Article claims that L&T Defense would be third largest Defense company after HAL and BEL if it was listed independently. Has revenue of 3.5 thousand crore and order book of more than 12 thousand crores.

Posts tagged Value Pickr

Simple Investing (12-02-2024)

In this post, I will try to put together two interesting studies on portfolio construction and long term investing.

Study 1: Suppose I entirely focus on picking stocks that double in 3 years, how many such stocks will I require in my 10 stock portfolio to achieve portfolio IRR of 20% (Buffet standard) assuming I begin with equal allocation.

Below table gives the answer

Conclusion: It is ok to have a 50% error rate over a 20 year period while trying to pick “2x in 3 years” stocks. Still, one ends up with 20% IRR. Investing is a field that tolerates very high error rates if the horizon is long enough!

Study 2: What is the ideal size of a portfolio that allows a good error rate in picking stocks?

To answer this question, lets run the above table for 10, 15, 20, 25 stock portfolio sizes and compute how many “2x in 3 years” stocks are required to achieve portfolio IRR of 20% over various time frames. From the computed number, let’s compute the allowable error rate %. For example, in a 10 stock portfolio, if 9 stocks are required with “2x in 3 years” characteristics, then the tolerable error rate % is 10%, Below table shows the tolerable error rate for various portfolio sizes

Voila! there is hardly any variation in the tolerable error rate when the portfolio size is changed.

Conclusion: Do not overburden yourself by putting more number of stocks in the portfolio. Just try to minimize the error rate as per the above table. In fact, the more number of stocks you try to put in a portfolio, the higher chances of making mistakes and achieving poor hit rates of “2x in 3 years”. Over a 15-20 year time frame, if 50% of your portfolio is “2x in 3 years” stocks, you will hit 20% IRR over entire 15-20 year period.

Just buy high quality businesses at good valuations and sit tight. This is a statement seen at many places. Above explanation is numbers version of the same story. Only ask two questions while evaluating a stock. Is it a 2x in 3 years story or 10x in 10 years story. If the answer to any of them is yes, go ahead and buy at a reasonable valuation. Else, find another one.

PS: I have recently started to write a blog to keep journaling my learnings and analysis. It’s here.

You may not find anything substantial until few months, but my endeavour is to keep it up and running.

