Thanks for your response.

Posts tagged Value Pickr

Chirag’s Portfolio (11-02-2024)

Hey Chirag, Thanks for mentioning me.

→ I don’t know your risk appetite or thesis through which you have’t laid out here anywhere

→ I’ll answer to the best of my knowledge except for few large cap gaints since for such business there are too many moving needles that can affect stock prices and i’m not good at understanding macros

Affle → The co. has niche in Ads all though valuations on absolute term are high but the valuation still remain in Median range. IMO the co. should keep growing at 15-20% CAGR at base level for next 4-5 Years once can do the math for the same

the terminal value will be high considering the business is differentiated from normal IT Service provider

ASRL → No idea

HDFC bank → Taking a contrarian view when everybody is hang up on PSU, I think HDFC and Kotak is a Bargain now. At base level if i consider HDFC’s Current valuation as the New Normal then too 1500 Branches added will give operating leverage in next 3-4 years. The same was the case with Equitas Small finance bank earlier

HPAL → no Idea

Indigo Paints → I have been away from Paints due to the fact that there is so much competition coming in. The Pie will be distributed in so many pieces and who’ll get the biggest pie is still unknown.

INFY → Too many moving cards

JIOFIN → Bet on the management seems to be the reason. I’ll see 3-4 years down the line how the things pan out for it. but since you have got the same in demerger the cost of the same is more or less 0

JUBILIANTGREA → No idea

Kotak Bank → Stated Above

Misthtaan → No Idea

Nazara → No Idea

Polycab → Too expensive for my cup of tea

SBI Card → interesting business, imo there will be 1 Winner for sure in this cards mega trend but not sure weather the same will be SBI card of others

Star Health → Out of circle of competence

TCI EXP → A good business

Ultratech → I’m more baised towards JK laxmi

WIPRO → Too many needle

Polyplex → can’t share my view due to personal reasons

Over all my thoughts

You seem to have accumalated the business

- at very high valuation. some how you started at peak of the market (2021) and still your cost is at peak. I sense FOMO

- Too many business → I prefer to track <10-15 business not more than that and from that 10-15, 6-7becomes the part of portfolio

- My sense is that you MAY not beat Index too. Because if youu don’t know what you’re buying how will you beat the market?

that’s my view.

If you want to discuss any further Reach out to me in DM i’ll be more than happy to connect.

The harsh portfolio! (11-02-2024)

I appreciate the response.

Chirag’s Portfolio (11-02-2024)

Hi Chirag, Please don’t take “Junk” as offensive, for me Junk are even good companies trading at exorbitant valuations, volatile margins, drop is sales is most dangerous.

Polyplex margins are volatile, sales have dropped, its a dull business which is good however need to dig into further if valuations are good.

SBI cards looks expensive to me, stand alone card business will never get fancy, last 4 year performance is pathetic, NPA issues are most severe in credit card due to unsecured nature. IDFC offers revolving credit at much lesser rate.

Tanla looks promising.

Affle and rategain are in expensive category, new investment is not warranted, dont confuse with Industry PE, PE for bull market and bear markets are different, a 80 PE valuation will be justified in a roaring bull market and for same business even 40 PE valuations will look expensive:joy:![]()

![]() , just see chart of Dmart.

, just see chart of Dmart.

I will advise to play caution. Better to be in cash 50%. All market is heated up, look at stock level, dig deep and than take a call. End of day, capital preservation is most important all the time

PSU banks are cheaper than Pvt banks , corporate governance concerns are over as Modi will return to power. Also due to lesser fiscal deficit, they will enjoy large margins as cost of fund will go down.

