Any update on court roceedings? Friday wad supposed to be the latest hearing

Posts tagged Value Pickr

Momentum Portfolio-TechnoFunda Picks (10-02-2024)

Any updates on portfolio? Which stocks are you tracking currently?

Accent Microcell Limited – A Niche Microcap with some puddles (10-02-2024)

Incorporated in Ahmedabad on April 10, 2012 Accent microcell limited is into manufacturing of a excipient named MCC à Microcrystalline cellulose

It’s one of the most used excipient in pharma value chain. MCC market is valued at $411 Million (around 2800 Crores) and is projected to reach $712.9 Million

Source – RHP

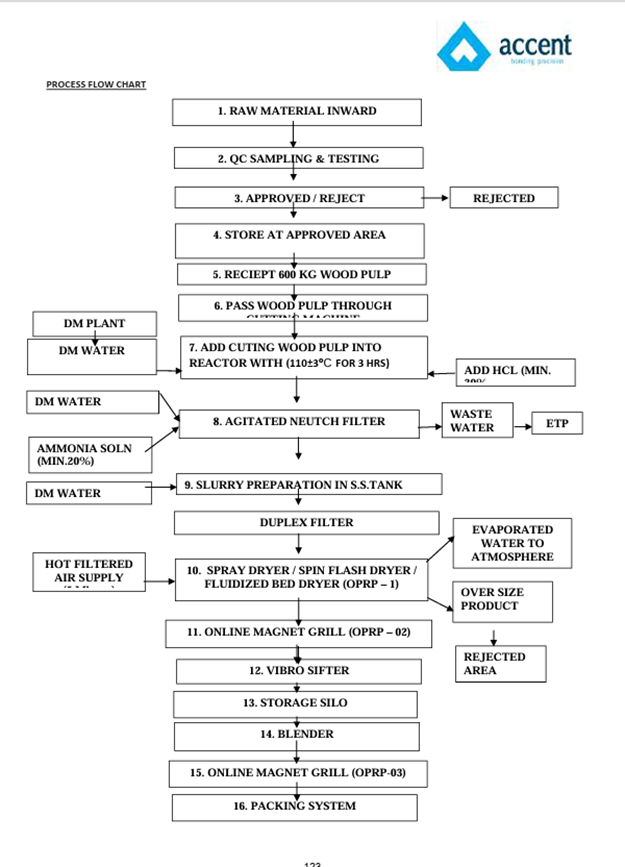

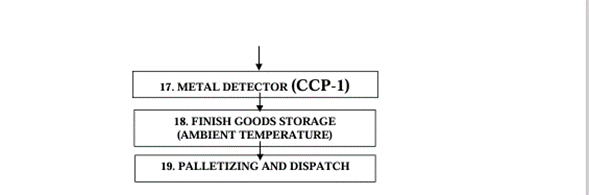

Process of manufacturing – Cellulose obtained from Wood pulp is mixed with Hydrochloric acid and mix it up and heated @105C for 15 minutes

The cellulose obtained is known as depolymerized cellulose and this Depolymerized Cellulose is Known As MCC

Value chain given in RHP

Where is MCC used in ? → in wide range of application such as pharma, textile, packaged food for anti-caking, etc. for Accent max contribution arises on account of Pharmaceutical business → 72%

If you have followed my Yasho thread (the co. has very minute division of B2C where co. manufactures the Anti-oxidant, for formulation of such anti oxidants carrier or filler is required à carrier – Helps API to reach to target site in formulation and Filler à helps in bulking the weight

Some of the competitor are

Dupont de Nemours, Inc.

Asahi Kasei Corporation

Sigachi Industries Limited

Accent Microcell Pvt. Ltd. (red flag)

DFE Pharma GmbH & Co.KG

Since the MCC market is very very tiny 2800 crores globally the exports are to facilitated in order to Ensure revenue growth → Domestic market will be sub 700 crores at max.

