Q3 2024 result.

Posts tagged Value Pickr

Orchid Pharma Ltd (10-02-2024)

Conference Call Q3FY24

Steel Strips Wheels Limited – Attractive Valuations (10-02-2024)

Steel strip wheels –

Q3 FY 24 concall highlights –

Sales – 1110 vs 938 cr ( export sales @ 174 cr, up 180 pc from 60 cr )

EBITDA – 117 vs 108 cr ( margins @ 11 vs 12 pc, down 100 bps YoY )

PAT – 60 vs 44 cr ( due lower tax outgo )

Current manufacturing capacity –

Steel wheels – 20 million to go upto 27 million wef Jan- Feb 24

Alloy wheels – 3 million to go upto 4.8 million in a phased manner – capex is in progress

No of plants @ 5

Tata steel holds 6.9 pc stake in the company

Nippon Steel and Sumitomo Metals together hold 5.4 pc stake in the company

Mkt share in domestic mkts –

PV – 42 pc

MHCV – 61 pc

Tractor / OTR – 42 / 70 pc

2-3 wheelers – 30 pc

Export sales for first 9 months @ 505 cr, up 130 pc from 220 cr LY

Export destinations –

US – 70 pc

EU – 26 pc

RoW – 4 pc

Steel wheels demand expected to grow at 8 pc CAGR for next 5 yrs vs 12 pc for alloy wheels

Alloy wheel contribution –

By volume – 15 pc

By value – 28 pc

Some popular models getting their alloys exclusively from the company – Carnival, Salvia, Creta, Verna, Aura, XUV 700, Magnite, Punch, Tigor, Kiger. Company enjoys 50 pc share wrt Sonnet, Venue, Nexon

Company enjoys > 50 pc mkt share wrt EV models of Mahindra and Tata Motors

Company expects alloy wheels, steel wheels sales to grow at 20 pc, 4 pc CAGR for next 2 yrs

At present, the company is doing an EBITDA of Rs 256/wheel. As the contribution from alloy wheels increases, this EBITDA/wheel should only go up from here on

Expecting to clock 4800-5000 cr of topline in FY 25. This yr, company should do 4400-4500 cr on the topline

Company completed infusion of Rs 138 cr into AMW auto components ltd via NCLT process. AMW is also involved in the manufacturing of steel/alloy wheels

Low tax rate for Q3 due company shifting to newer tax regime. Henceforth – yearly tax rates to be at 25 pc/yr

Seeing some slowdown in exports due to the Red Sea issue. At present, company is at max doing Rs 50cr /month of exports ( ie wef Jan 24 )

Company to undertake debt reduction wef FY 25 as a lot of capex is behind them

Expect alloy wheel production at 3.5-3.6 million wheels for next FY

Disc: hold a tracking position, biased, not SEBI registered

Priti International Ltd (10-02-2024)

I am not sure about maintaining such margin. Its not clear why this margin improvement is happening? Is it export, higher negotiation power or something else. Lets be hopeful that red sea crisis gets resolved. Export brings higher margin. Plus margin contraction QoQ looks like the affect of export decline due to red sea crisis. My main focus is on Brand building. It is still based on one city and still unknown to majority.

Endurance Technologies – Quality focussed Auto component manufacturer (10-02-2024)

Great numbers reported by the company and good to see continued moderation of revenue concentration in both segment (2-wheeler) and client (Bajaj).

Anurag Jain is a very capable promoter and has done a great job in finding new growth engines for company and executive them very well.

Now that he is past 60, one thing that is still not clear about the company is succession planning. Any idea about that?

Smallcap momentum portfolio (10-02-2024)

Update for entry on 12th Feb 2024

Based on ranking

- BSE

- SUZLON

- NBCC

- BSOFT

- HUDCO

- MEDANTA

- MCX

- SJVN

- MRPL

- SWANENERGY

- OLECTRA

- COCHINSHIP

- KAYNES

- CHALET

- PCBL

- MOTILALOFS

- IRB

- ITI

- IRCON

- SOBHA

Based on A → Z for easy tracking

- BSE

- BSOFT

- CHALET

- COCHINSHIP

- HUDCO

- IRB*

- IRCON

- ITI

- KAYNES

- MCX*

- MEDANTA

- MOTILALOFS*

- MRPL

- NBCC

- OLECTRA*

- PCBL

- SJVN

- SOBHA

- SUZLON

- SWANENERGY

Entry

MCX makes an entry

IRB, MOTILALOFS and OLECTRA cannot enter as there is no vacancy.

Exit:

SHYAMMETL exits

KALYANKJIL, NLCINDIA and WELCORP stay within the top 25 and hence remain.

Zensar technologies (10-02-2024)

Sales growth has been muted for all the IT companies but that doesn’t mean they are not adding new clients. Almost all the IT companies have reported very healthy order book, some even their largest ever. There is always a lag between signing up a new client and execution.

Now coming to margins, they are not really expanding, they are just normalizing. The reasons margin went south, for entire indian IT industry, in 2022 and 2023 were:

1- High attrition IT- Higher salary increments paid to existing staff to retain them

2- Higher bench- IT companies hired like crazy in 2021 in anticipation of more work post-covid which never materialized due to slow down in IT spend in their key markets (US, UK, Europe)

3- Higher subcontractor deployment- due to high attrition

Now that talent market has cooled with industry wide layoffs, companies are hiring less. Attrition has gone back to historical averages which means lesser salary increments. Subcontracting has also gone down. Finally IT companies are using automation to improve their operating efficiencies.

