ADSL have recently appointed Mr. Ramanan Ramnathan, a veteran in the industry. He was instrumental to turned around CMC, part of TCS. He will be helping on driving sales and strategy (improving compliance).

Posts tagged Value Pickr

Anuh pharma ltd (11-02-2024)

I have been a long time holder in this stock and will vouch that the promoters are only interested in making a fortune for their close family members …every 5 years they give bonus but other than that they have too much value unlocking possible but are reluctant to do that since they want to play under the hood. Many representations were sent to get themselves listed on NSE but they were least bothered.

Anuh pharma ltd (11-02-2024)

I have been a long time holder in this stock and will vouch that the promoters are only interested in making a fortune for their close family members …every 5 years they give bonus but other than that they have too much value unlocking possible but are reluctant to do that since they want to play under the hood. Many representations were sent to get themselves listed on NSE but they were least bothered.

Zomato – Should you order? (11-02-2024)

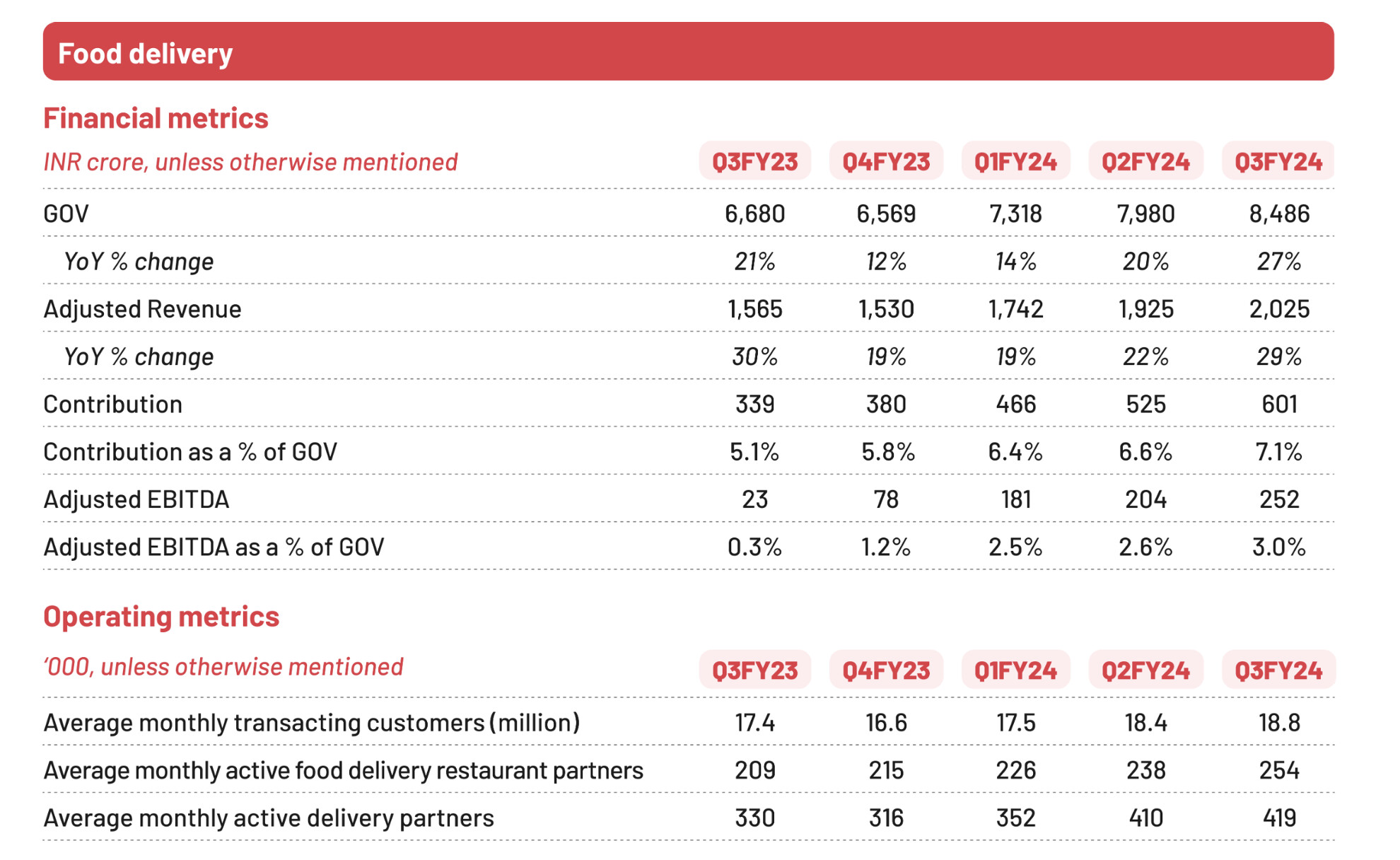

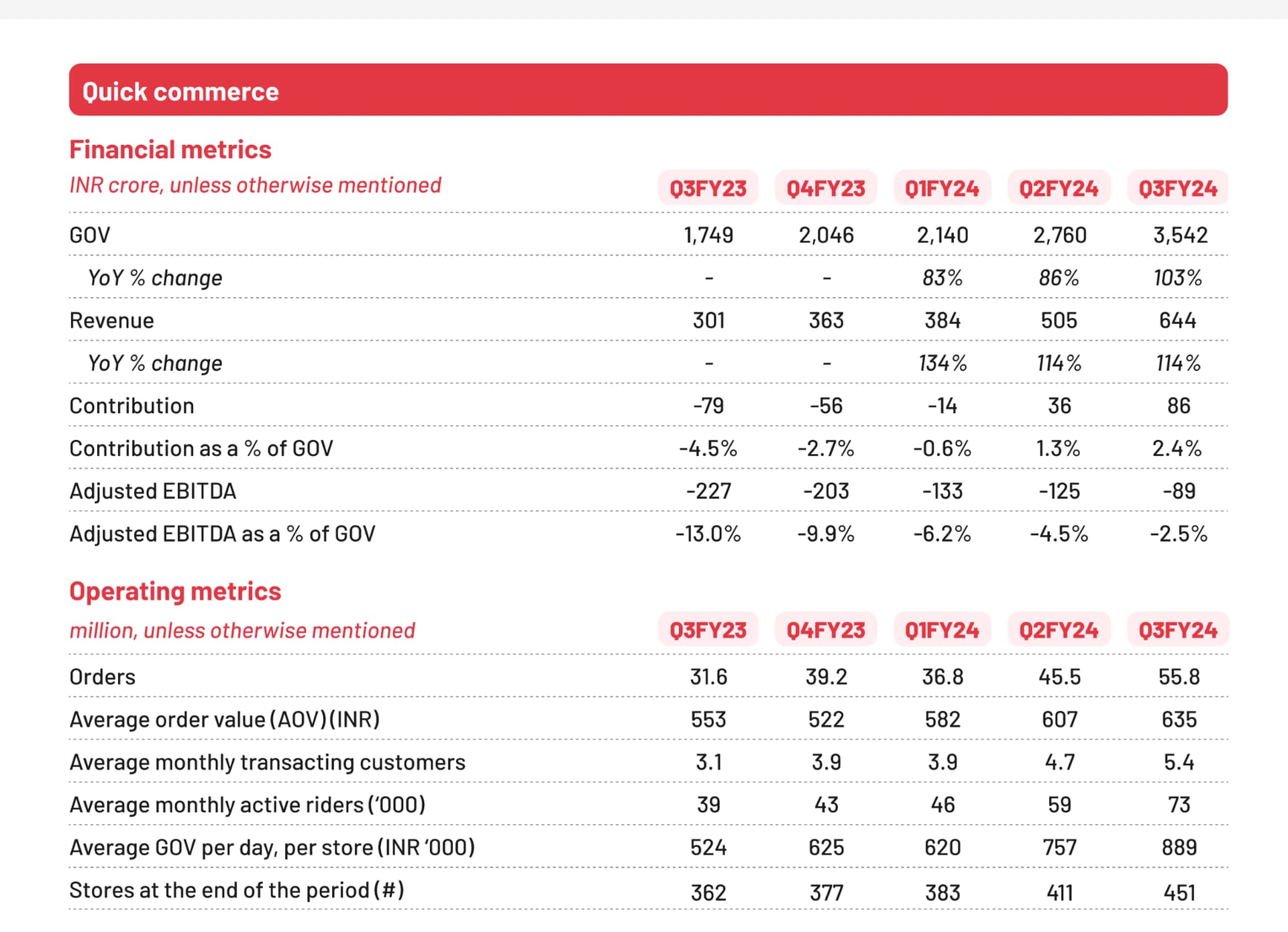

Notes from Q3FY24 deck –

- GOV across B2C businesses grew 47% YoY (13%QoQ) to 12886 Cr.