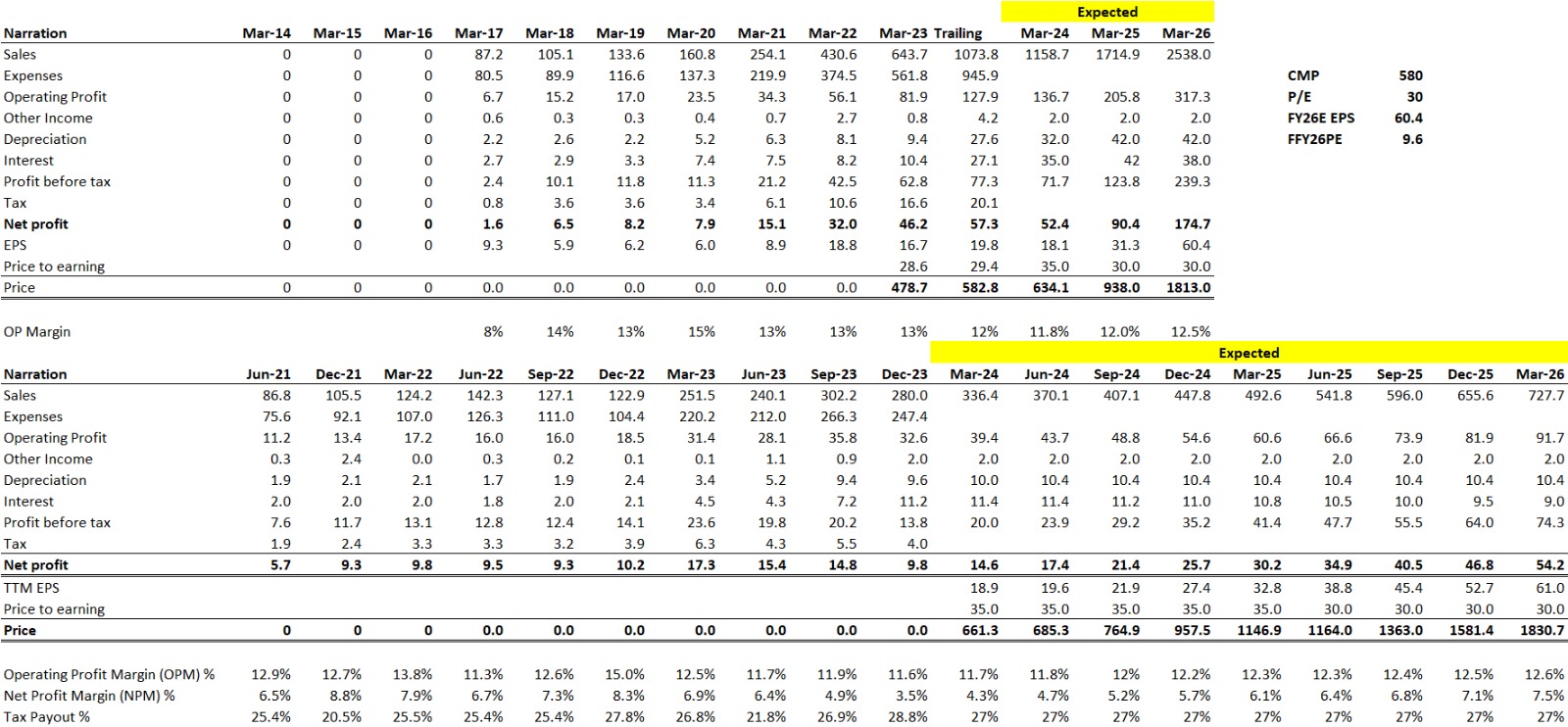

Hariom Pipes Ltd: A Capex Play! (12-02-2024)

Hariom Pipes

-Made a simple financial model as per guidance given by management

-I believe the next 2-3 Q more pain ahead on the Int & Dep side… after that Operating Lvg & Economies of scale will start to kick in… if CF improves

No Reco… posted just for educational purposes

Simple Investing (12-02-2024)

Hi @Investor_No_1… Any thoughts around HUL? Any specific reasons why you have not added it to your portfolio? Would you add at these levels, considering the long consolidation?

I try to do covered calls in large stocks and currently hold HUL and Marico from the FMCG pack. Marico gives a decent yield, HUL tends to be lower yield but I think it is at a good level and some more time correction will position it well for some consistent growth.

Mayur Uniquoters ~ Market Leader in Indian Synthetic Leather Market (11-02-2024)

Mayur reported another flattish quarter (flat sales and profits). They keep moving the goal post as it comes closer, now they are guiding for a step growth in FY26, while FY25 will also be a growth year. Concall notes below.

FY24Q3

-

PU sales : 2.07 lakh sq.m

-

PVC sales : 68.48 lakh sq.m (vs 70 lakh sq.m in Q2FY24)

-

Exports (53 cr.): export general (18 cr.), export auto OEM (35 cr.). Auto exports were impacted for 2 months due to strikes in Ford plant

-

Auto OEM: 42 cr., auto replacement: 38 cr., footwear: 34 cr., furnishing 5.60 cr.

-

BMW is still 4,000 m, expect ramp up from April 2024

-

Mercedes : 30’000 m/month

-

Used to supply 2.5 lakh m to Maruti which has reduced to 30,000 m as they only supply to their premium models which can give them higher margins

-

Will see growth in FY25 but big jump will happen in FY26

-

Have introduced a new product for marine market (exports) which they were working for 3 years

-

Zara had four visits to their Gwalior factory and Mayur is expecting orders in next 3-4 months

-

Retail furnishing : Sold 20,000 m last month. 500 dealers now and hope to add 500 more in next year

-

Have seen large number of PVC plants coming up (10-12 factories in Gujarat now vs 2 factories 5-years back). They install plants for 150 cr. Vs competitor plants of 20-25 cr.

Sorry I dont know. Manav had joined the co a few quarters back.

Disclosure: Invested (position size here, no transactions in last-30 days)

Mayur Uniquoters ~ Market Leader in Indian Synthetic Leather Market (11-02-2024)

Mayur reported another flattish quarter (flat sales and profits). They keep moving the goal post as it comes closer, now they are guiding for a step growth in FY26, while FY25 will also be a growth year. Concall notes below.

FY24Q3

-

PU sales : 2.07 lakh sq.m

-

PVC sales : 68.48 lakh sq.m (vs 70 lakh sq.m in Q2FY24)

-

Exports (53 cr.): export general (18 cr.), export auto OEM (35 cr.). Auto exports were impacted for 2 months due to strikes in Ford plant

-

Auto OEM: 42 cr., auto replacement: 38 cr., footwear: 34 cr., furnishing 5.60 cr.

-

BMW is still 4,000 m, expect ramp up from April 2024

-

Mercedes : 30’000 m/month

-

Used to supply 2.5 lakh m to Maruti which has reduced to 30,000 m as they only supply to their premium models which can give them higher margins

-

Will see growth in FY25 but big jump will happen in FY26

-

Have introduced a new product for marine market (exports) which they were working for 3 years

-

Zara had four visits to their Gwalior factory and Mayur is expecting orders in next 3-4 months

-

Retail furnishing : Sold 20,000 m last month. 500 dealers now and hope to add 500 more in next year

-

Have seen large number of PVC plants coming up (10-12 factories in Gujarat now vs 2 factories 5-years back). They install plants for 150 cr. Vs competitor plants of 20-25 cr.