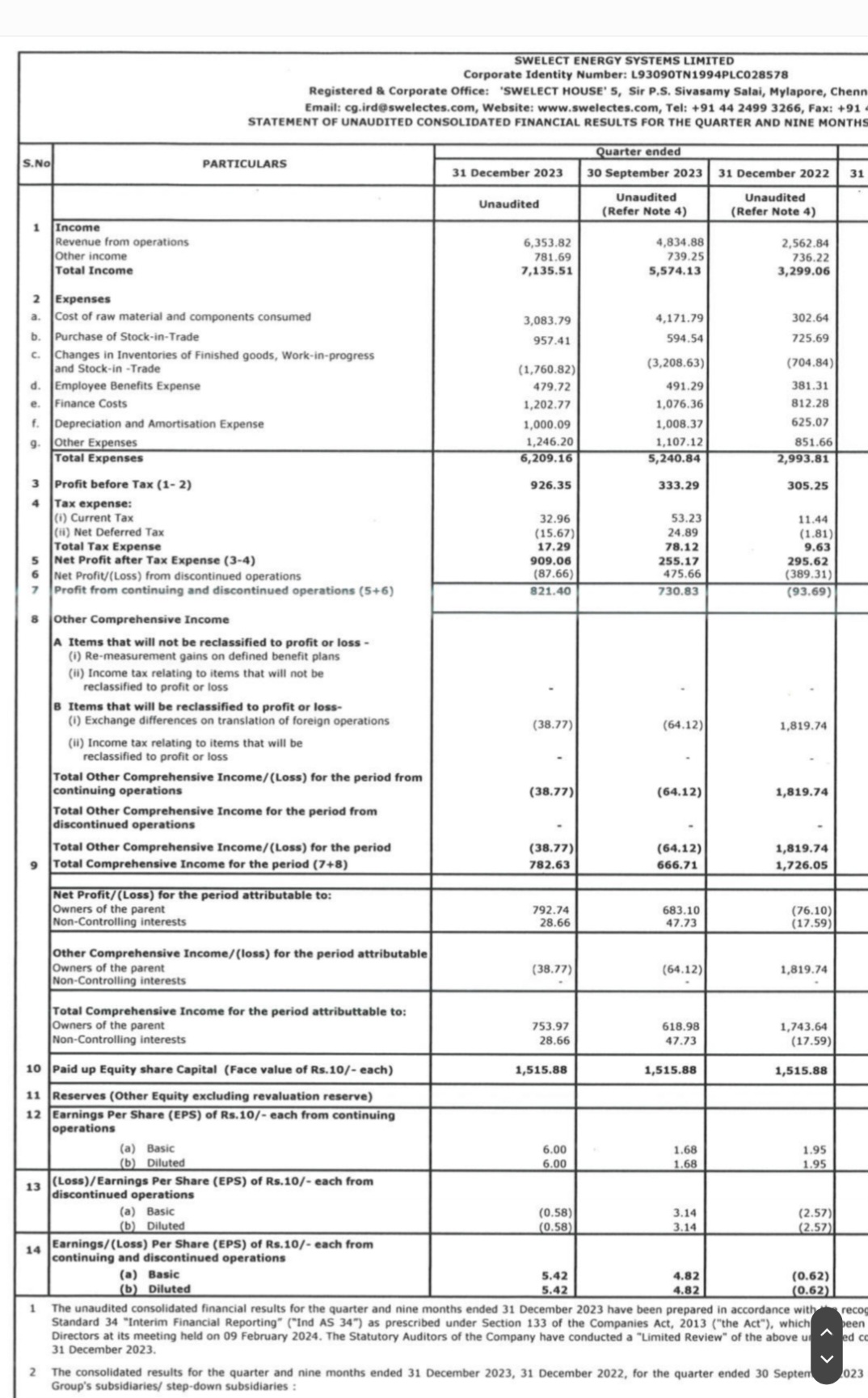

SWELECT ENERGY SYSTEMS LTD – some information from Annual report (11-02-2024)

Good result by Swelect energy

500 MW plant is slowly but surely showing in the results

With Goverment’s Push on Rooftop solar scheme, I am expecting an uptick in the topline going forward.

Disc: Invested, biased views

Centrum Capital (11-02-2024)

What about other subsidiaries like wealth and broking? They are still loss making. Housing and bank are doing well.

SKM Egg Products – thinking out of the shell (11-02-2024)