- Food delivery GoV grew 27% YoY while Blinkit GoV grew 103%

- Expect Food delivery GoV to grow 20%+ from here on. On Blinkit, Adjusted EBITDA breakeven may happen on or before Q1FY25

- Demand environment in discretionary consumption was muted and hence Food delivery GoV growth of 27% was below Zomato’s expectations but still higher than most of restaurants in the space

- Food delivery growth is there because it is still under served from supply standpoint. The monthly active user base has grown 20% YoY and also new restaurants have come under coverage

- Zomato Gold is still in testing phase and is being used to acquire/re-acquire customers. Customers switch between loyalty programs of Swiggy and Zomato based on who is offering lower pricing

- Despite drop in Zomato Gold pricing, contribution margin rose to 7.1%. This was because of increased ad-monetization which is leading to increase in ad revenue per order. Introduction of platform fee has also helped in margin improvement

- Blinkit GoV growth of 103% YoY was driven by –

- Robust uptick in demand due to festivals and occasions in quarter (77% increase in no. of orders)

- Less stock outs and adequate delivery partner availability were ensured

- While most of GoV growth was order volume led, it was also led by higher AoV as Blinkit has added higher ASP categories like electronics, festive needs, home decor etc. (15% increase in AoV)

- Also added 40 net new stores this quarter, taking store count to 451 (~10% increase)

- Despite increase in store count, average GoV per store per day grew 17% reflecting healthy SSSG growth

- 90% of GoV in Blinkit comes from top 8 cities so the growth there has to be high to maintain high GoV growth. While Overall business GoV grew 28% QoQ, top 8 cities grew 26% QoQ

- Close to 70% of stores in Blinkit are CM positive and 20% are above 5% CM and hence growing pool of contribution profit is making them to add new stores while maintaining expansion in CM margins

- In Q4FY23 it used to take 5.8 months for a store to do 1000 orders per day, now it takes 2 months as there is stronger product market fit in the business. This has led to faster breakeven

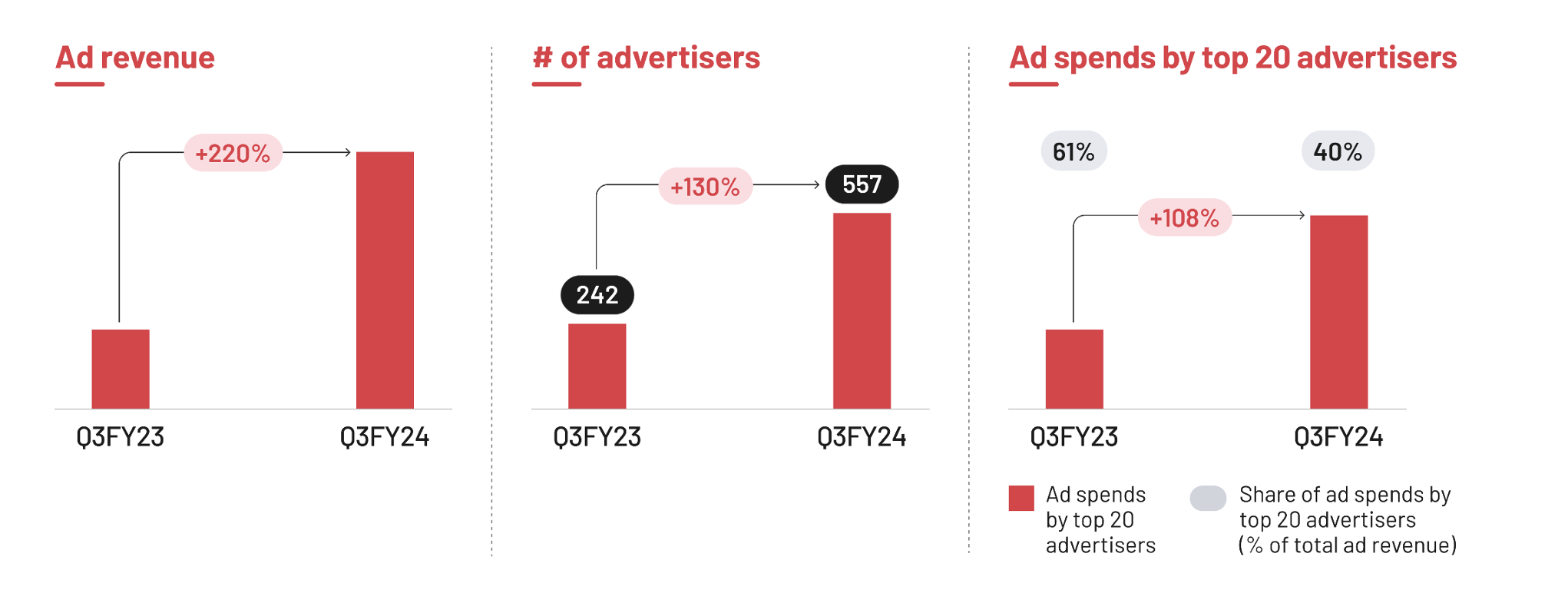

- Ad spends on Blinkit have grown 220% YoY vs GoV growth of 103%. This is because brands get higher RoI on ad spends on Blinkit and hence they are spending more here.

