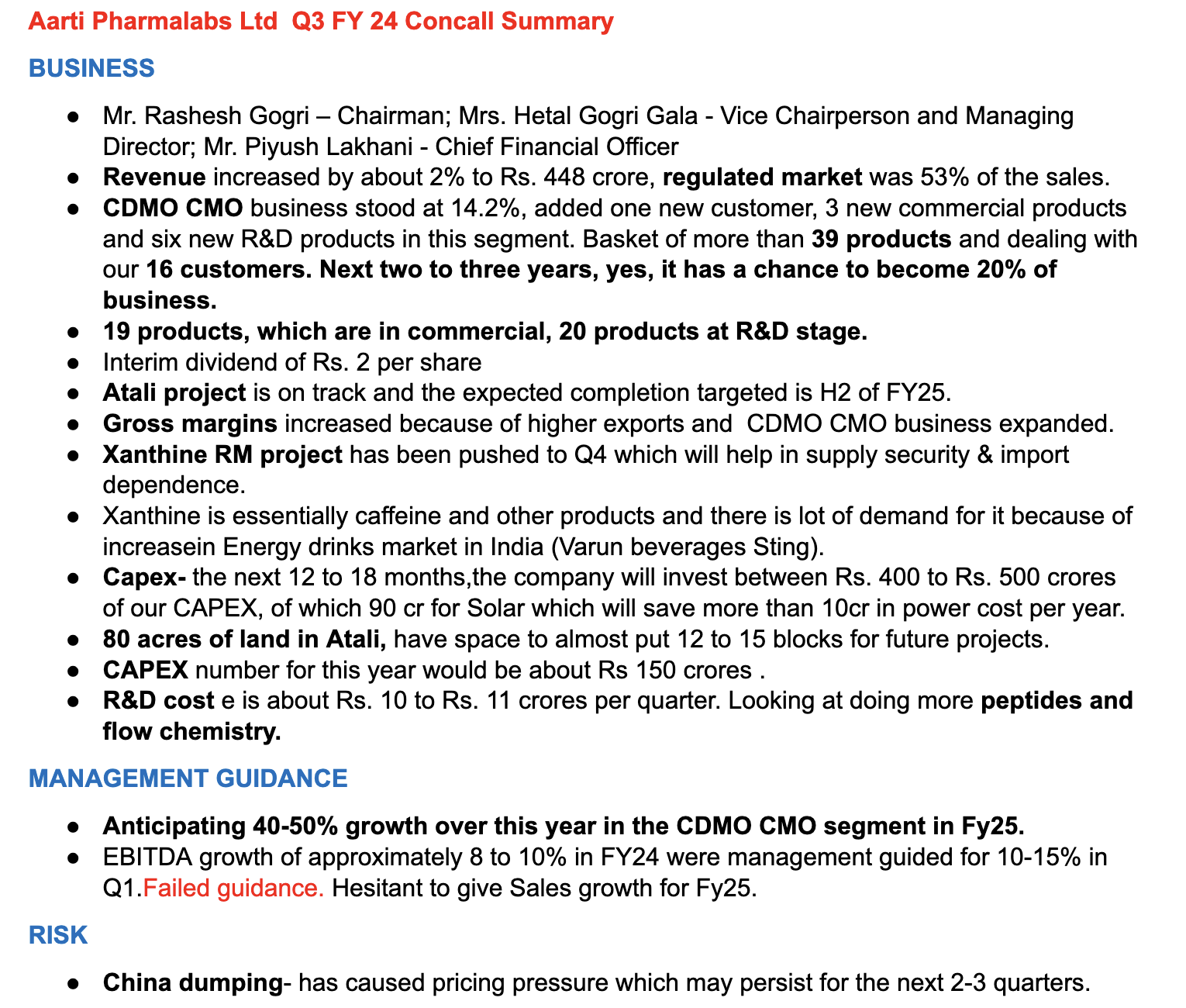

good results

https://www.bseindia.com/xml-data/corpfiling/AttachLive/f224393b-8894-479e-858d-1e02cb8c6493.pdf

Posts tagged Value Pickr

Nesco (14-02-2024)

Kovai Medical Center and Hospital – Health and Wealth (14-02-2024)

Were did you get the clinical materials ?

