BANDHAN BANK HAS GIVEN LOAN OF RS 22750/-CR.

85% has already paid by customer.

Pending amount Rs 3310cr.

bank has received 927 and 300cr additionally from customer and authority.

Now remaining amount is 2283cr. Bank has made provision 88% which comes to 2009cr.

Remaining amount is just 280cr. Calculated conservatively.

I am holding the shares.

Posts tagged Value Pickr

Bandhan Bank – in a sweet spot? (13-02-2024)

Newgen Software (13-02-2024)

Is the circuit just a sharp reaction to general sell-off and over-valuation or is there any news around Newgen? Can the better informed members kindly throw some light?

Everest Kanto Cylinders Ltd. – A long runway ahead! (13-02-2024)

While the management of EKC is sleeping, competition is setting up new plants…

PayTM (One 97 Communications Ltd) (13-02-2024)

Hi. In 2020, PhonePe went down because Yes Bank went down. Yes Bank used to be the sponsor bank for all UPI handles which were issued by PhonePe. For example if you went to PhonePe and linked your bank account you got a UPI handle which ended with @yesbank.

Now when Yes Bank went down, suddenly as a customer of PhonePe you could not make any transactions from the PhonePe app because the sponsor bank of your UPI handle was not working. So PhonePe spoke to NPCI and other banks. Within a day or so PhonePe got ICICI Bank as the sponsor bank. All UPI handles which ended with @yesbank were routed by NPCI towards ICICI. What do I mean by that? It is not as if your UPI handle on PhonePe app changed from @yesbank immediately. But whenever you wanted to do a UPI transaction on PhonePe, the sponsor bank at the backend whose servers were helping you complete the UPI transaction was ICICI.

Now ICICI could not have done KYC for crores of UPI customers of PhonePe overnight. I want to learn from this group why would the NPCI and RBI not allow the same thing for Paytm. Why would in Paytm’s case the new sponsor bank or banks be first asked to complete KYC for all the UPI handles? That is a major point which Suresh wasn’t asked. May be I am missing something.

Here are a few articles about what happened at the time of Yes Bank going down.

Shri Keshav Cements & Infra (13-02-2024)

Q3FY24 – Transcripts summary

-

Warrants have subscribed

-

Recognition – from The Bureau of Industrial Standards for meeting the highest quality of cement without any product failures over the past three years of observation

About the Business

350 – Distributors

500-600 – Retail Sales points

They are reducing around 75% – 80% of power cost by green plants

Permission has been granted for the expansion of the solar plant from the current capacity of 37 to 40-megawatt peak

-

Q1 final year will be similar

-

Q2 of next year is going to be a monsoon quarter

-

Q3 is a good quarter

-

Q4 will have little correction

Guidance

In the areas they are in almost 10 to 15 million tons of cement is being sold per month whereas they are only putting in a capacity of 1 million ton per annum which is very minuscule

They are aiming to reduce the dispatches on the delivered basis and relying mainly on an ex-plant basis

Guidance on pet coke – reduction of prices in the petroleum coke and Q4 they are expecting to go down

By FY ’26, they are targeting INR900 to INR1000 rupees EBITDA per Ton, and by 27 they are expecting 300 cr of revenues

By FY26 they are aiming for about 75% to 80% of capacity

At 80% efficiency of 1 million ton capacity Considering inflation and a projected revenue of 5,000 per ton, the revenue range is anticipated to be between 370 to 430 (presumably in crores INR) for the top line.

Management has got a very good experience in setting up the power plant

Why sales are flat

- The cost of the dispatches done in this quarter are typically ex-plant basis and the company is trying to reduce the dispatches on the delivered basis and relying mainly on an explant basis to dealers with discounted prices despite the increase in capacity utilization which has reached 76%

- The reason for doing so is not to be able to pass on the cost of logistics to the consumer.

Volumes

- FY23, there are 2,26,000 tons over the dispatch quantity

- As of 9months, it has reached 1,98,000

- Expecting the range of 240 to 245,000 tons for FY24

Reason for improvement in EBITDA & PAT

Changes in terms as mentioned above and reduction of prices in the petroleum coke

EBITDA – In this quarter 11.7 cr of EBITDA 8cr is contributed by solar

Reason for solar plant expunction

- For transmission from existing lines, 20% to 30% of the capital cost has already been incurred

- So now they are just enhancing the DC capacity to accommodate the existing electrical equipment capacity

- To accommodate this internal consumption of electricity without incurring additional costs such as cross-subsidy charges this plant will be added

- With this capacity of 3 Megawatt, they can increase EBITDA and are expected to be commissioned by April 2024

- After the expansion and commissioning of a new one-million-ton capacity in July, the power currently generated and potentially sellable to external parties dew to efficiencies will instead be consumed internally due to increased operations

- This setup allows for capitalizing on incentives for the existing power generation facilities, which can then continue to sell power externally with government incentives, while the new solar power project, supports the internal power needs

Inefficiencies

Until the capex is deployed their EBITDA per ton will be lower than the Industry

Now they are consuming 110 units per ton compared to 60 units per ton of electricity as per the industry

TRF – emerging from parent’s shadow! (13-02-2024)

Withdrawal of TRF’s merger with Tata Steel has triggered quiet a rally in TRF. I tend to agree with the upmove

My simple thesis on this name:

- Withdrawal of merger is a clear indication that the worst is behind – both financially and operationally

- A CHP (Coal Handling Plat) manufacturer, it is likely to be a beneficiary of growing thermal power need in the country. TRF is a vendor to BHEL who has been winning significant quantum of thermal power orders. Those should start to reflect in its vendor books as well.