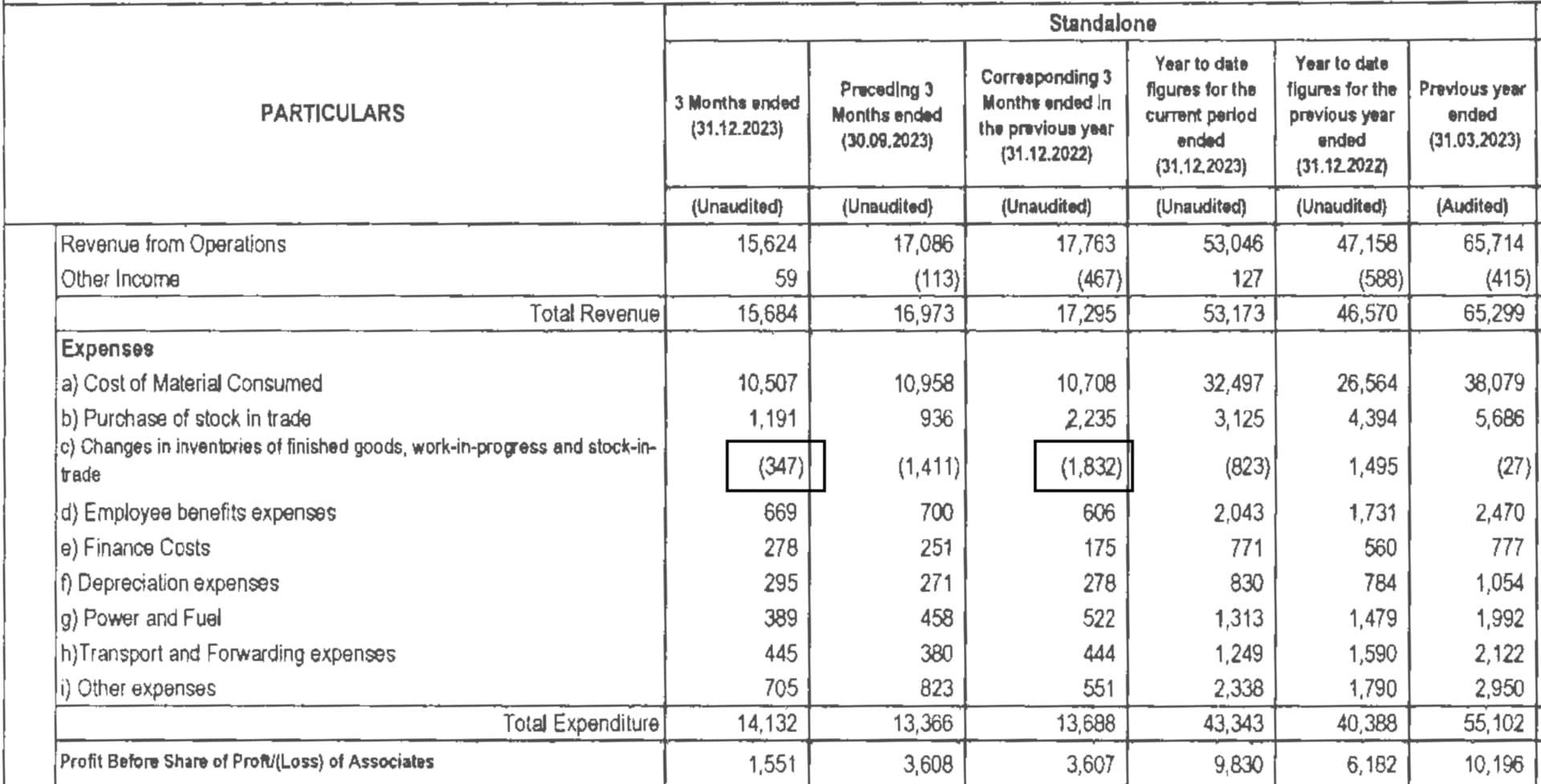

Results – Q3 FY’24

Summary:

Revenue – Rs 153 Cr

Net profit – Rs 12 Cr

OPM – 13%

Overall, the results are disappointing to most. The stock has already corrected 20% after the results came out. But this post will try and dig a bit deeper. With the limited knowledge we have about the breakdown, let’s try and look between the lines.