Zomato – Should you order? (11-02-2024)

Notes from Q3FY24 deck –

- GOV across B2C businesses grew 47% YoY (13%QoQ) to 12886 Cr.

- Food delivery GoV grew 27% YoY while Blinkit GoV grew 103%

- Expect Food delivery GoV to grow 20%+ from here on. On Blinkit, Adjusted EBITDA breakeven may happen on or before Q1FY25

- Demand environment in discretionary consumption was muted and hence Food delivery GoV growth of 27% was below Zomato’s expectations but still higher than most of restaurants in the space

- Food delivery growth is there because it is still under served from supply standpoint. The monthly active user base has grown 20% YoY and also new restaurants have come under coverage

- Zomato Gold is still in testing phase and is being used to acquire/re-acquire customers. Customers switch between loyalty programs of Swiggy and Zomato based on who is offering lower pricing

- Despite drop in Zomato Gold pricing, contribution margin rose to 7.1%. This was because of increased ad-monetization which is leading to increase in ad revenue per order. Introduction of platform fee has also helped in margin improvement

- Blinkit GoV growth of 103% YoY was driven by –

- Robust uptick in demand due to festivals and occasions in quarter (77% increase in no. of orders)

- Less stock outs and adequate delivery partner availability were ensured

- While most of GoV growth was order volume led, it was also led by higher AoV as Blinkit has added higher ASP categories like electronics, festive needs, home decor etc. (15% increase in AoV)

- Also added 40 net new stores this quarter, taking store count to 451 (~10% increase)

- Despite increase in store count, average GoV per store per day grew 17% reflecting healthy SSSG growth

- 90% of GoV in Blinkit comes from top 8 cities so the growth there has to be high to maintain high GoV growth. While Overall business GoV grew 28% QoQ, top 8 cities grew 26% QoQ

- Close to 70% of stores in Blinkit are CM positive and 20% are above 5% CM and hence growing pool of contribution profit is making them to add new stores while maintaining expansion in CM margins

- In Q4FY23 it used to take 5.8 months for a store to do 1000 orders per day, now it takes 2 months as there is stronger product market fit in the business. This has led to faster breakeven

- Ad spends on Blinkit have grown 220% YoY vs GoV growth of 103%. This is because brands get higher RoI on ad spends on Blinkit and hence they are spending more here.

Jitendra portfolio review (11-02-2024)

Dear experts. Please review my portfolio. I was investing “too diversified” (think over 50 shares). I sold it entirely and started from clean slate from Nov 2023.

Following is my current portfolio:

Name, Avg buy price, portfolio allocation %

Pennar Industries, 110, 21%

Capacite Infra, 269, 18%

Transformers India, 189, 8%

HBL Power, 321, 8%

Elecon engg, 907, 7%

ACE, 847, 6%

Ador Welding, 1500, 5%

KSolves, 1079, 4.5%

Shivalik Bimetal, 530, 4%

Usha Martin, 321, 4%

REST allocation to stocks for swing trading.

Please review and let me know how do you see this portfolio for long term horizon (2+ years)

Jitendra portfolio review (11-02-2024)

Dear experts. Please review my portfolio. I was investing “too diversified” (think over 50 shares). I sold it entirely and started from clean slate from Nov 2023.

Following is my current portfolio:

Name, Avg buy price, portfolio allocation %

Pennar Industries, 110, 21%

Capacite Infra, 269, 18%

Transformers India, 189, 8%

HBL Power, 321, 8%

Elecon engg, 907, 7%

ACE, 847, 6%

Ador Welding, 1500, 5%

KSolves, 1079, 4.5%

Shivalik Bimetal, 530, 4%

Usha Martin, 321, 4%

REST allocation to stocks for swing trading.

Please review and let me know how do you see this portfolio for long term horizon (2+ years)

Rategain – Fast Growing SaaS Leader (11-02-2024)

@pranshukh

Company has small equity of 11 cr and have cash in bank of 1000-1020 cr. with zero debt, drag down ROE and ROCE.

Rategain – Fast Growing SaaS Leader (11-02-2024)

@pranshukh

Company has small equity of 11 cr and have cash in bank of 1000-1020 cr. with zero debt, drag down ROE and ROCE.

INOX Wind (11-02-2024)

It is kind of a puzzler. Even DII FII stake has been increasing in Inox wind but not IWEL. The only explanation seems like IWEL having less liquidity. So while a fund can accumulate slowly, they sure can’t exit in a panic.

Disc: Holding IWEL.