PEL has iterated in the last few calls regarding its compliance to the housing finance company and discussion with NHB/RBI regarding the same. They have shown intent of retaining that… If that is the case I doubt they can get into Land financing as they can’t have a subsidiary in housing finance while the parent (NBFC) doing land finance.

Posts tagged Value Pickr

Borosil Limited (13-02-2024)

Excellent Q3 FY24 results from Borosil consumer division. YOY revenue growth of more than 45% with EBITDA, PAT growing 101% & 134%. Looking forward for the concall.

| Q3 FY24 | Q3 FY23 | YOY | Q2 FY24 | QOQ | 9M FY24 | 9M FY23 | YOY | |

|---|---|---|---|---|---|---|---|---|

| Revenue | 302.45 | 207.17 | 45.99% | 234.87 | 28.77% | 713.37 | 565.03 | 26.25% |

| EBITDA | 64.42 | 21.94 | 193.62% | 39.31 | 63.88% | 124.7 | 71.01 | 75.61% |

| EBITDA % | 21.30% | 10.59% | 101.12% | 16.74% | 27.26% | 17.48% | 12.57% | 39.09% |

| PAT | 37.3 | 15.93 | 134.15% | 18.54 | 101.19% | 60.79 | 48.73 | 24.75% |

| PAT % | 12.33% | 7.69% | 60.39% | 7.89% | 56.23% | 8.52% | 8.62% | -1.19% |

PI Industries – Superior Business Model (13-02-2024)

Correct cash is 3292 crore, not 19,500 crores

” * Company has large cash, liquid funds & fixed deposits of around Rs 19,500 Cr, primarily from past fundraise”.