Dishman Carbogen Amcis Ltd (14-02-2024)

Dishman Carbogen seems to be coming out of a 5 year downtrend with the recently completed successful audits by the EDQM, AIFA and Japanese PDMA. Not only do these approvals open up incremental revenue opportunities, but this should finally enable the company to utilise Bavla much more relative to international French/Swiss operations and hence improve the margin profile.

As a story this reminds me of Piramal Pharma a couple of quarters back. This is an innovative CRAMS business with largely international operations and a management overhang (due to IT raids in 2019), offering deep value at 1.2x PS/0.5 PB. Recently significant Capex also has been completed and the France capex is scheduled to go live in upcoming Q4.

Eventually these are lumpy businesses and margins/revenues seem to be at an absolute bottom here last 3 quarters, in good times this has been a 25% OPM business. In general pharma tailwinds are now evident across the board and this is one company which should finally be able to use the completed inspections to significantly improve thier profitability/revenue profile, if not starting from results today but hopefully as things kick in in Q4’24 and FY 24/25.

Disclosure : Invested in self and family accounts and biased. I am not a SEBI registered advisor and this is not investment advice.

Dishman Carbogen Amcis Ltd (14-02-2024)

Dishman Carbogen seems to be coming out of a 5 year downtrend with the recently completed successful audits by the EDQM, AIFA and Japanese PDMA. Not only do these approvals open up incremental revenue opportunities, but this should finally enable the company to utilise Bavla much more relative to international French/Swiss operations and hence improve the margin profile.

As a story this reminds me of Piramal Pharma a couple of quarters back. This is an innovative CRAMS business with largely international operations and a management overhang (due to IT raids in 2019), offering deep value at 1.2x PS/0.5 PB. Recently significant Capex also has been completed and the France capex is scheduled to go live in upcoming Q4.

Eventually these are lumpy businesses and margins/revenues seem to be at an absolute bottom here last 3 quarters, in good times this has been a 25% OPM business. In general pharma tailwinds are now evident across the board and this is one company which should finally be able to use the completed inspections to significantly improve thier profitability/revenue profile, if not starting from results today but hopefully as things kick in in Q4’24 and FY 24/25.

Disclosure : Invested in self and family accounts and biased. I am not a SEBI registered advisor and this is not investment advice.

Mrs Bectors Food Specialities: Can it beat the industry? (14-02-2024)

Sir, from where we can track this data?

Entertainment Network India Limited (ENIL) (14-02-2024)

Fabulous results reported by ENIL, cyclicality seems to be playing out here in the media industry with last year being a major bottom. Ad spends have visibly already picked up and we have not reached Q4’24 and Q1’25 yet when the central election advertising starts kicking in.

In Q3 PAT has gone up to to 24 Cr for the quarter versus 3 Cr in Q2 and (8) Cr loss in Q3 last year. Revenues also saw a YOY increase of 21%.

The share price rise has been steep recently but valuation wise, at 12x trailing EV/EBITDA, this is still much below the 20x EV/EBITDA multiples this business has seen in good times earlier. Even Music Broadcast, a business in the same industry as ENIL but lower OPMs is currently trading at EV/EBITDA of 16+.

With Gaana now in their basket, plus all the digital initiatives with Mirchi, the streaming story is picking up pace. Hopefully with election spends, we are looking at a solid Q4 and Q1 ahead.

Disclosure : Same as above, invested since Aug’23 and biased. Added more last week. I am not a SEBI registered advisor and this is not investment advice.

Antony Waste – Long Term (14-02-2024)

Any reason for such a big fall? Results were not that bad

Antony Waste – Long Term (14-02-2024)

Any reason for such a big fall? Results were not that bad