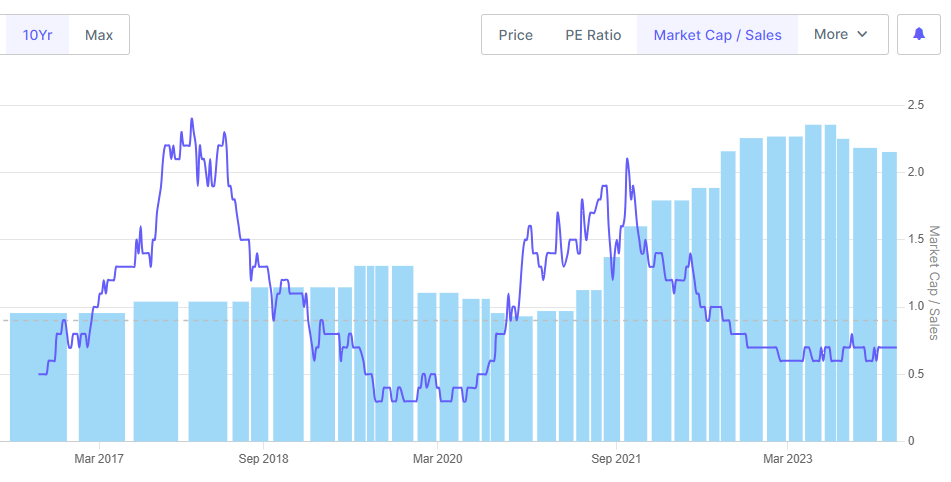

The tricky part seems to be – how does all this translate in terms of valuations/potential entry point? If this doesn’t work out, what could be the potential downside? And if it does, is the upside large enough to compensate for the waiting period and all the volatility?

A few open-ended questions in this context:

-

Price/Sales could be one way to look at it. However, with volatile sales, both due to fluctuating PAN prices as well as increase in volume from new plants, this on it’s own doesn’t provide the full picture?

-

Given that IG Petro is one of the lowest cost producers of this commodity with a net debt free balance sheet, a reasonable P/E or EV/EBITDA on normalized earnings could be assigned. What could be a reasonable multiple in such a case?

-

Decrease in institutional holding (FII+DII) or insider buying could be another important indicator?

Would love to get any thoughts.

CFF Fluid Control Limited – SME (16-02-2024)

One more order receipt.