Is it true that dollar has never done a rights or bonus issue, and only one split of 1:5 in 2017?

Posts tagged Value Pickr

Campus Activewear – betting on the India Consumption Theme (10-02-2024)

Q3 fy 24 concall Note

Volume muted?

A: demand like entry segment is muted for all

Premium segment grew.

If premium grew, why it’s not reflecting in margin?

A: Is due to performance marketing and ad spends

Entry level is 20% now, earlier it was 35-36%.

Premium 45% now.

10% marketing is spend vs 5-7% in normal year. Spend level will be 6-6.5% in future.

Online is fattish, b to c ok. O 2 O takes time.

Other player doing margin 20% we are in 12%?

A: Increase in ad spend is the reason, that will normal soon

We have to spend extra to generate demand

Higher premium doesn’t necessary high margin.

Margin came down to 12 from 20-21. No guidance. But we are trying. Reduction on inventory days greatly

BIS: will restrict cheap import from china and Vietnam

Implemented from 1/1/2024

Local manufacturer will be benefited

Campus is the recipient of first BIS certificate. 100% compliant.

EBITDA margin long term long-term is aspiration is 20%.

Accenture is consulting partner

Online margin is higher than trade margin historically but situation is not stable.

Not major delta across the channel in future as we are putting efforts in performance marketing

Online was 38% last year.

Volume is flat but increase in other expenses?

A: Leasing, one of inventory, inflation and employee cost.

Current is tuff year for industries.

100 / year EBO is run rate and it will be continue same run rate.

Disc: Invested

Premco Global — Narrow Fabric (A critical component for inner wear) (10-02-2024)

Premco, poor results continues in the series for the company. Dividend declared for quarter also declined to Rs 2 per share during Q3FY24 as against Rs 6 per share declared in Q3FY23. The decline in dividend declared is major concern for me.

During the quarter. while consolidated profit declined by 53% yoy, standalone profit declined by more than 61%. So, India business continue to adversely affected. Even depreciation charge for quarter is almost same last year in standalone business, hence assume that company has not commericalised new plant. When the new capacity would be operational, the company performance is expected to remain lower than normal level of profitability due negative operating leverage.

Overall, no positive take away from the results in my view. Proftiablity in Vietnam and India under pressure, No update on capex commencement, Major drop in Dividend, No attempt from management for NSE listing. Critically evaluating my investment in company.

Disclosure: My view may be biased due to my investment in the company. I may increase/decrease/exit my holding in the company without informing forum. I am not SEBI registered advisor. I am not recommening any investment action in the company. Reader shall do his/her own due diligence/consult financial advisor before making any investment decision.

Page industries (10-02-2024)

Don’t know if it’s just me but Vedji Ticku used to communicate properly while VSG only says a few words about a specific question and starts to generalise about long term picture, robust growth etc

eCom growth was 39% for Q3 and 28% was for YTD

Page finally has good product range in Athleisure which is where bulk of the incremental growth is going to come. They had very few designs and product offering range itself was small pre-covid. They have worked hard to improve this but the pricing is a big hurdle they need to overcome. I am not sure how they can scale Athleisure if they continue with the existing prices, particularly outside of metro/t1 cities. 40-50% premium to competition is a bit too streched. There is a huge addressable market but I feel they are limiting themselves to targeting a tiny part of the population with the rigid pricing model.

There seems to be a lack of understanding by Page’s management about the market dynamics and how big of a tailwind apparel has in India given the increase in discretionary spends. Every person wants to “look” good, brand matters but not at a 50% markup unless you’re catering only to the luxury segment.

The power has shifted back to the retailer and consumers will prefer Zudio/Trends over legacy brands like Page because of the steep difference in price points. Zudio had 60% growth in apparel for the last two quarters. Brand loyalty has taken a hit with change in customer buying patterns.

