What disaster numbers from KECL, and mgmt seems least bothered to give any clarification or updates.

Does anyone have any update on whats going on with the business?

Posts tagged Value Pickr

Kirloskar Electric – A Turnaround Bet? (12-02-2024)

PI Industries – Superior Business Model (12-02-2024)

Surplush cash is around 2800 or is it 19500 crore? Apology if i missed something

Apollo Hospital : The one stop healthcare service (12-02-2024)

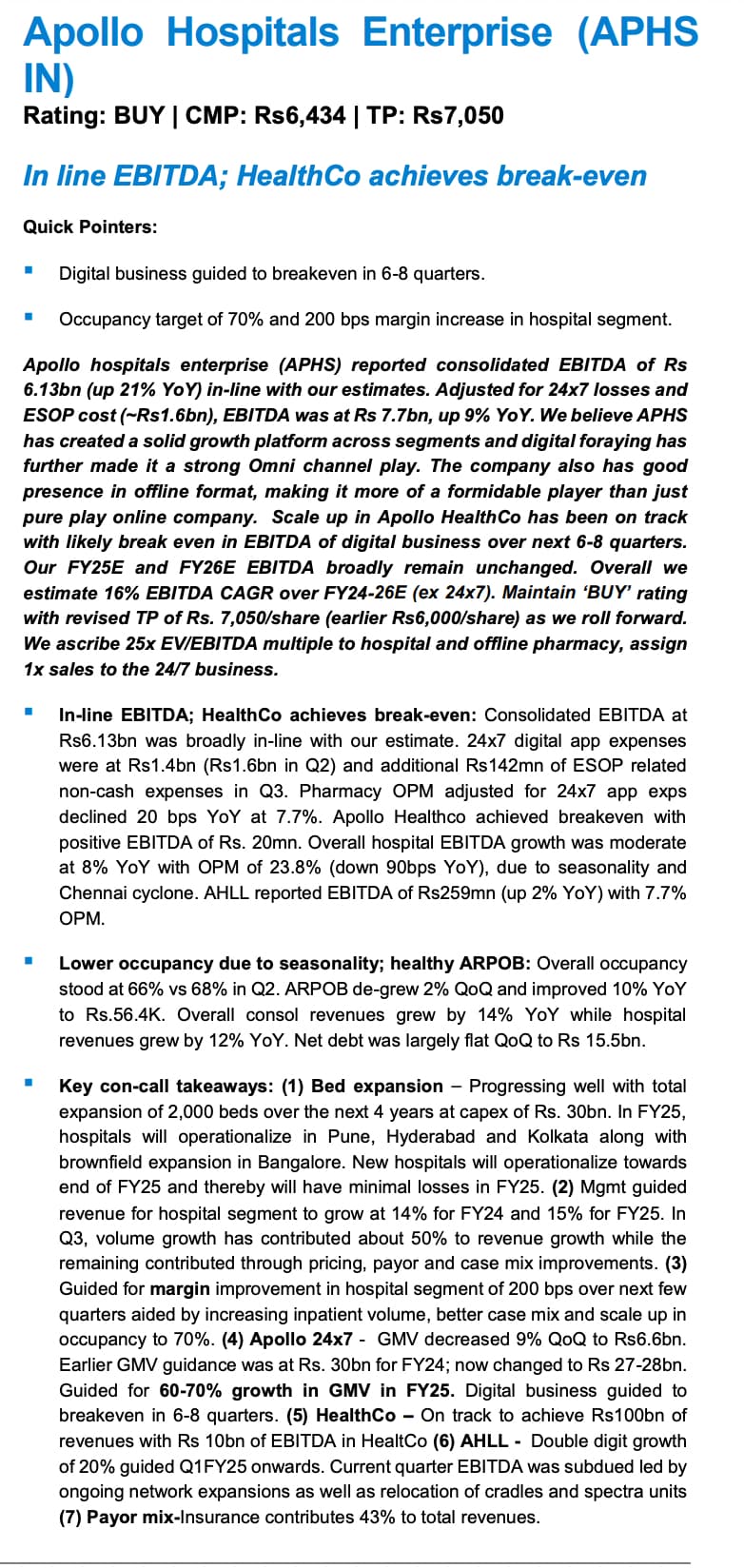

In line EBITDA; HealthCo achieves break-even

PI Industries – Superior Business Model (12-02-2024)

Q3 FY24 Conference call main points

The incremental growth (60℅) registered in this quarter has come from new molecules which has been developed ovr last 2-3 years.

Pyroxasulfone has gone generic in few countries and 10-15℅ price cut has been observed till now. It is going to go generic in other developed countries as well over the years.