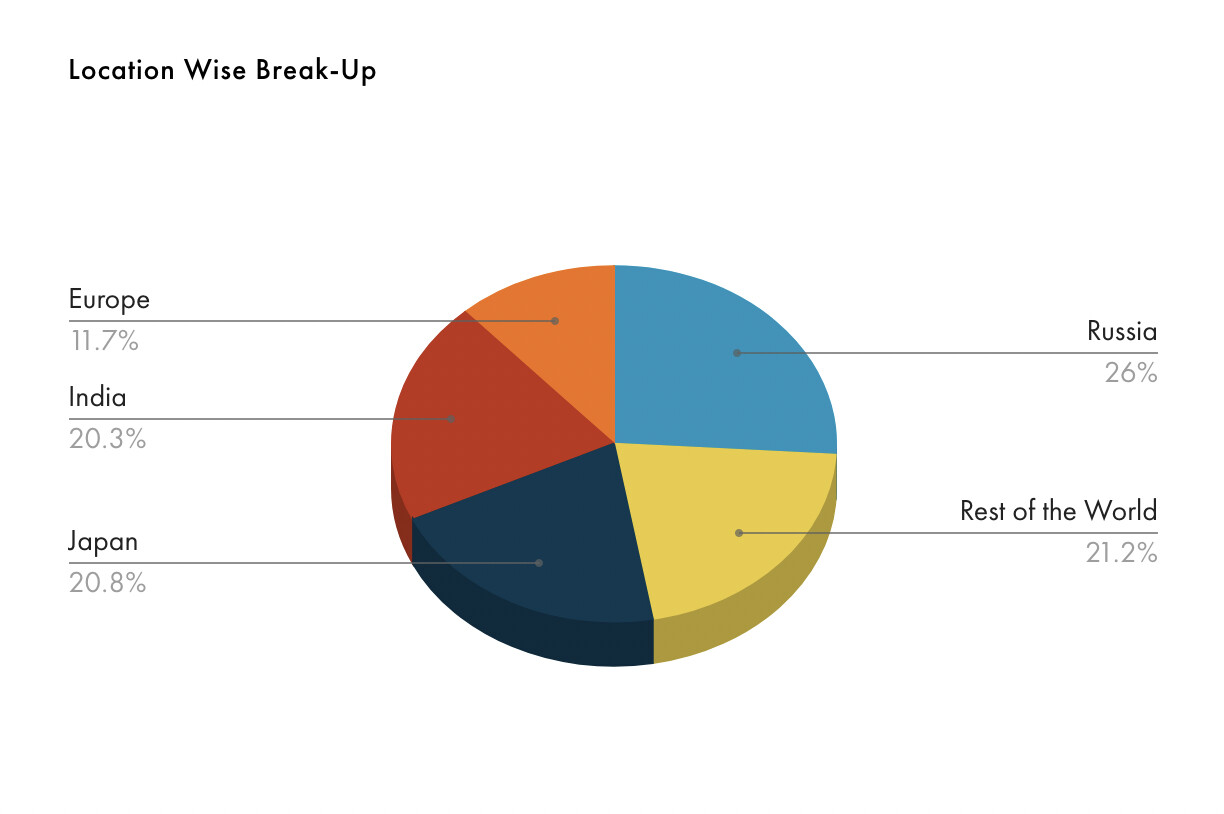

Let’s start with the geographical split:

Russia is their biggest importer. Followed by Japan and the domestic market in India.

What’s happening in Russia?

The egg prices are sky high. Egg farmers claim that the industry is in “a perfect storm” with prices soaring to over 40% this year.

Russian egg imports will be exempt from the import duty for the first 6 months of 2024, the economy development ministry has decided. Authorities expect that imports from ‘friendly’ countries could help return the balance to the market. The price hike has happened due to a perfect storm in the Russian egg industry, Leonid Kkolod, an independent agricultural analyst, told the local press. Over the past 2 years, Russian egg farms have been silently suffering having to maintain operations with ‘negative profitability’. Among the reasons that pushed the profitability into the red zone, tough import dependence is the first to blame.

Source: poultryworld

Is the situation going to change? Yes! It looks like the the demand for eggs in Russia will primarily be met by India. More specifically, we also need to look into Egg powder imports. Are they going to increase as well?

Russia would commence the import of egg powder from India about a month from now (or perhaps sooner), owing to the increase in the demand for it. Rosselkhoznadzor, Russia’s agricultural watchdog, confirmed the development. The Russian media has, in fact, criticised the decision to open the market to Indian imports, stating that the local makers wouldn’t be able to compete with Indian prices and could be wiped out. Nevertheless, Rosselkhoznador has decided to go ahead with it.

Similarly, Japan’s primary egg exporter is also India, and their economy is also recovering with their stock market hitting a 34-year high. This is all positive news for Indian exporters.

Domestic demand for egg powder:

The Indian Egg powder market is forecasted to grow at a 7.1% CAGR through to 2029. Again, egg prices have risen sharply in India. I’m from Bangalore and an egg cost me Rs 6.5 from my local grocery shop. A sharp rise in egg prices is seen in the country due to the decline in production. Good export demand is aiding the uptrend in price, which producers said is likely to hold on to current levels till February.

So what is SKM doing with all this demand?

Stocking up inventory! The advantage about egg powder, unlike eggs, is its longer shelf life. SKM’s recent results clearly points to the fact that the drop in OPM% margins is primarily due to stocking up of inventory:

The expense related to changes in inventories of finished goods increased from -18.3Cr from last year to -3.47Cr this year. This suggests that the company is investing more in its inventory of finished goods during the current quarter compared to the same period last year. Meaning the value of the inventory is going up. Again, I’m not a financial expert and would like it if someone can analyze it further for me. So that explains the drop in OPM% and net profits.

Please do share your thoughts ![]()

How to take leverage to go long in market (~2 years)? (11-02-2024)

Hi. Please share the source for this. I did my research and did not find any such restriction.

Sandhar Technologies – An emerging market leader (11-02-2024)

Hi @joinjp2003, what are your thoughts on the cyclicality of this business and customer concentration risk? Also the Management expected higher growth but it wasn’t achieved (I think it 20% actual vs 25-30% which they said).

I have been following this company and built some position recently. Read your comments here and it re-enforced my confidence ![]()

I happened to have worked with the Company on an acquisition they eventually didn’t go through with. But the Management is quite aggressive in their projections and Mr. Dawar is a nice man to talk to!

Malhar’s Investing Thoughts (11-02-2024)

One of the study projects I’m doing is what influences which sectors and themes drive a bull market. Recently, defence, railways, EVs, engineering/manufacturing and PSUs have been the leaders.

In the 2010-2018 cycle it was NBFCs and high RoCE asset-light consumer companies.

The 2003-08 cycle was led by real estate, infrastructure, metals etc.

I am trying to understand: what factors drive this?

Some of my hypotheses include:

- Capital cycle of that sector

- Government policy push

- Starting/initial valuations

Thoughts invited.