Even after seeing such fantastic eCom growth, the management is still hell bent on not having a native application on either Android or ios. Significantly smaller brands who do 100-200 crore turnover have applications as people use their smartphones 4-6 hours a day and a lot of online shopping happens online via mobile but no… not Page! Abfrl has different applications for each of their big brands like Van Heusen, Louis Philippe, Peter England, Allen Solly etc…

Either the management is too late or they focus too much on ARS/logistics/distribution etc forgetting such trivial things. I still remember from the previous con calls in 2019-21 period on how Bharat Shah (ASK) was quizzing the management about below average marketing/reach. They have followed a similar trend in apparel too.

Disc – top-3 holding, made transactions in the last 30-days

How to take leverage to go long in market (~2 years)? (10-02-2024)

People interested to know – I got around 50% of money invested using loan against security (in my case mutual funds) at 9%. FYI.

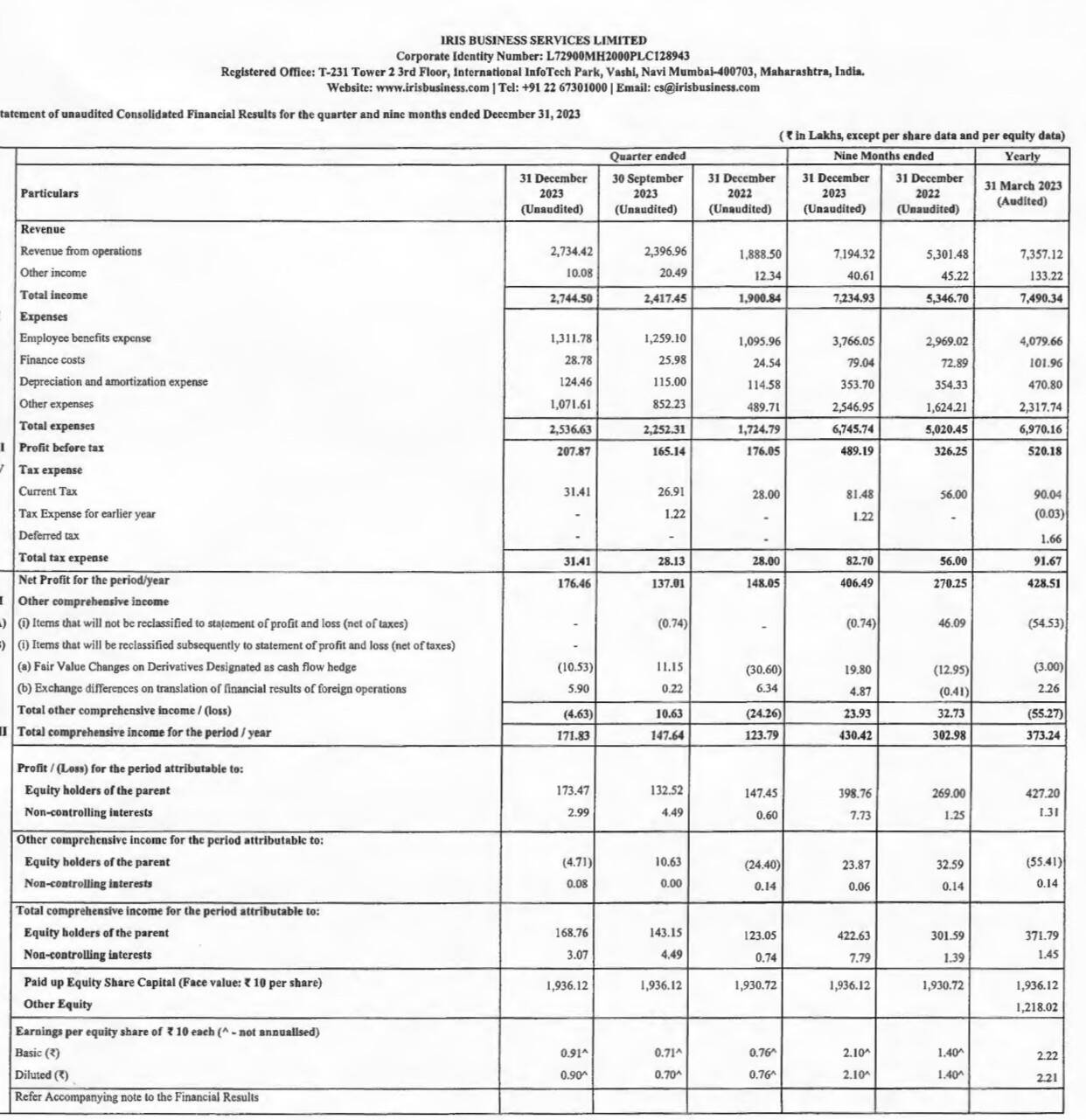

Iris Business Services – Emerging SAAS Microcap (10-02-2024)

Good results from Iris Business Services.