For Zensar 18% is their highest reported EBITDA and they are still not there yet. With further revenue growth, operating leverage might even take it above 18%. Given the cheapest valuation among their peer group I find the stock quite well placed.

Disclosure- Invested in stock since 2022 (at 250 level) and could be biased.

By the way I am among very few who has continuously increased his allocation to IT stocks in 2022 and 2023 even when celebrated fund managers were giving sell calls and telling everyone to avoid the sector. Some even said CHATGPT will kill the industry.

I have worked in IT industry for close to 20 years and have seen the cycles so was confident this one will reverse too. Some of my best returns in 2023 have come from IT stocks thankfully.

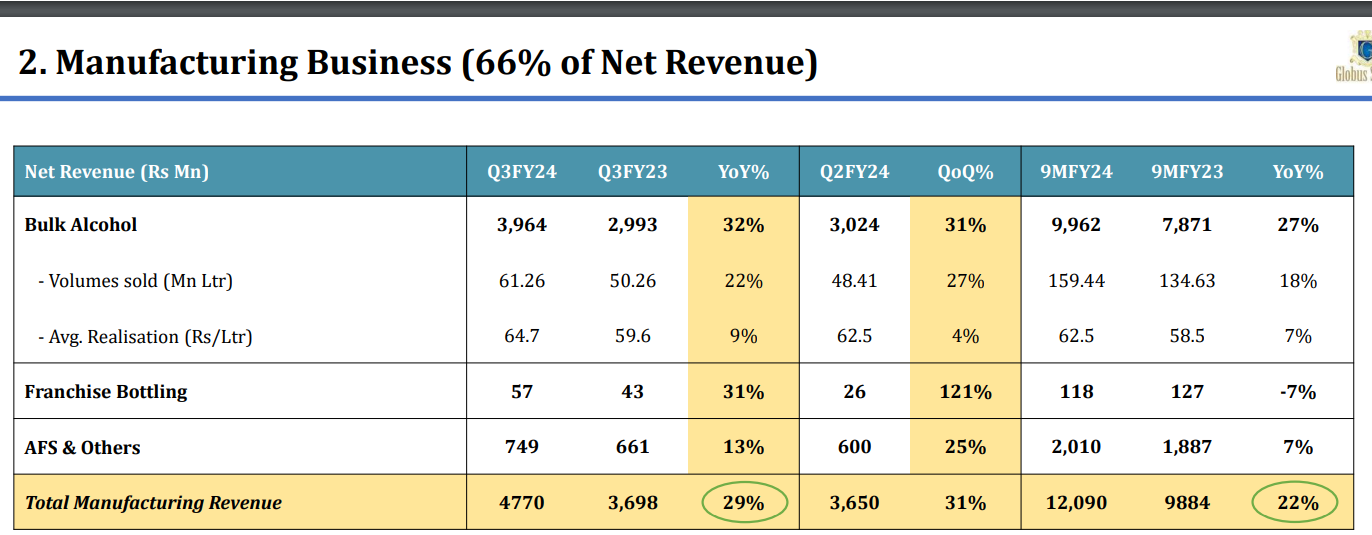

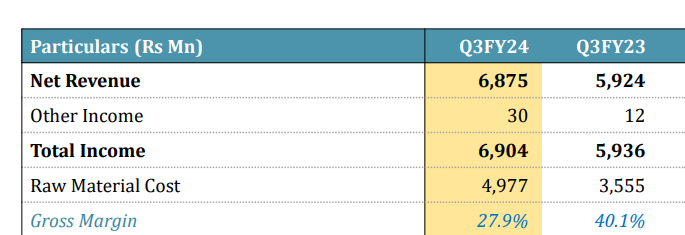

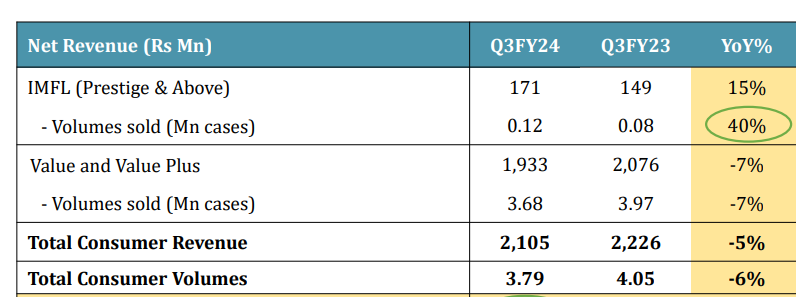

Globus Spirits (10-02-2024)

Great sales growth!! Steady growth in sales for the past many quarters. Capacity utilization back at 90%. I was eager to know what triggered the growth in sales.

Bulk segment performed with significant growth in bulk alcohol, franchisee bottling and by products on a QoQ basis.

Margin compression was expected as management guided in the last concall. Gross margin dipped further

Consumer sales down down YoY

Prestige still a very small part of the sales. Still at a nascent stage. Still a long way to go.

Have new capacities coming onstream next quarter which can further aid sales growth

Margins could be cyclically at the lowest levels.