Q3 Results are good. They achieved 10% margin which is 2017 level. From the next quarter PEB new plant will start producing from Feb 24. So, revenue growth will be there from next quarter. Re-rating expected.

Q3 Results are good. They achieved 10% margin which is 2017 level. From the next quarter PEB new plant will start producing from Feb 24. So, revenue growth will be there from next quarter. Re-rating expected.

Thanks for reminding about PPFCF stake in HDFC Ltd before merger. I edited my comment accordingly.

Per concall, they said this was because of 1 time expense on UP project of c.5 Cr. UP project is expected to end next quarter and they do not foresee incurring this again. Overall margin guidance is at 11-12% in FY24 and going forward.

Another reason for dip is interest which is attributable to Surat diamond dispute receivable + UP receivable. If Surat diamond does not reconcile by March 24, then arbitration is reqd which might take an year. To curtail high interest cost, Co has passed QIP resolution recently. If its gets resolved, they expect to get debt to normal levels. Capex guidance stays at 4% of revenue. Precast facility is currently operating at 50% utilization though at a lower margins [EBITDA positive] which they expect would ramp if opportunity strikes (i.e; if someone is willing to pay a premium for early completion).

No provisions are made in books for Surat diamond dispute. Monitorable on bad debts.

Rev guidance for FY25 is 3000 Cr with margins of 11-12%. Mgmt did say in EPC project 1-1.5% fluctuations are normal.