Consistent growth in revenues and profits

Sharda Motors – Emission tailwinds or EV threat to exhaust systems? (10-02-2024)

I listened to Sharda Motors q3 fy 24 concall. As usual it’s very difficult to expect easy to understand and forthcoming answers from management. Management is very conservative in answering questions in concalls. But whatever I gathered and deduced from concall is as follows…

Since past 2 quarters company has been benefitting from change in RDE emission norms for Passenger vehicles. The TREM emission norms have been pushed to fy 2027.

On being asked about the growth in company per quarter, management says a rough estimate can be made by looking at Gross profit gorwth. On calculating the gross profit, for which I used sales minus raw material numbers, I get figures of 139 , 131, 144, 137, 175, 172 ( all figures in crores) for last six quarters. It is a clear indication of benefits since past two quarters. On being asked how long this benefit can last, management was largely evasive.

The above issue came into play because the newer products sold do not account for Catalyst ( a part within the emission product chain) as it is not used in design of products for latest emission norms. And earlier too, Catalyst was only a pass through part for the company, not accounting for any margin. So minus the Catalyst, the sales amount shows decline but this calculation does not reflect the true picture.

e.g An emission product which earlier used to cost say Rs 120, ( with cost of catalyst being rs 20) will now cost 100 rs. If profit on each product remains same at rs 12, then earlier profit margin used to be 10% (12 % 120 multiplied by 100) but with the newer product (minus catalyst) margin is 12% ( 12 % 100 multipled by 100)

Near term growth tailwind is the new RDE norms based products. As the product matures its contribution to sales and margins improve. How long this lasts is anybody’s guess. Management is very reticent about this question.

The other growth driver is exports. China plus one factor is playing out better than expectations of the management. From the management answers, it appears that this could play out atleast partially in FY 25.

On use of net cash on balance sheet, management says primary focus is to go for a well thought out acquisition which could aid growth. Dividend distribution policy is spelled out which stipulates payment of anything from 10 to 30% of profits as dividend according to judgement of management. A couple of times mention was made as to provide shareholder returns and that something was being thought about it. ? Buybacks besides dividends. ? ( no clarity here)

On the information about land parcel in NCR region which everyone knows has appreciated a lot in recent times, there was no information about approximate value of the land being talked about.

All in all a concall which is reminiscent of most past concalls wherein while listening you try to grasp whatever you can and after listening when you think about take home message, it remains same as before. ![]() Nothing new.

Nothing new.

If anyone has better understanding of this company and concall, please put pen to paper and share details. I have put up whatever I have understood from a difficult to grasp concall.

INOX Wind (10-02-2024)

Thanks for the clarification. It is indeed for IGESL.

I missed to attend the earnings call, but had a second look at the slides. Honestly I don’t quite understand why they should add two slides in the middle, though related but of a separately listed entity.