The major grades of MCC manufactured and marketed by Company are branded under the name “accel”. Besides “accel” they sell products under the name “acrocell”, “maccel” and “Vincel”.

The company has 2 manufacturing unit → @ Dahej and Pirana à both are running at optimum capacity @100% and 95% respectively

The company IPOed recently and there was no OFS the whole issue was Fresh infusion

Purpose of the IPO was to Install the capacity for Croscarmellose Sodium (“CCS”), Sodium Starch Glycolate and Carboxymethylcellulose (CMC)

For the amount of 54.39 crores the commercial production for which will start from March 2025

Croscarmellose sodium is a super-disintegrant, which means it helps tablets break down quickly and completely when they come into contact with moisture in the gastrointestinal tract. This property is useful for improving the dissolution and absorption of active pharmaceutical ingredients (APIs) in tablets or capsules.

Hence for pharma co. both are a need however they don’t complement each other’s value chain hence we can safely say they are venturing in horizontal integration (expansion)

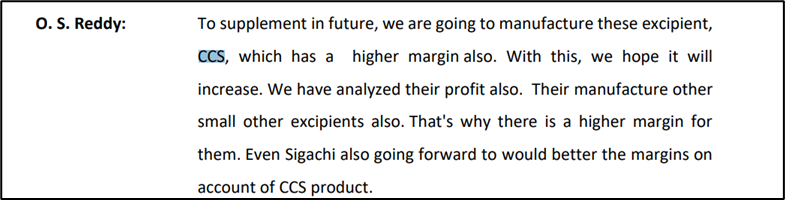

Now why does Croscarmellose Sodium (“CCS”) Excite me – See below SS

The CCS margins are more than 30% although the capacity for Accent is around 2400 out of 10,400 MT capacity but a start is a start

Market for CCS is almost 850 Million double of MCC market

The EBITDA margins for the company can be sub 24% once the capacity comes live

Considering that 70% of revenue is on account of pharma it’s not surprising that Gujarat is the major contributor of their revenue and for export it’s Brazil. Their MCC market and CCS market is Big

4 members of family are paid cross of 30 Lakhs which frankly is very nominal considering that annualised pat as per Sept result can be 28 crores

Certain Redflags:-

The IPO proceeds will be used in manufacturing the capacity – the land for which is procured from the Related party at 0.6 crores à possibility of Mark up pricing

“Independent contractors” from which the whole expansion project is to be facilitated are “Patels” only à the chances of being related party not recognised by the law is high though no proof

Source – RHP

The promoter is into the same business through Unlisted entity Accent Microcell Pvt. Ltd. (red flag) which is mentioned as competitor for MCC in RHP à what’s the need for the same?

Land In Dahej SEZ is on lease (ofc) risk of non renewal

The company is owned by Patel family average cost of acquisition is around 10 Rupees Source – RHP

Issued on preference basis to family members @50 Just before the IPO on August 2023

Disclaimer – Not invested

Portfolio tracker for moderatores, administrator and VPs of ValuePickr forum (10-02-2024)

Can we use this thread to link portfolios of moderatores, administrator and VPs of ValuePickr forum?

This will help to manage a mega-thread that has important portfolio links spread across ValuePickr forum.

Sharda Motors – Emission tailwinds or EV threat to exhaust systems? (10-02-2024)

Listened to the conf call.

Basically, the business is a high NFAT one (and being decently profitable) and therefore generates more cash than regular business can utilize. Thus, it is imperative that the management shows a sense of urgency to deploy this cash which seemed missing. The last few calls, the updates have been static on this front. Management wants to buy cheap, which is good, but waiting for it too long is also a cost which management doesn’t recognize.

Else, their response to every question was generally non-committal barring they will outgrow industry.

Investing Basics – Feel free to ask the most basic questions (10-02-2024)

Can someone tell do we track portfolios of VP, moderators of forum for learning purpose and understanding rationale when they enter or exit any stock?