The innovator for which PI is supplying this pyroxasulfone has got some extended patent registration for the formulation/combination making out of pyroxasulfone and this would in a way protects innovator and PI ultimately from the risk of pricing erosion.

PI has got 25-30 molecules in CSM buisness and so is pretty diversified in terms of overall product and revenue mix.

Some seasonality element on the dometic agri business side this quarter, management expects performance to improve and they have got quite a few branded products which they continue to market.

No guidance given by management for FY25, they would give it in Q4, reasonably confident of achieving 18-20℅ growth in overall business this year.

Recovered amount from the one off element is to the tune of 700mn.

Continue to work towards pharma, mainly towards improving infrastructure deploying resources and other development.

Pharma business to have similar margins as PI overall agri business margins (24-26℅).

Aspire to take pharma business to the 25℅ of overall revenue of PI in the coming 4-5 years.

HBL POWER SYSTEMS: Booting-up for the Race of the Century (12-02-2024)

It’s Mr. Market typical behaviour, we don’t have to find the reason for every down or up move, the situation is for taking the advantage either to buy or sell considering current and future prospects.

Lesson from Ben Grahams Intelligent Investor.

Share India Securities – will they give security to Retail (12-02-2024)

Here it is, but i don’t know, there is still a little bit of misunderstanding by me i guess, they have released on same date and have pledged also on same date, in morning i checked and it was showing this thing, i think they are doing it for personal purpose means trading from individual accounts. Here, in november also some release of pledge was there

Krishana Phoschem ltd – Agro – Based Multibagger? (12-02-2024)

Recent development which was missed

.

Government caps profit margin for fertiliser stocks

.

.

Also for the latest quarter the EPS is 0.60 ( last quarter 3.25 ). Higher expenses lead to lower margin. Need to dig deeper.

Bull therapy 101-thread for technical analysis with the fundamentals (12-02-2024)

@ashish_agarwal Please find the ceinsys AGM transcript here.

Update based on results so far

Garware, Daily – Strongest result and broke out with volumes post numbers.

Based on the concall, some of our guesswork came up right. PPF volumes ramping up very well. IPD still a drag but yet company has posted all-time-high revenue and profits. Margins have clear levers for growth above 20% when 1. IPD margins improve in the next 6-12 months 2. Market spends taper off 3. SCF volumes come back in summer.

Management thinks 600 Cr per quarter and so 2400 Cr topline is doable with current production lines which means, operating leverage accruing from fixed costs of production will also contribute to improving margins. No plans for merging GIL or selling Mumbai land but plans seem to be on for selling Aurangabad or Nashik land (don’t remember). A better capital utilisation plan will act as a trigger for re-rating alongside further improvement and sustenance in numbers

Sharda Motors, Monthly – Three months of sideways movement post breakout.

Results here too have been good. There’s clear volume growth in BS-VI, if we excuse the lack of topline growth due to company reducing catalyst trading and looking at gross profits. Essentially at an absolute level, profits are growing and understandably margins as well, with the trading component removed. Market has been chasing skirt with PSUs and ignoring value stocks like this but hopefully things will turn. One thing to note though is that TREM-V might be delayed to Apr ’26. I see it more as an optionality at this point and valuation doesn’t reflect even BS-VI growth at this point. Payouts have got to go up as well and are probably the reason market isn’t getting excited. Hopefully dividends for FY24 would be better.

Taal, Monthly – Support from previous monthly tops from ’22 and ’23. 2400-2500 levels should be strong support here.

Has been the worst result of the lot as margins have continued to be hit despite topline growing. The breakneck hiring done in FY24 (520 to 620 employees) is causing a big drag on margins (employee cost gone up from 22 Cr to 28 Cr per qtr). My thesis was that margins will revert back to 30-33% levels sooner or later. As per the management, they don’t hire when they don’t have projects, so hopefully these people will become billable soon.

It continues to remain cheap, so I intend to hold for another quarter or two since there aren’t many value buys available at this point.

Disc: Invested in all 3. No recent transactions in any of them. I am not a registered advisor and I write for clarity. Please do your own research

Sanghvi Movers (12-02-2024)

Wind installation picking up pace:

April- June : 1139;

April- July : 1306;

April- August : 1456;

April- September : 1551MW (monsoons)

April – October: 1659

April – November: 1930

April- December : 2103

April- Jan : 2336

Kiri Industries: Loan reduction and demand surge (12-02-2024)

Concall update

Oral judgement may come in a week. Written judgement may take time

Minimum 100 million dollar(820 crore) will be received by March 24, rest will come through auction

Subsidiary for receiving money for investment in Singapore

Kiri has signed MoU for green hydrogen with a German company , that is one sector kiri is looking forward to invest once the money is received