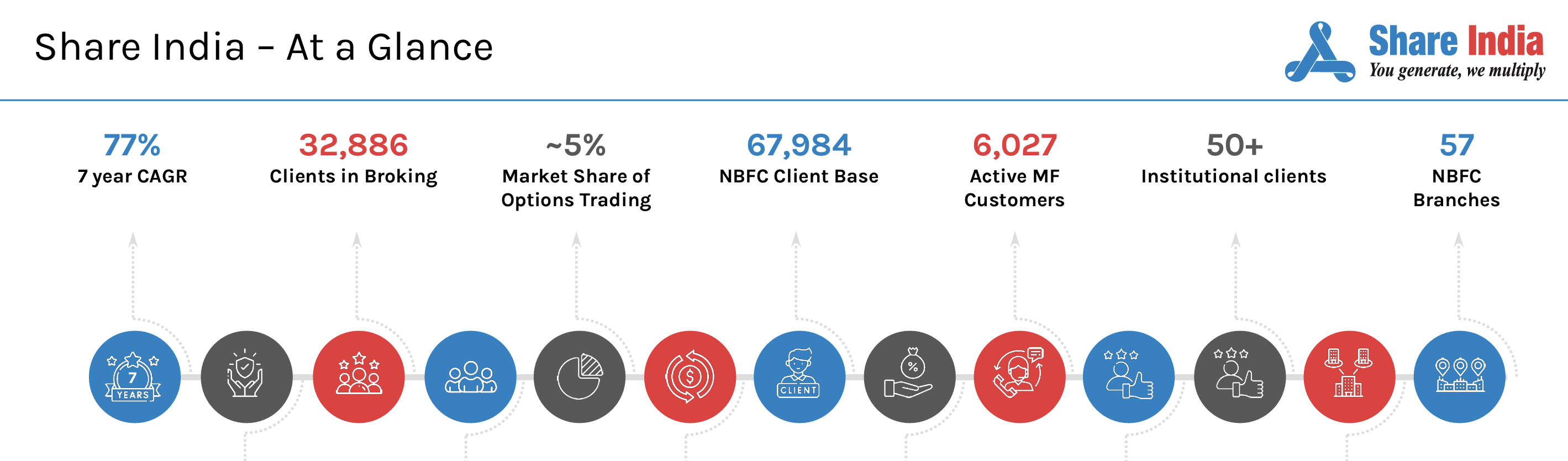

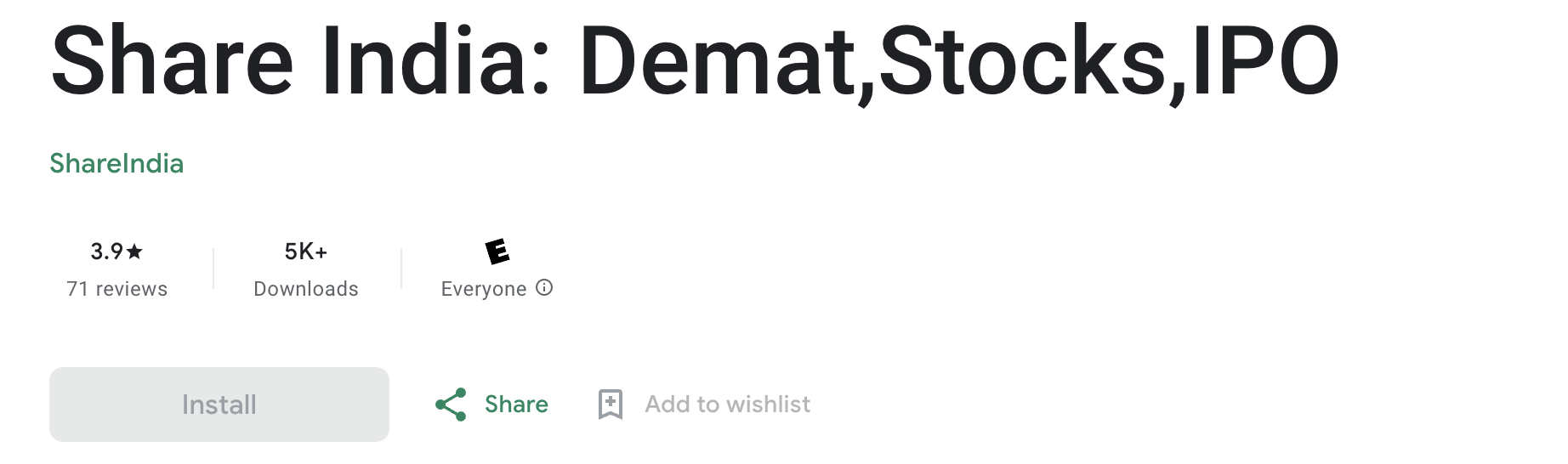

Share India Securities – will they give security to Retail (13-02-2024)

Hi all,

I am trying to make sense of number of broking customers of the business. As

As per Q3 FY24 presentation, they have 32,886 clients in broking.

However, in Google play store the number of downloads for Share India (Demat and Stocks app) are only 5000. If I triple the count to account for apple and web users, it comes around 15,000. Does anyone know what am I missing?

Cupid Ltd – Helping the world play safe! (13-02-2024)

Big decision for me today.

I’ve completely exited Cupid @ 14x from the Average Cost and almost 18x from the Lowest Cost.

The primary reason is the Valuation. Even if the Revenue triples in 5 years as targeted and you apply a high growth rate post that (Say 20% for 20 years), the company would still be Overvalued. The Valuations could still support a very Bullish case, but I’m not comfortable with that.

Lessons I gleaned during this journey:

-

“Promoter Risk” is overrated (Unless in cases of fraud). At the best, it could be a Minor Risk. Of course a passionate and driven Promoter is excellent. But if the Business Fundamentals are strong, even a decent successor will be able to run it effectively. So, Fundamentals before anything else.

-

There will be thousands of naysayers for any given investment. It’s your job to monitor and justify the investment to yourself. Conviction is your rock. Conviction comes from cold, hard, self-introspected facts and not opinions. Opinions, especially from experts, do matter. But you’ve to verify them yourself against data once to build up Conviction.

-

Finally, an often repeated one — the patience to hold is one of the paramount virtues in investing. It’s as important as buying at the right price. If you’ve done all the work, then holding is the final lap. Do it well.

My sincere thanks to Mr. Garg and all the very best to Mr. Halwasiya for the future.

Note: I might consider entering again after seeing more proof of execution. At a much, much lower Price though for sure.

PayTM (One 97 Communications Ltd) (13-02-2024)

I look at this scenario with this perspective…

When Phonepe had to migrate from Yes Bank to ICICI bank because of RBI diktat in 2020, UPI’s major utility was P2P than P2M. In P2P, the underlying account remains with an existing bank and a virtual payment address is provided by the UPI Player in tie-up with a bank like ICICI or Axis or Yes bank. You may observe that when you create a new Virtual payment address, on a new UPI app, its created instantaneously without any KYC completion. So Phonepe had only migrated the Virtual address and not the underlying account which is a far easier exercise

But the situation can be very different when it comes to the merchant onboarding which gained traction around 2021 with BharatPe cracking this model.

