cell and gene therapy solutions sound very interesting. however, the results may or may not be interesting. any thoughts on NATCO pharma investment in EYWA pharma Singapore?

Posts tagged Value Pickr

Use of Large Language Models For stock research (08-02-2024)

Like if you can work with apis only that can be a use case but I am also making a react app to easily just add file and chat with the assistant easily so even non tech people can run it locally.

Garware Hi-tech films (Earlier Garware polyester) (08-02-2024)

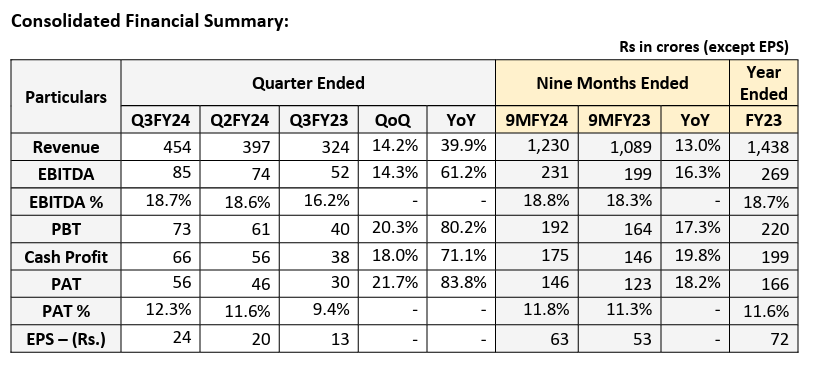

Q3 FY24 -Blockbuster Results

Records Highest ever quarterly revenues and profitability

Q3FY24 consolidated revenue up by 40% YoY at Rs. 454 crores and

PAT up by 84% YoY at Rs 56 crores

Paint Protection Film business continues robust performance, driven by significant demand increase, contributing one-third of revenue

Solar Control Film continues growth trajectory back with global demand recovery

Launched world’s first Rooftop series for the automobile segment

Robust response received in Expo – Automechanika and ACE Tech (Architectural)

Dr S. B. Garware, Chairperson and Managing Director of GHFL

“…Going forward, product innovation remains our cornerstone, coupled with aggressive

sales and marketing strategy, to drive us towards higher value-added products and

profitability.”

Ms Monika Garware, Vice Chairperson and Joint Managing Director of GHFL

” While the industry faced geo-political challenges, including “red sea crisis” and supply chain

issues in the later part of the quarter, our performance remained strong. This resilience is

attributed to strong demand for PPF, solid recovery in SCF across domestic and international

markets, supported by effective shipping and logistics.”

Business Updates:

Paint Protection Film (PPF)

The PPF business achieved a substantial 35% sequential revenue growth in Q3FY24 compared

to Q2FY24, due to strong demand primarily from USA, Middle East and India. Recent launch

of Ceramic Coating, complementing our PPF product line, aims to further enhance growth

prospects. The business delivered a significant 36% contribution to total revenue in Q3FY24.

The PPF plant is running at optimal capacity with intermediate processes supported by other

lines.

Solar Control Film (SCF)

SCF business accounts for around one-third of the company’s total revenue and has achieved

a 10% sequential revenue growth in Q3FY24 compared to Q2FY24, due to improved global

macroeconomic environment and surge in automobile sales. This growth momentum is

expected to continue with strategic diversification into the architectural film segment. The

architectural films products have made a successful debut at the recent ACE Tech expo,

garnering considerable interest from key stakeholders.

The company foresees accelerated growth in the untapped domestic market. The recent

unveiling of Rooftop series products at the Automechanika Expo underscores the company’s

dedication to meeting specific domestic market demands. Furthermore, the exhibition of PPF

products at the expo garnered significant interest from OEMs, retailers, and car enthusiasts,

reinforcing the company’s focus on domestic market potential.

IPD Business

The IPD business experienced a decline in Q3FY24 compared to Q3FY23 due to industry

headwinds. The capacity utilization of IPD plants stood at 72% in this quarter as compared

82% in Q3FY23. Despite this, the Company’s strategic emphasis on expanding its specialty

segments and improving capacity utilization underscores its commitment to strengthening

market presence and increase future profitability for the IPD business.