- At 14x trailing PER, it is one of the cheapest stock among peer set.

- Finally, despite recent run-up, market cap is just INR 530cr. For a Tata Company, that should indicate signicant upside potential.

Happy to hear others’ views.

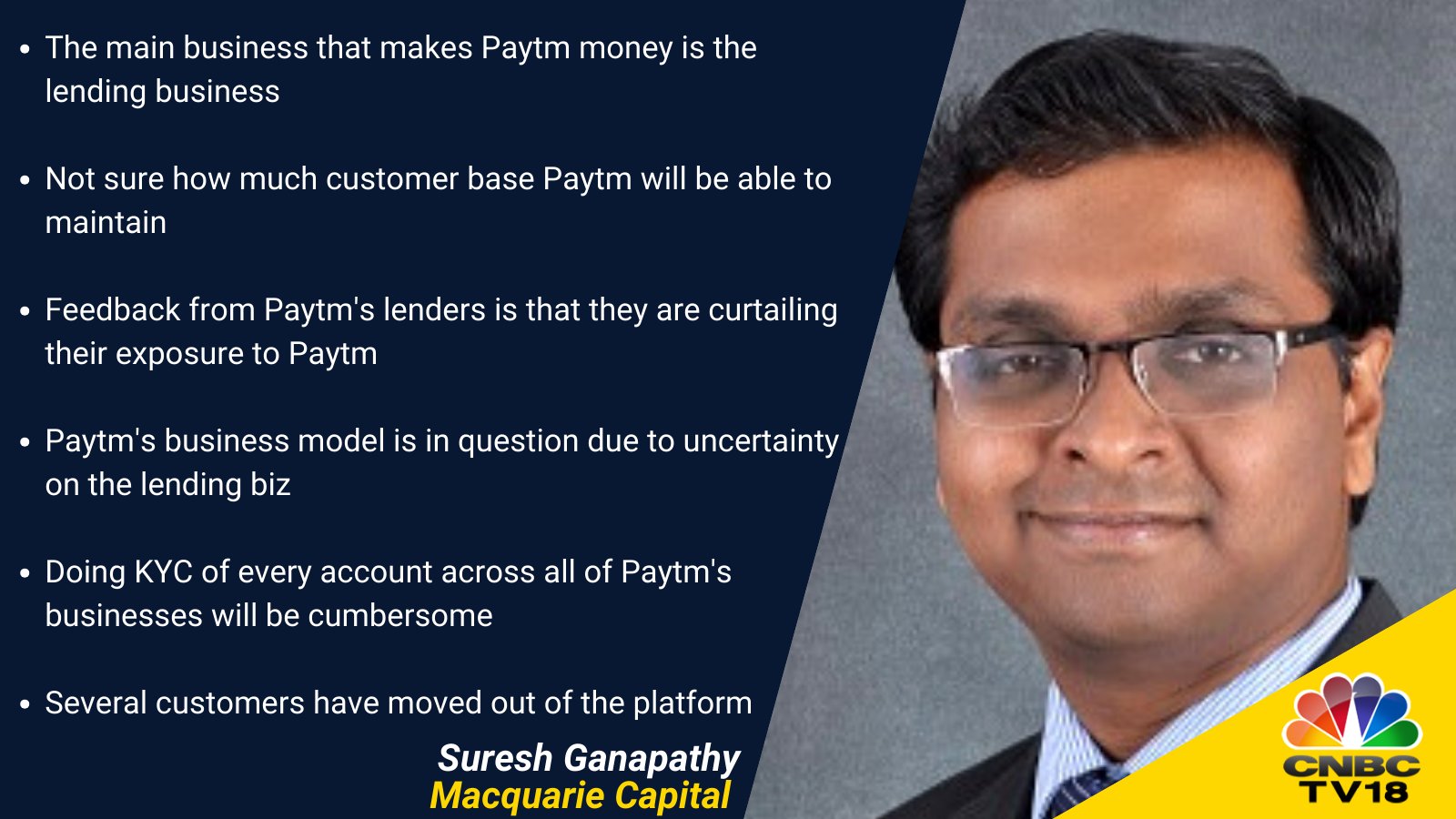

PayTM (One 97 Communications Ltd) (13-02-2024)

Last week, I asked a few questions – but didn’t get satisfactory answers. but Macquarie helps!

Current business is trading at ~2x book value.

Disc: no holding. closely tracking to see if the evidence so far merits an action.

Tata Steel – Would be merger be of any value? (13-02-2024)

Withdrawal of TRF’s merger with Tata Steel has triggered quiet a rally in TRF. I tend to agree with the upmove

My simple thesis on this name:

- Withdrawal of merger is a clear indication that the worst is behind – both financially and operationally

- A CHP (Coal Handling Plat) manufacturer, it is likely to be a beneficiary of growing thermal power need in the country. TRF is a vendor to BHEL who has been winning significant quantum of thermal power orders. Those should start to reflect in its vendor books as well.

- At 14x trailing PER, it is one of the cheapest stock among peer set.

- Finally, despite recent run-up, market cap is just INR 530cr. For a Tata Company, that should indicate signicant upside potential.

Happy to hear others’ views.

Globus Spirits (13-02-2024)

For the first time, since I’m looking at it, they’ve taken a good decision of not expanding capacity of ethanol. I think this should bring more focus on Consumer biz. Need to watch out as it is not easy to build a consumer brand.

Disc. Not invested at all and not planning to anytime soon.