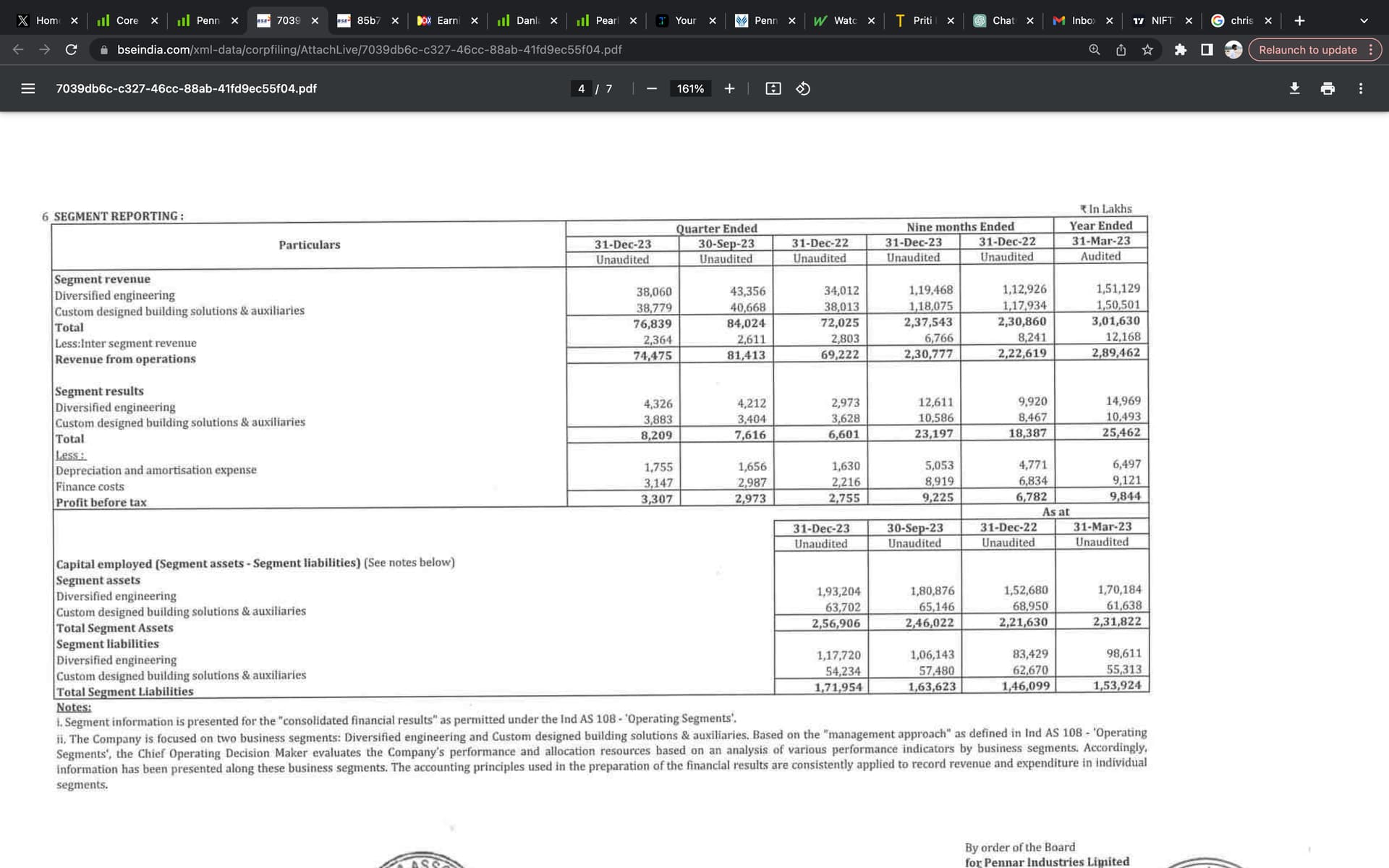

Decent results

Q3 CONS NET PROFIT 238M RUPEES VS 198M (YOY); 260M (QOQ)

Q3 REVENUE 2.43B RUPEES VS 2.7B (YOY); 2.4B (QOQ)

We should look at EBIDTA as there is large deferred tax item this Q. On EBIDTA(417 M) basis they have shown growth Y-o-Y(367M last year) as well as Q-o-Q(399 M last Q). Revenue is a function of gas prices so we should look at gas volumes.

A good move which can add scale to Mahindra defence

Yes, PPFCF had -8% exposure to HDFC ltd. Before jan 2023. After merger of HDFC twins – they are now holdc bank.

What I find very interesting personally is that it is HDFc ltd. Which has brought up the cost of capital after merger and therefore, that lead to the market giving them a good beating. PPFCF was betting on this business with higher CoC and lending across specific lending categories.

Also, Mr Thakkar had earlier spoken about how 3-4 quarters after merger will be difficult and will take streamlining business. Streamlining = replacing high cost of capital of HDFC ltd with the Low cost of capital which bank gets. (This happens on maturity of various loans).

Another thing, HDFC ltd deposits are not growing at the pace of lending. For deposits:

I like how things stand. Open to other critiques.

This is just my opinion and I’m invested. Therefore biased.

With 8.1% of weightage in HDFC bank, PPFCF is betting heavily on HDFC bank for its next 5 yr return as they are reducing their exposure to ITC and Bajaj Holding which i think is the right strategy.

PPFCF would have had more than 8.1% exposure to HDFC bank but being a MF they cannot. They have kept 1.9% as cushion for any market crash scenario or they had already at 10% now after this 15% correction within a month. But retail investors have the gift of having unlimited exposure to a given stock.

we are at the peak of rate cycle. A minimum of 3 to a maximum of 6 rate cuts expected in HY2 of FY25. I always wanted to have big exposure to high quality company at lower valuation but it never happened in case of HDFC bank in the last decade except covid crash. But i had plenty of other options during that crash. Now when entire market is at peak valuation, i am glad to see HDFC bank at 14.7 PE which gave me the opportunity to increase stake throughout FY24. If return expectation is to beat nifty by nominal 3%, then HDFC bank may be right choice for next 5 yrs.

Not sure on what basis they arrived, but here is the latest from management.

This means more than 2.5 GW for next two financial years.

Apollo pipes is planning to invest 125 cr in Kisan mouldings will be big boost for having strong foot hold in UP and other parts of india.

7bbcdfb6-9dd6-439f-9a33-96014b3ff033.pdf (272.8 KB)

0786ddfe-81e9-4a41-bb0b-26a39fe962c7.pdf (783.6 KB)

Thank you Amol 2021.