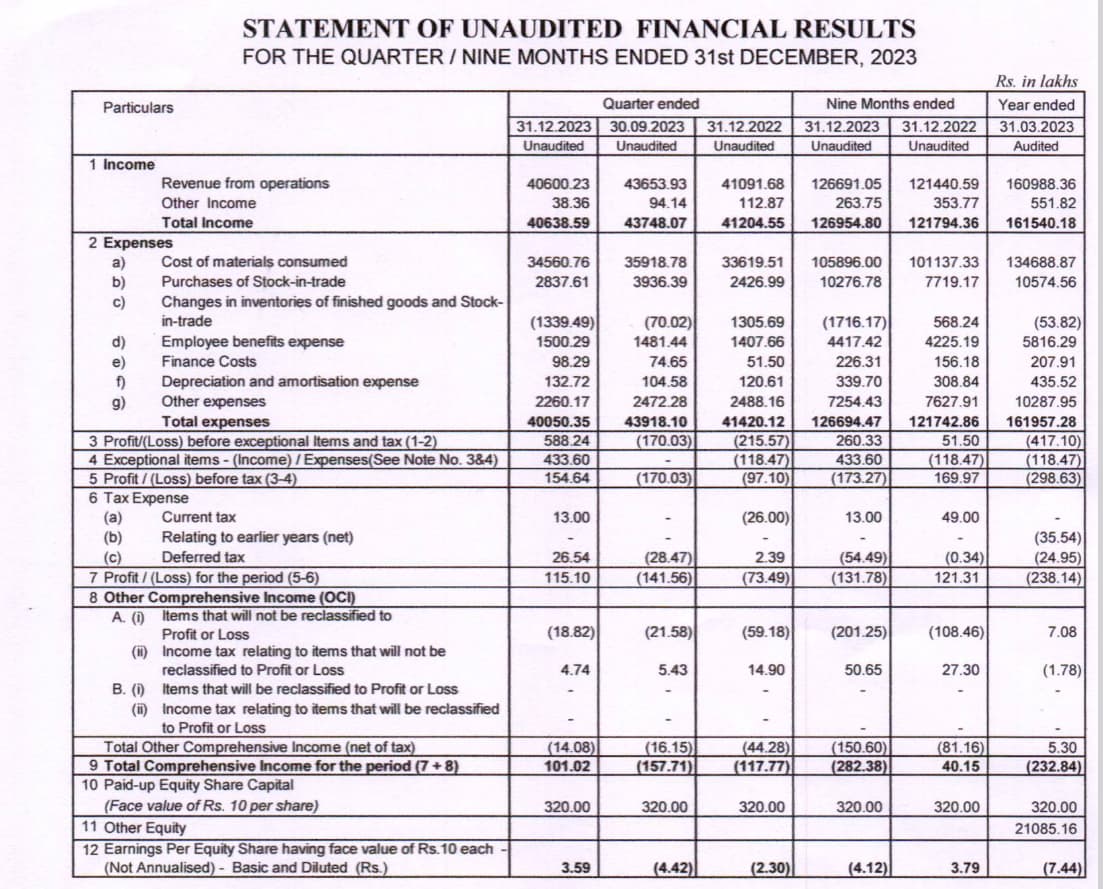

KSE Limited — Interesting Business (10-02-2024)

Decent numbers:

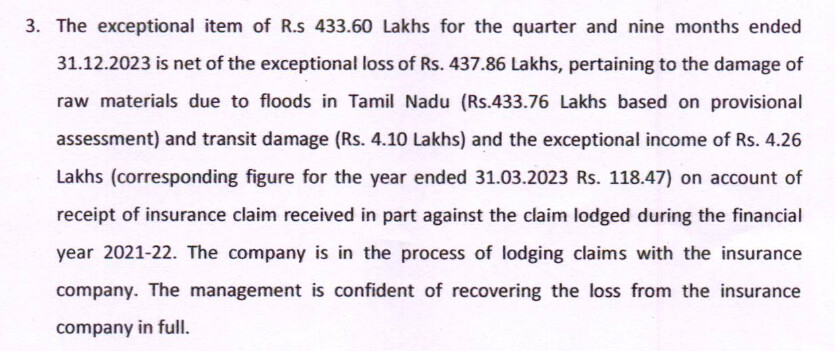

PAT would have look better if exceptional loss was not there due to floods in TN.

Everest Kanto Cylinders Ltd. – A long runway ahead! (10-02-2024)

I feel the results were excellent when compared to the previous few quarters

Revenue grew by 28% to 329 Cr YoY

EBITDA grew by 255% to 51 Cr

Margin at 15.6% vs 5.7%

Net Profit at 36 Cr vs -17 Cr loss