Long term chart shows that whenever the divergence between BSE Small cap index and nifty 50 doubles, bse small cap index corrected to the level of nifty 50. It will be interesting to watch what will happen this time.

Long term chart shows that whenever the divergence between BSE Small cap index and nifty 50 doubles, bse small cap index corrected to the level of nifty 50. It will be interesting to watch what will happen this time.

I don’t see it as a red flag either. On the contrary, I like the fact that they are being pro-active in keeping us in the loop by providing all the key updates and happenings. If I look at the last few messages i received, they talk about 1. Launch of MSME Sampark – which has details of how the MSME ecosystem is evolving 2. Impact analysis of the interim budget 3. Confirmation about raising 250 crores through NCDs 4. Earnings report 5. Press release of Q3 FY24

Maybe what we can watch out for is, see if they will continue to send all information, even bad news, with the same enthusiasm and transparency. If they do, this is a good move.

Markets have been extremely volatile in the last two or three days. There has been a sharp decline in stocks especially in the mid and small caps. This is a feature of investing in such stocks. The ride is bumpy but has better longer term rewards.

The market can do one of three things at any time.

The probability of markets going up or down linearly is usually very low. That means you will not find stocks going up every day for very long. Every few days, it will correct or go sideways.

When markets are going down very rapidly, you again have three choices:

My default position is to do nothing if I have conviction in the stock(s) that I am holding. Exactly like I do nothing when stocks are going sharply up. Most of the time doing nothing works to your advantage. The problem with investors is they are mostly looking for action. They are glued to their mobiles checking the broker account or moneycontrol portfolio and this creates an itch to do something at all times. The other problem is they don’t have any conviction in the stocks they have bought because usually it is based on hearing a tip from some random person (and that includes analysts on TV, Twitter, YouTube, Telegram etc). So, a person who has very little conviction will be the first to throw in the towel when the going gets tough.

The next course of action I think of doing is to cut losses and triggering my stops. This is because I usually do not want to fight with the market. The market can decide to behave completely contrary to what I expect it to do. I respect both my capital and time. But this also means that you need to give a certain amount of breathing room for your stocks to bounce up and down without taking you out of your position.

The last option for me is to buy. And 99% of buying is if I am averaging up. I have stopped averaging down with only one exception – when I am in building a position.

First is to look at my portfolio or my watchlist and see if there is any stock where the allocation is lesser than what I wish. If so, then I top it up.

The other aspect I do is I will divide my capital to be deployed into 4-5 chunks and then use that every day the market goes down.

In case my allocations are as they should be, and still I have additional capital to deploy, then I will deploy it across all the stocks in my portfolio.

Only if there is very high conviction in those stocks. Currently, the market is doing a sector rotation every few months and stocks or industries that have done really well see more correction (both price and time-wise). For example, PSU stocks, railways and defence sectors have seen more severe falls than other sectors in the last three days. It is always prudent to let a stock stabilise before jumping in. That may mean you buy higher than the lowest point. But it also means the probabilities are in your favour.

These are two separate decisions. Do not club them into one. Whether you want to buy a stock based on its results is a separate decision. If you think the results are bad and you wish to exit, then do so.

Always keep in mind the basic tenet of doing nothing if nothing much has changed that warrants action.

Short, sharp corrections are par for the course in a bull market. One of the best ways to invest in an uptrending market is to do a SIP. If you are buying stocks yourself, buy on the days the markets are down. You don’t have to rush in to buy everything in one day. There will always be opportunities in the market.

With a regular SIP mode of investing, you will be better psychologically positioned than investing in a lump sum.

When markets are volatile, it is worthwhile to remember these basic tenets:

[Discl: invested]

[Discl: invested]

A preferred supplier to global off-highway vehicle market.

Uniparts is present both in the OEM and aftermarket segments in the off-highway industry with strong global operating model and wide customer base comprising of over 125 customers from across the globe.

Our products are shipped to over 25 countries worldwide

North America agricultural equipment market demand continues to be soft and in the short term, especially for smaller equipment

Europe: stable to marginally down

Domestic: soft

New orders

Excellent Results .

