My qualifications are B.Com and LLB. Am I eligible to register myself with SEBI as a research analyst?”

Posts tagged Value Pickr

Senco Gold: Upcoming gold story! (13-02-2024)

Senco posted a robust topline growth in Q3 FY24 yoy and 9M FY24 yoy. Whereas bottom line was down due to reduction in margins. Not an expert of this, can someone let me know is the margins hit due to increase in gold prices? I can see the cost of materials consumed is 79% of total sales against 67% last year same quarter.

| Q3 FY24 | Q3 FY23 | YOY | Q2 FY24 | QOQ | 9M FY24 | 9M FY23 | YOY | |

|---|---|---|---|---|---|---|---|---|

| Revenue | 1651.24 | 1344.47 | 22.82% | 1144.4 | 44.29% | 4099.73 | 3262.78 | 25.65% |

| EBITDA | 190.01 | 172.34 | 10.25% | 50.52 | 276.11% | 317.18 | 273.66 | 15.90% |

| EBITDA % | 11.51% | 12.82% | -10.23% | 4.41% | 160.66% | 7.74% | 8.39% | -7.76% |

| PAT | 108.62 | 103.11 | 5.34% | 10.69 | 916.09% | 146.73 | 132.24 | 10.96% |

| PAT % | 6.58% | 7.67% | -14.23% | 0.93% | 604.21% | 3.58% | 4.05% | -11.69% |

Edelweiss Financial Services (13-02-2024)

Disagree on ARC.

Look at ROEs on that one.

This used to be a very good business 5-7yrs ago. Now there’s restrictions on ownership structures and leverage – that makes this a lot less attractive.

Cineline India – Picture abhi baaki hai (13-02-2024)

Looks like a decent result. Overall turn around is on the way—2 quarters now of continuous profit. The hotel business is steady and the movie business is becoming bigger. QoQ will vary some what depending on releases.

YM Portfolio For Long Term (13-02-2024)

Whats your thesis on Refex industries? What % of your portfolio is in it?

Rahul Kumar’s Portfolio Review: Stock Market Investment Journey (13-02-2024)

Whats your thesis on Refex industries from here?

Som Distilleries and Breweries (13-02-2024)

Promoters’ ongoing purchases from the open market may be seen as a positive development. However, these disclosures suggest a strategy to accumulate as much stake as possible, potentially at the expense of current stakeholders’ interests.

The question arises: Is it legal to acquire such stake at any valuation without shareholders’ permission? If so, promoters could feasibly continue acquiring stake in the future, even at lower valuations, without restrictions. Does the law permit such activities openly?