Sorry I dont know. Manav had joined the co a few quarters back.

Disclosure: Invested (position size here, no transactions in last-30 days)

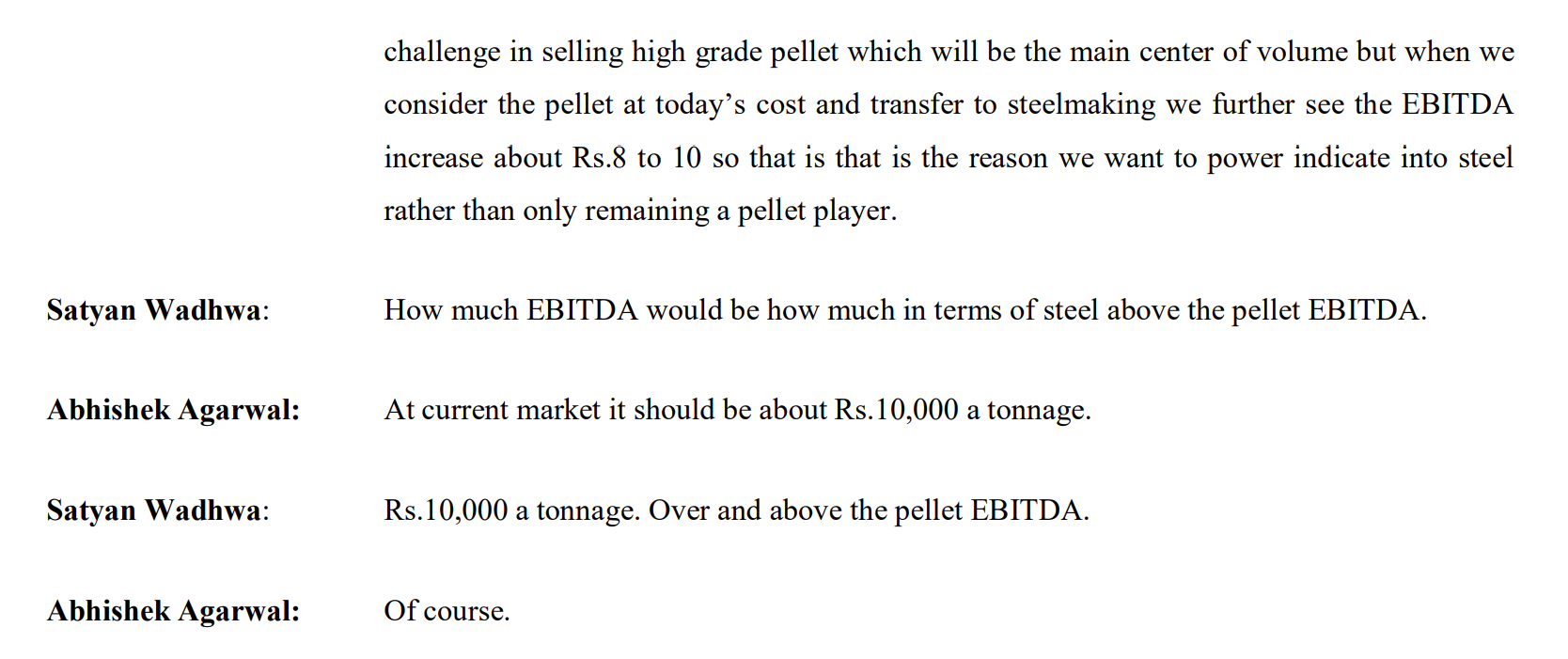

Godawari Power – Any Trackers? (11-02-2024)

I guess Peak EBITDA could be more higher, as per concall they would be having EBITDA of 10,000 rs over and obove pellet EBITDA, Pellets EBITDA is nearly 4,000 rs

So EBITDA from steel could be nearly14,000 Rs

Assuming peak utilisation of 90% capex can add near to 2500 crores

@Worldlywiseinvestors any idea on hum much time they will take to reach peak utilisation for this integrated steel plant?

Godawari Power – Any Trackers? (11-02-2024)

I guess Peak EBITDA could be more higher, as per concall they would be having EBITDA of 10,000 rs over and obove pellet EBITDA, Pellets EBITDA is nearly 4,000 rs

So EBITDA from steel could be nearly14,000 Rs

Assuming peak utilisation of 90% capex can add near to 2500 crores

@Worldlywiseinvestors any idea on hum much time they will take to reach peak utilisation for this integrated steel plant?

Five Star Business Finance – Financing Bharat! (11-02-2024)

Very good pointers. Thank you!!

Five Star Business Finance – Financing Bharat! (11-02-2024)

Very good pointers. Thank you!!