Revenue Growth

GHFL delivered a robust performance in Q3FY24, achieving its highest-ever revenue and

profitability. Consolidated revenues surged 40% to Rs. 454 crores and consolidated PAT

increased by an impressive 84% to Rs. 56 crores, compared to the corresponding quarter last

year, demonstrating the company’s strong financial momentum. The key growth driver in

Q3FY24 was the CPD segment, encompassing PPF and SCF businesses, which witnessed a

remarkable 80% YoY revenue growth. This remarkable performance was partially offset by a

9% YoY decline in the IPD segment. Notably, 82% of GHFL’s revenue comes from exports,

primarily driven by North America and Asian markets. Additionally, the company’s focus on

value-add films contributes approximately 91% of its total revenue, positioning it for superior

growth in the industry.

Margin

GHFL reported outstanding EBITDA growth in Q3FY24, demonstrating continued financial

strength. EBITDA surged 61.2% YoY to Rs. 85 crores, with the margin expanding to 18.7%

compared to 16.2% in the corresponding quarter last year. This improvement was primarily

driven by higher volumes in the PPF and SCF film segments. However, margin pressure on IPD

products and strategic investments in marketing and sales initiatives partially tempered the

EBITDA gains. While an aggressive marketing strategy has led to strong sales performance, it

has also resulted in temporary margin pressures. The company is confident that these

investments are expected to pave the way for sustainable growth and market leadership in

the long term.

Nestle India – FMCG Play (08-02-2024)

On their website it mentioned as Nestle India and address is also same. On Amazon also packer and manufacturer is mentioned a Nestle India.

Also, I could read Nestle India Ltd on one of the packs. Amazing range of health products.

Amazing range of lifestyle and health products from a trusted brand. They will dominate OTC.

They have leveraged their multiple global health brands to launch Nestle Resource in India.

Nestle India has been a fair MNC unlike Pharma MNCs or Cummins.

Only their pet food was independent initially as it was loss making but merged with Nestle India now.

Natco Pharma: Focusing On Complex Products (08-02-2024)

according to the export data shared by mohit, natco pharma has export value of 1710 mn in Q3FY23 and 1390mn in Q2FY24. however, according the NATCO pharma PPT concall presentation, its 3337mn IN Q3FY23 and 7923mn in Q2FY24. can any one verify and update…

Relaxo Footwear: a wannabe brand play (08-02-2024)

Good point. Thanks for the info

Mrs Bectors Food Specialities: Can it beat the industry? (08-02-2024)

Compared to other FMCG companies, the results aren’t bad QoQ at revenue level.

The reason for decline in profit needs to be seen as I am assuming raw material inflation should not be a factor. Yet to see press release.

I think the strong market reaction could also be due to the very sharp run-up this stock has seen over the last 10 months.

Interesting to know the Management commentary on margins going forward, how well they are managing the distributor expansion and contribution from overseas operations (Walmart, UAE etc) going forward.

Disclosure: Invested at 1,000 level. Keenly following this stock to add more once the Management commentary is out.

Oil India- has its time come? (08-02-2024)

It is still cheap. Expensive or cheap is a comparative thing. Compared to the other PSUs, and many private companies it’s earning is not really discounted. I have made some investment in this, Chennai Petro and IOL.

All three have risen substantially but to me still there is a lot of value left in these. Specially Chennai has impressive ROE & ROCE.

I am also hoping those who missed the bus in the Railways are going to make a beeline for these.

Relaxo Footwear: a wannabe brand play (08-02-2024)

Stock trading at absurd valuations. The only trigger which can create some opportunity for Relaxo could be the BIS which has been implemented from January 1st 2024. If this standard helps to erase un organized competition from the market, i think Relaxo can gain from it. With double digit volume growth & market share gain, we might see operating leverage play.

Mrs Bectors Food Specialities: Can it beat the industry? (08-02-2024)

I think its Q n Q which does not seems promising