Oracle Financial Services (10-02-2024)

Thats the problem. They do not have investor calls and no detailed documents either. I am not able to ascertain whether this revenue jump is one time or would it be a recurring revenue now.

How to take leverage to go long in market (~2 years)? (10-02-2024)

-

I got offering from ICICI bank and Kotak bank.

-

Process was entirely online. Took me 30 mins for KYC, 4hrs to get money online. Process charge 200 Rs.

-

Interest paid monthly

-

Interest charged from day loan is taken

-

Money can be used for any personal usage.

-

Loan can be closed instantly.

Annapurna Swadisht Ltd – A Swadisht FMCG investment? (10-02-2024)

It is just grammatically incorrect sentence. What they mean to say is that as a company majority of their operations and hence revenue is being driven by the North-East region of India, and they think that the profits are inadequate. The sentence should read:

“The company is regularly making profit. However, presently our volume of operations are limited to North East Indian States only. Because of the limited span of our operations, our profits seem inadequate.”

Point 2 suggests the measures that the company is taking to improve the span of their operations via geographical expansion and diversification, and, increase the utilization of their production facilities.

Point 3 is forward looking statement, which signifies that because of the steps mentioned in point 2, they are confident of posting better than previous fiscal’s results.

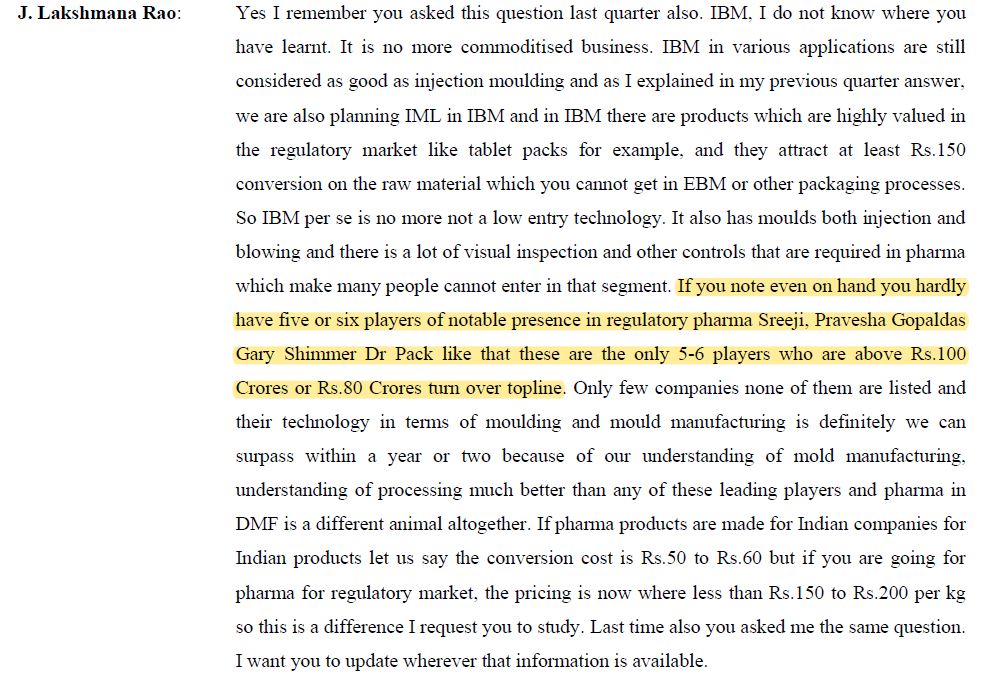

MOLD TEK PACKAGING—dividend plus growth (10-02-2024)

According to their Q1 & Q2 FY24 Concalls, their competitors to pharma packaging are Sreeji, Pravesha Gopaldas and DrPak. I have been tracking the company concalls for the last two quarters and I couldn’t find their competitors in the paints & lubes segments.