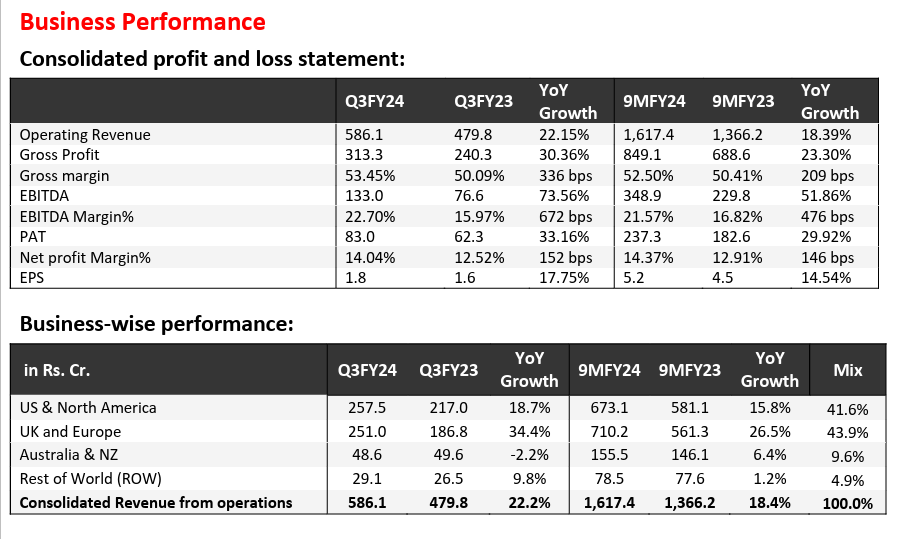

Q3FY24 Financial Highlights

![]() Operating revenue was Rs. 586.1 cr., up by 22.2% YoY driven by market share gains, new launches, the addition of new customers, an increase in our share with existing customers, and incremental contributions from the acquired Teva facility.

Operating revenue was Rs. 586.1 cr., up by 22.2% YoY driven by market share gains, new launches, the addition of new customers, an increase in our share with existing customers, and incremental contributions from the acquired Teva facility.

![]() Gross profit was Rs. 313.3 cr., up by +30.4% YoY with a Gross margin of 53.5%.

Gross profit was Rs. 313.3 cr., up by +30.4% YoY with a Gross margin of 53.5%.

![]() EBITDA was Rs. 133 cr., grew by 73.6% with an EBITDA margin of 22.7%

EBITDA was Rs. 133 cr., grew by 73.6% with an EBITDA margin of 22.7%

![]() EPS grew by 17.8% YoY to Rs. 1.84

EPS grew by 17.8% YoY to Rs. 1.84

Business Highlights

US Market

![]() US & North America Formulation business reported growth of 15.8% YoY to Rs. 673.1 cr.in 9MFY24 on account of new product launches and also due to an increase in the share of existing products.

US & North America Formulation business reported growth of 15.8% YoY to Rs. 673.1 cr.in 9MFY24 on account of new product launches and also due to an increase in the share of existing products.

UK and Europe Market

![]() Revenue of Rs. 710.2 cr. from the UK and Europe Formulation business in 9MFY24 as compared to Rs. 561.3 cr. during last year, registering a growth of 26.5%.

Revenue of Rs. 710.2 cr. from the UK and Europe Formulation business in 9MFY24 as compared to Rs. 561.3 cr. during last year, registering a growth of 26.5%.

Australia and New Zealand Market

![]() Australia and New Zealand business reported Rs. 155.5 cr. in 9MFY24, which grew by 6.4% YoY, due to incremental market share.

Australia and New Zealand business reported Rs. 155.5 cr. in 9MFY24, which grew by 6.4% YoY, due to incremental market share.

RoW Market

![]() RoW business reported Rs. 78.5 cr. in 9MFY24

RoW business reported Rs. 78.5 cr. in 9MFY24

Other Highlights

![]() In 9MFY24, the capex incurred was Rs 160.6 cr. Capex investment is in line with plan for scaling the acquired manufacturing unit from Teva Pharma in Goa which will drive future growth.

In 9MFY24, the capex incurred was Rs 160.6 cr. Capex investment is in line with plan for scaling the acquired manufacturing unit from Teva Pharma in Goa which will drive future growth.

![]() Cash Balance at the end of 31st December 2023 is at Rs 688 cr.

Cash Balance at the end of 31st December 2023 is at Rs 688 cr.

![]() In 9MFY24, Cash from Operations is at Rs 169.0 cr. and Free Cash Flow is at 8.4 cr.

In 9MFY24, Cash from Operations is at Rs 169.0 cr. and Free Cash Flow is at 8.4 cr.

I don’t see it as a red flag. The more disclosure a company does, the better it is for shareholders.

The ongoing beating since last 3 days, so far has beaten overvalued small caps, few names are already beaten by -30%.

how strong does smallcap space look now ?

I am sure it isnt at ~100. So, is it just an intermittent beating or they are driving them small caps out of party ? how hot does it look, still touchable ?

I tried touching few yesterday, it still hurts ! yet trying to touch some ![]()

![]()

Ugro capital has touched 200 DMA today. Correction was with low volume so indicating not much worry on technical front.

But recently company has started updating events and disclosure via whatsapp. I would take it as a red flag as when a company over emphasised its achievement to retail shareholders, “dal me kuch to kala hai…”

I want to know boarders view on that. Are there any other companies doing so? Is it a normal trend?