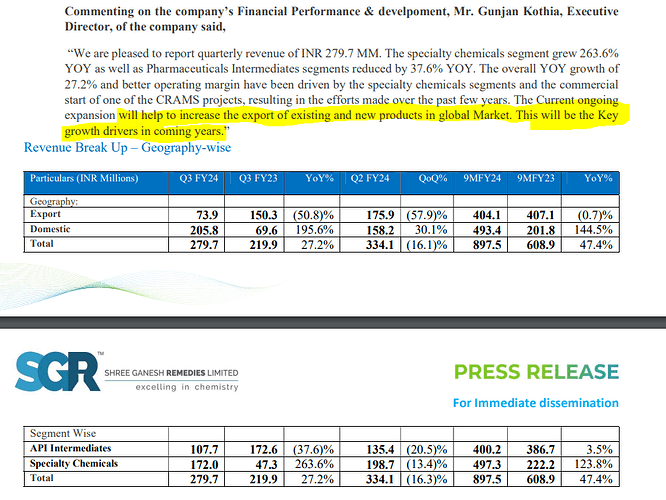

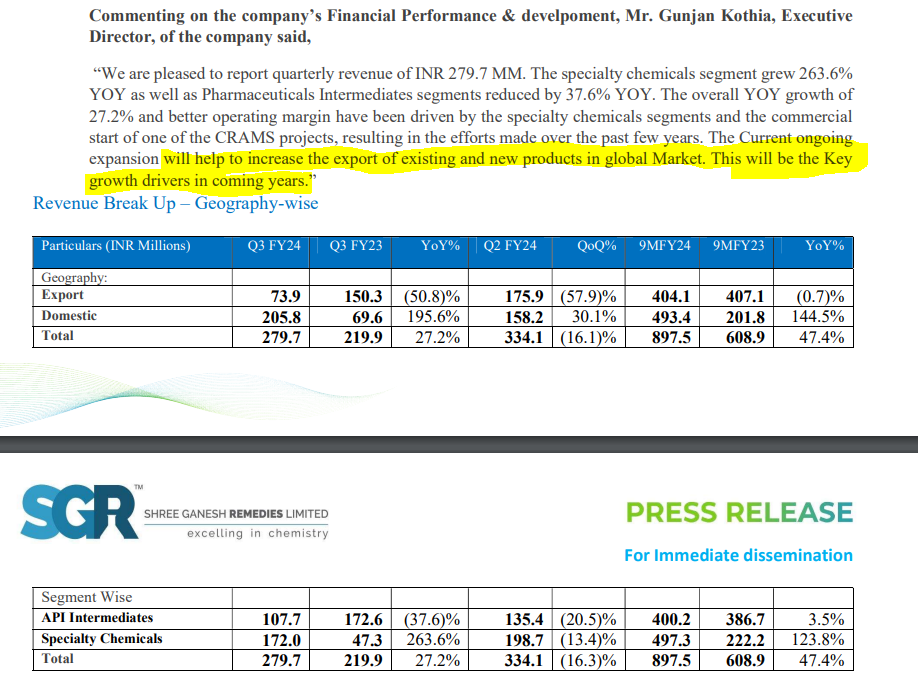

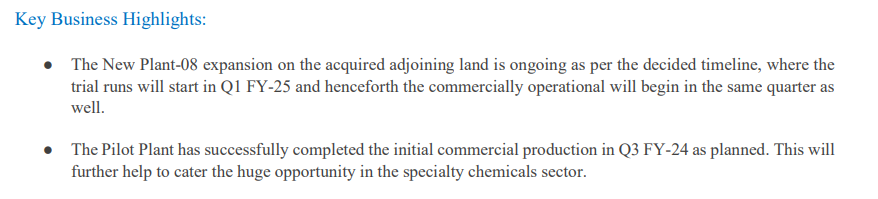

Shree Ganesh Remedies Limited (SGRL) – A pioneer in API intermediaries and Speciality chemicals? (13-02-2024)

SGRL posted a mixed set of Q3 FY24 results.

| Q3 FY24 | Q3 FY23 | YOY | Q2 FY24 | QOQ | 9M FY24 | 9M FY23 | YOY | |

|---|---|---|---|---|---|---|---|---|

| Revenue | 27.97 | 21.99 | 27.19% | 33.42 | -16.31% | 88.11 | 60.89 | 44.70% |

| EBITDA | 9.32 | 6.79 | 37.26% | 10.03 | -7.08% | 26.86 | 17.77 | 51.15% |

| EBITDA % | 33.32% | 30.88% | 7.91% | 30.01% | 11.03% | 30.48% | 29.18% | 4.46% |

| PAT | 4.8 | 4.35 | 10.34% | 6.55 | -26.72% | 16.12 | 11.15 | 44.57% |

| PAT % | 17.16% | 19.78% | -13.25% | 19.60% | -12.44% | 18.30% | 18.31% | -0.09% |

Financial Highlights

- Company posted a robust 27% yoy increase in revenue, with 37.26% increase in EBITDA and 244bps in EBIDTA margins as well (at 33.32%).

- Tax rate was 35% (against ~24% qoq/yoy) causing a dent in the PAT (down 13% yoy).

- On a qoq basis company posted de-growth of 16% in revenues and 27% in PAT.

- While Specialty chemicals posted robust growth, there is a significant de-growth in API intermediaries revenue and export revenues. The increase in margins attributed to the one of CAMS projects being commercialized.

Business updates

References:

MTAR Technologies – A wager on innovation meeting economies of scale (13-02-2024)

I feel that Q4 will be flattish YoY & expected growth of FY24 is differed by 1 year to FY25.

Order inflow is quite strong in Q3 and i expect that Q4 will see more orders, as long as the orderbook is building then i don’t see any much risk.

Electrolyzers opportunity is much bigger than these SOFC boxes, fluence energy & product related revenue (import substitutes) can contribute significant revenue in FY25.

Techno electric engg ltd (13-02-2024)

Huge underperformance in topline growth but margins holding up is great.

1000cr revenue guidance in Q3 and Q4 combined doesn’t look possible now.

Also they will raise 1250cr not sure why.

Let’s see what they say in the concall ![]()

Disclosure : Biased