In this P2M model, a QR/ Soundbox issuer like Paytm gives the product along with the underlying bank account with a bank account… Paytm having exclusive Payments bank license, it routed all its merchants to PPBL to maximize the opportunity. When the underlying new account is that of Paytm, it is obligated to complete the KYC. Now when you transfer the underlying account, either of 2 things should happen:

-

Merchant has an existing alternative KYC verified account and Paytm has to just link the QR Code to that account and merchant can continue to operate with that account — (heavy on Ops – Merchant should be reached out to by Feet on street and collect the new account number and then link the current QR Code)

-

Merchant has no existing alternative KYC account and Paytm has to issue a new account with Axis/ ICICI/ Yes Bank and get the KYC done with the new bank and then link the QR to that newly opened account — (Centralized Activity – KYC to be collected and bank account to be created by FoS)

I think Paytm will focus on migrating the merchants who had loan accounts with them followed by Sound box merchants followed by QR Stickers to migrate. But even if any of these get missed, it will be a reputation risk for Paytm and will have deleterious consequences on the paytm brand name

But I hope and believe that Paytm will be able to overcome this within deadline or work back with RBI for an extension

PS: This is my understanding of the process from my secondary research. Please feel free to correct my understanding

Discl: Invested

PayTM (One 97 Communications Ltd) (13-02-2024)

The problem is not kyc but something else. Kyc is done by bank where you have your saving account and not by upi sponser bank. For example, if you create a new upi on a different app, say mobikwik, today, it will be active immediately without any kyc and its sponser bank (HDFC) won’t come to you asking for your docs. If you want to use wallet, then kyc is necessary. So if paytm ties up with a third party bank to ensure continuation of wallet, then it will be a big headache for the partner bank to do crores of kyc all over again.

Also banks are hesitating to partner with paytm because RBI is very angry at it. Yesterday, Axis bank MD said paytm is a big player and they would be happy to work with them, IF the RBI permits

PayTM (One 97 Communications Ltd) (13-02-2024)

There are 3 kinds of txns w.r.t. merchants:

Type 1. P2P – similar to the Phonepe 2020 case where consumers transact with other consumers

Type 2. P2M (soundbox) – consumer transacts with a merchant using UPI modality (~0% MDR but subvented by banks) – may be individual KYC necessary

Type 3. P2M (POS machines) – consumers transact with merchants (typically big box retailers) where alongside UPI, there are other instruments like CC/DC/EMI as well.

Paytm doesn’t divulge into each of the above categories. Overall there are ~40mn merchants (~10Mn having soundbox i.e. no. 2) and ~300 mn consumers.

Overall above 3 types of transactions accrue 7-9 bps at a net revenue basis with gross being around 30-35 bps which at the scale of Rs 5 trillion per qtr is decent at 25-30% gross margin.

My assumption is case 3 has to be re-KYC surely with there’s VISA/MC etc involved along with banks. Not sure about type 2 (maybe someone can shed some light).

So size and scale of Paytm might dampen their swift transition, which I believe Suresh is alluding to in fewer words.

That’s my 2 cents. Happy to be proved wrong and corrected.

Disc: no holding. closely tracking to see if the evidence so far merits an action.

TCI Express – Logistics Sector niche player (13-02-2024)

Thanks for sharing. Are’nt TCI Express and Delhivery’s customer base different? Correct me if I am wrong – TCI Express is more B to B and Delhivery B to C. TCI Express with its sticky customer base and per mgt commentary post Q2 results, margins were to improve in the second half year from the achieved margins of 15.8% in Q2. Mr. Agarwal further mentioned that Q3 and Q4 FY2024, will have higher growth and committed volumes would be achieved. The Margins and revenues though seemed to be flat in Q3.

Again during Q2 concalls – festive season and resilient domestic demand were expected to be favorable for Q3 results due to higher utilization but the mgt perspective post Q3 results mention of continued headwinds on account of muted festive demand and long holiday season during the quarter. Mgt in its Q2 con call did not acknowledge the heightened competition in the industry as a bearing on its results. Revenue and volume guidance for FY 24 from prior concalls were to be 14 to 15% and 13% on volume. This would mean a last qtr revenue of approx 485 crores to stick to their guidance. Not sure if this is possible from its current quarterly average.

Clear case of mgt over promising and under delivering. Hope to see some expected gains in margins due to the Pune automation center.

Disclosure: Invested from slightly higher levels.

JTL Industries – Fast Grower at an inflexion point (13-02-2024)

company can operate at 65% capacity utilization because they have to customize products which requires change in lines.